Today Inflation may leave the Fed with no room to cut

Today’s inflation report may not decide the Federal Reserve’s next move on its own, but it could change the policy debate around the rest of 2026.

Inflation is expected to rise to 4.2%, up from 3.8% in April.

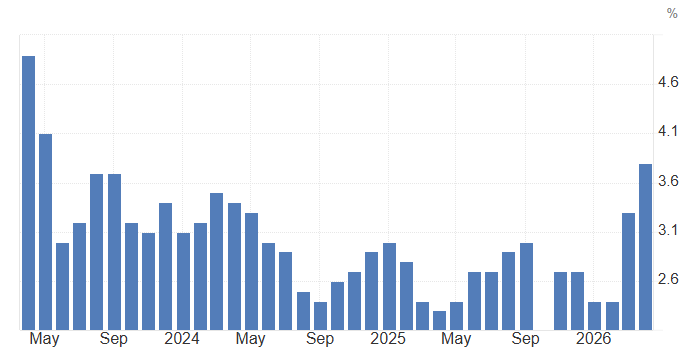

Rate-hike expectations have returned, with markets pricing a 68% probability of a move in the fourth quarter.

Treasury yields could move higher if the report confirms that inflation is accelerating again.

Inflation is back at the center of the Fed debate

The inflation report is arriving at a difficult moment for the Federal Reserve.

For much of the past year, investors were waiting for the economy to slow enough to justify rate cuts. Softer inflation readings helped with that story. Slower labour-market data helped it too. The assumption was simple: policy was already restrictive, inflation was gradually cooling, and the Fed would eventually have room to ease.

That story now looks less comfortable

Inflation is expected to rise to 4.2%, from 3.8% in April. If confirmed, it would be the highest annual rate since April 2023. The number matters not only because it is moving higher, but because it is rising while job growth is still strong.

That combination changes the Fed’s room for maneuvering. A central bank can talk about patience when inflation is falling. It is much harder to do that when inflation rises again and the labour market is still absorbing higher rates.

This is why today’s report matters. It may not force an immediate hike, but it could make rate cuts almost impossible to defend.

Source: U.S. Bureau of Labor Statistics

That combination leaves the Fed with little room to sound relaxed.

The market will not only watch whether inflation reaches 4.2%. It will watch where the pressure is coming from.

If the increase is mostly driven by energy, the Fed may be more careful. Energy shocks can lift headline inflation quickly, but policymakers often try to look through temporary moves unless they start feeding into broader prices.

The bigger risk is services inflation

If shelter, transportation, insurance, healthcare or other sticky categories remain firm, the Fed will have a harder time arguing that inflation is only a short-term problem. Services inflation tends to move slowly, and once it becomes embedded, it is harder to reverse without keeping policy tight for longer.

That distinction matters.

A headline inflation shock can move markets for a day. A broad inflation shock can change the policy path. If today’s report shows that inflation is not just higher but wider, the Fed will have little reason to keep any soft language around future easing.

The market is no longer trading a clean rate-cut story

The most important shift may come from the Fed’s language, not the rate decision itself.

Markets expect the central bank to formally remove its policy easing bias from the official statement. That would be a meaningful change. It would tell investors that the Fed no longer sees cuts as the natural next step.

This is not only about wording

Fed statements shape financial conditions. If the Fed sounds too relaxed while inflation is accelerating, markets may price lower yields, stronger equities and easier credit conditions. That would work against the central bank’s inflation fight.

The Fed does not want that

So even if officials are not ready to signal a near-term hike, they may still choose to close the door on cuts. The message would be simple: inflation is still too high, the labour market is still too strong, and policy cannot ease while those two facts remain in place.

A fourth-quarter hike is back in the conversation

The most important market shift is the return of rate-hike risk. Markets are now pricing around 68% probability of a Fed rate hike in the fourth quarter of 2026. That does not make a hike certain, but it shows how far expectations have moved.

This is no longer a market built around cuts. It is a market trying to decide whether inflation has become strong enough to force the Fed back into tightening mode.

A 4.2% inflation print would support that view, especially if the details show broad price pressure rather than a one-off move. The Fed can look through temporary noise. It cannot easily ignore renewed inflation pressure when job growth is also surging. For now, inflation is winning that debate.

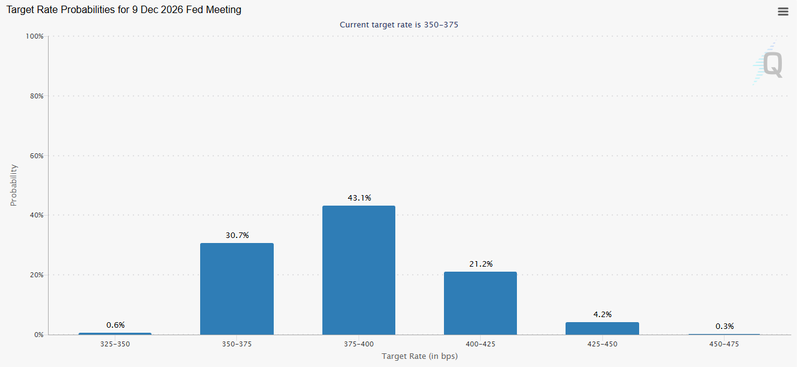

Source: CME Group