The UK balancing inflation, interest rates and the pound

The UK enters Q3 facing a difficult economic backdrop. Inflation remains too sticky, while growth is no longer strong enough to give the Bank of England unlimited room to keep policy restrictive. As a result, markets will be watching every data release closely, because the next move in interest rates, gilt yields and the pound will depend on whether inflation continues to cool without the economy losing too much momentum.

The majority within the Bank of England believe a weaker economy could help bring inflation under control without the need for further tightening.

Cutting rates while core inflation remains elevated could damage credibility.

The BoE will possibly maintain a higher-for-longer policy stance throughout Q3.

Higher for longer? The BoE’s next challenge

The Bank of England is not navigating a straightforward easing cycle. Growth is slowing, but inflation has not yet returned comfortably to target. That is the challenge. If policymakers cut rates too early, they risk keeping inflation expectations too high. If they keep policy tight for too long, they risk placing unnecessary pressure on households, businesses and credit conditions.

This is why the BoE's messaging has become more cautious. Markets may still expect policy easing over the coming quarters, but the Bank cannot commit to a fixed path while wage growth and services inflation remain sticky. Headline inflation still matters, but it is no longer the whole story. The BoE is paying closer attention to domestic inflation pressures because they are harder to reverse than energy-driven price shocks.

The majority within the Bank of England believe a weaker economy could help bring inflation under control without the need for further tightening. As demand slows and labour market conditions soften, companies become less able to pass higher costs on to consumers, particularly as spending becomes more cautious. This gave the Bank of England reason to keep the policy rate at 3.75% during Q2 rather than move towards further tightening.

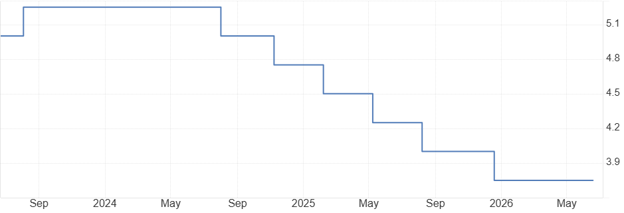

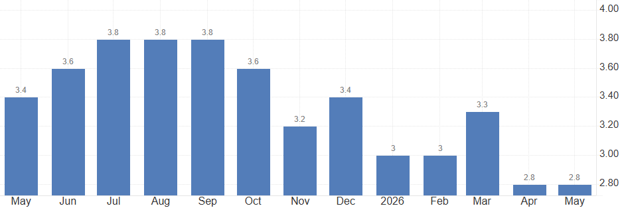

Source: BoE

Why inflation remains the UK's toughest challenge

The UK's inflation challenge has become increasingly driven by domestic pressures. While energy prices triggered the initial shock, services, wages and housing costs are now slowing the pace of disinflation.

Services inflation remains stubborn because it is closely linked to labour costs. Many service-sector businesses rely heavily on staff, so when wages rise, operating costs increase as well. Those costs are often passed on to consumers through higher prices, making inflation slower to fall. Weaker growth may reduce pricing pressure, but it is unlikely to bring prices down quickly while labour costs remain elevated.

Housing adds another layer of complexity. A shortage of supply continues to support rental costs, while higher borrowing costs have not resolved the shortage of homes. This leaves the Bank of England in a difficult position. Monetary policy can cool demand, but it cannot solve supply constraints.

That is why the Bank remains cautious. Cutting rates while core inflation remains elevated could damage credibility. But waiting too long could deepen the economic slowdown.

Source: Office for National Statistics

GBP's next move depends on growth, not just rates

Expectations for the pound will depend on how the UK's policy path differs from that of the US and the eurozone.

In the rate divergence scenario, inflation keeps the Bank of England on hold while the Fed and the ECB move towards easing. That could support the pound, as UK interest rates would remain relatively more attractive.

The second scenario is that higher borrowing costs begin to weigh more heavily on economic activity, leading to a sharper slowdown and forcing the BoE to cut rates. In that case, the pound could come under pressure as markets begin pricing in weaker growth, rather than focusing solely on the interest rate gap.

The stagflation scenario is the most challenging. The economy slows while inflation remains high, leaving monetary policy with few good options. Cutting rates could damage credibility, while keeping them high could place even greater pressure on growth. In this scenario, sterling volatility could increase and investors may demand a higher risk premium for holding the currency.

The BoE will possibly maintain a higher-for-longer policy stance throughout Q3 and will not rush into rate cuts after the first positive inflation reading. Inflation may ease further as energy pressures continue to fade, but that alone is unlikely to trigger a clear easing cycle while services inflation and wage growth remain stubborn.