Would higher interest rates really bring down US inflation?

The US enters the third quarter facing a familiar but increasingly complex challenge. Inflation remains above target, while economic growth and the labour market have stayed resilient enough to keep the prospect of further interest-rate increases on the table. The key question is whether tighter monetary policy would meaningfully reduce inflation or simply add pressure to an economy already dealing with supply-driven price shocks.

Tightening into the current shock carries a different risk.

The energy shock is real, but it does persistent enough to recreate the inflation spiral that followed the Russia-Ukraine conflict in 2022.

Market pricing of a brief hiking cycle followed by tentative rate cuts next year looks misplaced.

The policy dilemma facing the Fed

Inflation is keeping rate hikes on the table. Growth and the labour market are giving the Federal Reserve just enough room to consider them. That is the policy dilemma shaping the start of the third quarter.

Inflation remains above target, the economy has not collapsed, and the labour market is cooling without breaking. On paper, this gives the Federal Reserve, led by Kevin Warsh, room to argue that policy may need to remain restrictive for longer or even tighten further if inflation proves stubborn. The case for higher interest rates, however, is far less convincing. The real question is not whether the economy can absorb tighter policy, but whether tighter policy would address the kind of inflation the US is facing.

The latest inflation shock still appears to be driven more by supply constraints than overheating demand. Price pressures have been fuelled by energy market volatility, geopolitical risk and higher costs across oil-linked commodities, rather than by a broad acceleration in domestic demand. That distinction matters. Higher interest rates can cool spending, weaken credit conditions and slow hiring. They cannot produce more crude oil, lower fertiliser prices, ease shipping disruptions or remove geopolitical risk from the Strait of Hormuz.

This is why tightening into the current shock carries a different risk. It could do little to address the underlying drivers of inflation while adding pressure to an economy already absorbing higher input costs.

Inflation is still sticky, but the worst may be behind us

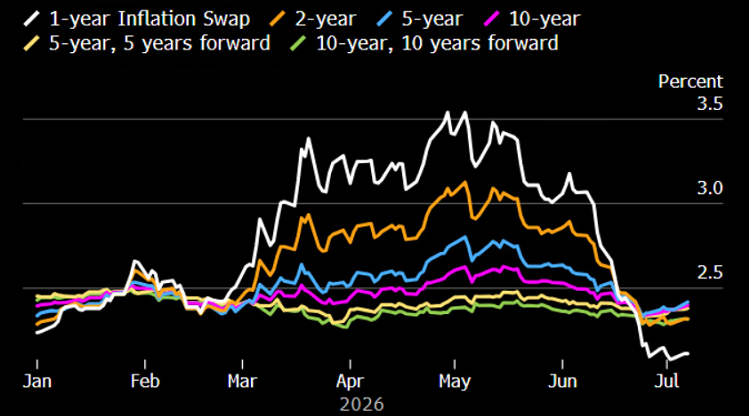

Headline inflation appears to have peaked in May, with both CPI and PCE inflation likely to ease in June as the earlier surge in energy prices fades. While renewed geopolitical tensions show the backdrop remains fragile, the inflation outlook does not depend entirely on a lasting ceasefire.

For headline inflation to reach a new high, oil would likely need to return to extreme price levels. That remains outside the baseline scenario unless geopolitical tensions escalate significantly. The energy shock is real, but it does not yet appear large or persistent enough to recreate the inflation spiral that followed the Russia-Ukraine conflict in 2022.

Source: Bloomberg

The broader commodity spillover also appears more contained this time. Prices for jet fuel, fertiliser, plastics, aluminium, polymers, natural gas and other oil-related inputs have already peaked in most cases and are now moving lower. Steel remains the main exception. That suggests the second-round effects of the latest energy shock are fading more quickly than they did in 2022.

This does not make inflation harmless. It makes the policy response more complicated. If the shock is already reversing, additional rate hikes risk responding to yesterday's inflation pressures rather than tomorrow's inflation trend.

The Fed needs to respond to inflation, not just react to it

Energy inflation is never harmless, even when it starts outside the core basket. The Fed learned that lesson earlier in the decade. A shock in oil or gas prices can quickly feed through transport costs, utilities, imported goods and corporate margins. Companies facing higher costs eventually must choose between absorbing the hit or passing it on to consumers.

The difference this time is that the pass-through still appears contained. Core inflation is running below headline inflation at 2.9% versus 4.2%, inflation expectations remain broadly anchored, and the labour market has not generated the kind of wage-price spiral that would force the Fed into a more aggressive tightening cycle. That gives policymakers room to be patient, even if it does not give them room to be dovish.

Source: Bloomberg

The US economy remains resilient, but it is not overheating. Real GDP is expected to grow by around 2.1% in 2026 before easing to an average of about 1.9% in 2027 and 2028. That is neither a boom nor a recession. The labour market tells a similar story, with unemployment at around 4.3%: high enough to show cooling, but not high enough to force rate cuts. This is the uncomfortable middle ground. The economy is too strong to give the Fed a clear reason to cut rates, but the inflation shock remains too supply-driven for higher interest rates to look like a straightforward solution.

Are markets expecting the wrong outcome?

Market pricing of a brief hiking cycle followed by tentative rate cuts next year looks misplaced. If the Fed raises rates into the later stages of a temporary supply shock, the disinflationary benefit could be limited. The cost, however, would likely emerge later through a weaker labour market in 2027 and 2028.

That leaves the third-quarter baseline looking less like the start of a renewed tightening cycle and more like an extended pause. The Fed may prefer to keep rates steady while monitoring inflation expectations, especially if oil prices continue to retreat and the latest energy shock fades.

The risk scenario is different. The Fed could still follow a path similar to the European Central Bank by delivering one rate hike before returning to a data-dependent stance. Such a move would shift market attention towards the labour market's ability to withstand higher rates for longer.

Either way, the Fed's dilemma will remain one of balance. Even if policymakers choose a more restrictive path, they will still need to weigh inflation risks against the lagged effects of tighter policy on growth, credit and hiring. That is where the third-quarter tension may become most visible: in the gap between market pricing and the Fed's reaction function. If that gap widens, financial assets could face sharper swings as investors reprice the path for rates, growth and inflation.