ECB rate hike risks reviving the 2011 policy mistake as inflation shock tests Europe

The European Central Bank is preparing for one of its most difficult policy decisions in years. Inflation is rising again, energy prices are feeding price pressures, and officials want to defend their credibility. But with eurozone growth weakening, a premature rate hike could leave the ECB exposed to the same criticism it faced in 2011: tightening into a fragile economy just before conditions deteriorate.

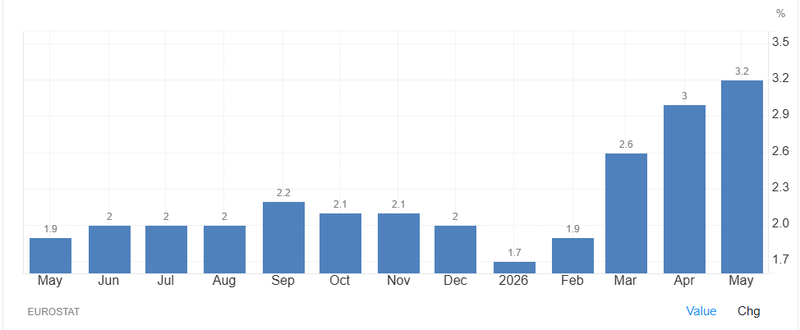

Eurozone inflation has already risen to 3.2%.

The ECB is weighing a rate hike as energy prices climb.

Economists warn of a possible repeat of the 2011 policy error.

Weak growth and falling PMIs make the decision more dangerous.

ECB faces a credibility test as inflation rises again

The European Central Bank is moving closer to a rate hike as officials grow more concerned that higher energy prices could turn into a broader inflation problem across the eurozone.

The pressure is clear. Inflation in the 21-country bloc has already reached 3.2%, moving further above the ECB’s 2% target. Underlying price pressures have also strengthened, while business surveys show that companies still plan to raise prices. Household inflation expectations are elevated as well, raising concern that the latest energy shock could become more deeply embedded in the economy.

Source: TradingEconomics

For the ECB, this is not only a question of inflation data. It is a question of credibility.

After being accused of reacting too slowly during the 2021-2022 inflation surge, policymakers are wary of repeating the same mistake. Russia’s invasion of Ukraine sent energy prices sharply higher, eurozone inflation eventually hit a record 10.6%, and the ECB was forced into an aggressive tightening campaign. That experience still shapes the current debate.

This time, officials do not want to look passive. But acting too soon carries its own risk.

The 2011 mistake still shadows ECB policy

The warning from economists is straightforward: the ECB may be at risk of repeating its 2011 error.

In 2011, under Jean-Claude Trichet, the central bank raised rates twice as commodity and energy prices pushed inflation higher. The decision was later widely criticized because the eurozone economy was already vulnerable. The region’s debt crisis deepened, financial stress intensified, and the ECB was forced to reverse course after Mario Draghi became president.

The lesson from that period is uncomfortable. Inflation shocks driven by energy prices can look dangerous in the short term, but tightening policy into a weak economy can make the damage worse.

That is why the current debate is so sensitive. The ECB is again facing higher energy-driven inflation at a time when growth is losing momentum. A rate hike may help protect the central bank’s inflation-fighting image, but it could also increase pressure on households, firms and weaker eurozone economies.

Inflation expectations are driving the hawkish case

The strongest argument for a rate hike is inflation psychology.

ECB officials worry that households and firms may start to believe inflation will stay above target for too long. Once inflation expectations become unanchored, the central bank’s job becomes much harder. Higher wage demands, stronger pricing power and defensive corporate behavior can turn a temporary energy shock into a more persistent inflation cycle.

This is why hawkish policymakers argue that the ECB can no longer simply “look through” higher energy prices.

The latest inflation reading at 3.2% is already uncomfortable. If energy prices keep rising and core inflation continues to firm, the central bank may feel forced to act before second-round effects become clearer.

In that sense, a rate hike would be less about crushing current demand and more about sending a message: the ECB remains committed to its 2% inflation target.

The growth backdrop argues for caution

The problem is that the eurozone economy is not in a strong position.

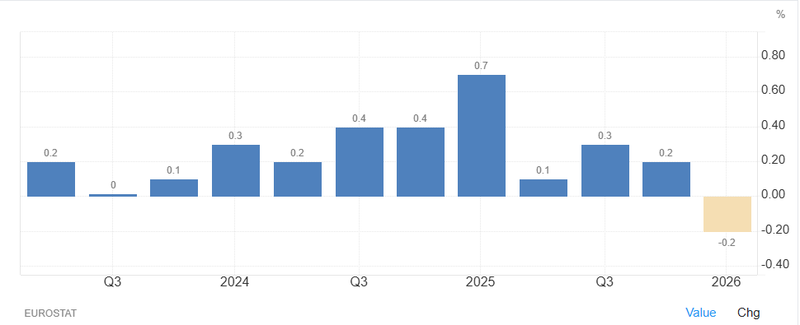

Business activity has weakened, and survey data show the composite PMI at its lowest level since 2024. Manufacturing remains under pressure, services are slowing, and France is showing particular signs of weakness. The eurozone economy also shrank at the start of the year after a sharp contraction in Ireland forced revisions to earlier growth estimates.

Even excluding the distortion from Irish data, growth appears modest, estimated around 0.2% to 0.3%.

That is not the kind of backdrop that gives central banks much comfort when raising rates. Higher borrowing costs could weigh on households already dealing with expensive energy and weaker real income. They could also pressure firms at a time when demand is softening.

This is the core policy dilemma: inflation is too high, but growth is too weak.

Source: TradingEconomics

Why a rate hike could backfire

A rate hike would be easier to justify if there were clear evidence that higher energy prices were feeding into wages and broader inflation. So far, that evidence is not decisive.

Some economists argue that faster core inflation may reflect factors beyond energy pass-through. Others see limited signs of excessive wage pressure. If the ECB tightens before second-round effects are firmly visible, it risks adding unnecessary pressure to an economy already struggling with weak demand.

That is where the 2011 comparison becomes powerful.

The ECB can raise rates to prove its anti-inflation credibility, but if the economy deteriorates quickly after the move, markets may see the decision as another policy mistake. A central bank that hikes and then cuts soon afterward can still defend the move as an “insurance” step, but the political and economic cost may be high.

Markets expect hikes, then cuts

Investors and economists are increasingly pricing a complicated ECB path: rate hikes first, followed by rate cuts later.

The market consensus points to two quarter-point rate increases this year, reflecting the view that inflation is running above the ECB’s comfort zone. But expectations also include at least one rate cut in mid-2027, as growth weakness eventually forces the central bank to ease again.

This kind of path is not unusual under uncertainty. Policymakers may argue that a temporary tightening step is needed to protect inflation expectations, then reverse it once the shock fades.

The danger is perception. If the ECB hikes now and cuts later because the economy weakens sharply, the move may be remembered less as insurance and more as a premature tightening cycle.

The ECB is becoming the G7’s lead hawk

Another reason the decision matters is the ECB’s position relative to other major central banks.

The Federal Reserve has adopted a more cautious wait-and-see stance as it monitors the economic fallout from geopolitical tensions and higher energy prices. The ECB, by contrast, appears closer to acting quickly, which would make it one of the most aggressive inflation fighters among Group of Seven central banks.

That contrast could support the euro in the short term if markets see the ECB as more hawkish than the Fed. But it could also hurt eurozone assets if investors conclude that the central bank is tightening into weakness.

For European equities and bonds, the message would be mixed. A stronger inflation-fighting stance may help credibility, but higher rates could pressure valuations, credit conditions and consumer demand.

Households and firms may carry the cost

The economic cost of an ECB rate hike would not be evenly distributed.

Households are already dealing with higher living costs, especially if energy prices remain elevated. Higher interest rates can add pressure through mortgages, consumer credit and weaker job security. Firms face a similar challenge as borrowing costs rise while demand slows.

This is why some economists argue that the inflation shock may fade on its own if growth weakness deepens. If consumer demand is already under pressure, companies may struggle to pass higher costs through for long. In that case, tightening policy may not be necessary to bring inflation down.

The ECB’s challenge is that waiting carries risk, but acting carries risk too.

Market takeaway

The ECB is trapped between two painful memories.

The first is 2021-2022, when inflation accelerated sharply and the central bank was accused of reacting too late. The second is 2011, when the ECB raised rates into a fragile economy and was later forced to reverse course as the debt crisis worsened.

This week’s decision sits directly between those two lessons.

A rate hike may help protect the ECB’s credibility and send a clear signal that inflation above 2% will not be tolerated. But with eurozone growth weakening, business activity slowing and energy prices driving much of the inflation shock, tightening policy now could become a costly error.

For markets, the key issue is not only whether the ECB hikes. It is whether President Christine Lagarde can convince investors that any move is a limited insurance step, not the start of a longer tightening cycle.

If the ECB signals restraint after a hike, the damage may be contained. If investors see the move as the beginning of repeated tightening into a weak economy, Europe could face a much tougher market reaction.