Kevin Warsh’s Fed debut sparks bond selloff as rate-hike bets surge

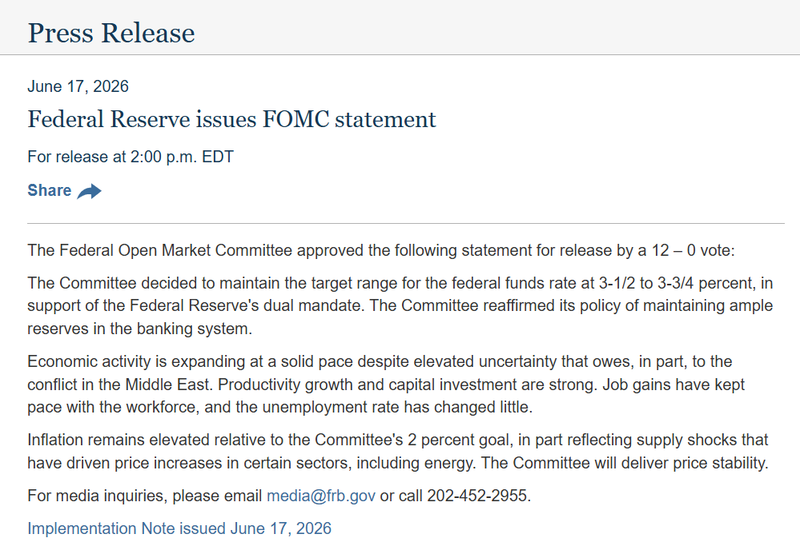

Kevin Warsh’s first Federal Reserve meeting delivered a clear message to markets: inflation is back at the center of policy. The Fed held rates steady at 3.5% to 3.75%, but Warsh’s debut press conference, a shorter policy statement and new rate projections pushed traders to price a more aggressive path for rate hikes, triggering a sharp selloff in short-term Treasuries.

The Fed held rates steady at 3.5% to 3.75%.

Two-year Treasury yields jumped 13 basis points.

Futures traders priced a quarter-point hike by October.

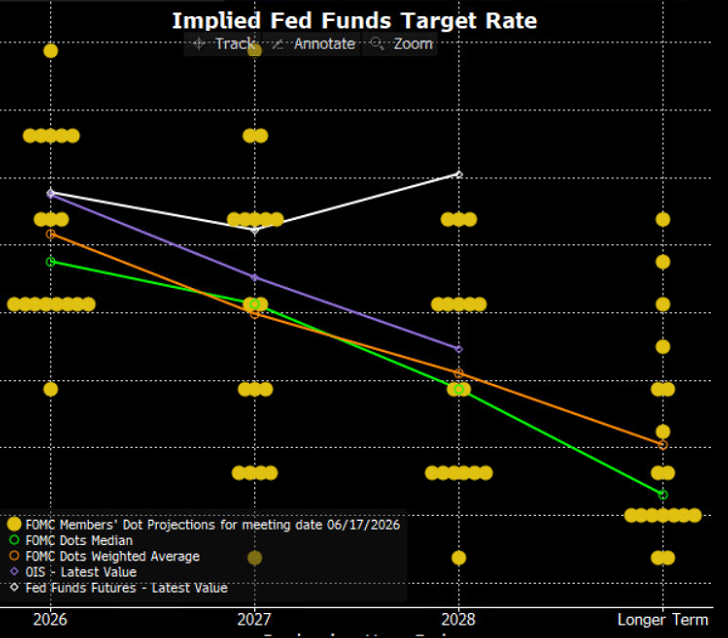

Nine of 19 Fed officials expect at least one rate hike this year.

Warsh sends a clear inflation message

Kevin Warsh needed only one meeting to reset expectations across the bond market.

In his first press conference as Federal Reserve chair, Warsh made price stability the main message. The Fed kept interest rates unchanged in a range of 3.5% to 3.75%, but investors focused less on the rate decision and more on the tone. The message was direct: the central bank is not ready to tolerate inflation staying above target.

Source: TradingEconomics

That was enough to trigger a wave of repositioning. Traders sold short-term Treasuries, futures markets shifted toward rate-hike bets, and Wall Street began treating the new Fed leadership as more serious about inflation than some investors had feared.

The meeting also helped reduce doubts about whether Warsh would bend toward political pressure for lower rates. Instead, his first appearance suggested that the Fed’s inflation mandate remains the priority.

Treasury yields jump after the Fed meeting

The sharpest reaction came in the front end of the Treasury market.

Two-year Treasury yields rose 13 basis points, the biggest one-day increase since April 2025. It also matched the largest move in two-year yields on a Fed meeting day since 2008. That matters because two-year yields closely track expectations for the path of monetary policy.

The move showed that investors were no longer treating rate hikes as a distant risk. Futures traders strengthened bets on a quarter-point rate hike by October, and pricing shifted toward two hikes by the end of the first quarter of 2027, compared with one before the Fed decision.

Longer-term bonds moved differently. Thirty-year Treasury yields slipped to their lowest level since late April, suggesting that markets believe a tougher Fed stance could eventually help contain inflation over the longer run.

The yield premium investors demand to hold 30-year bonds over two-year notes remained near a 14-month low after Wednesday’s move, reflecting a flatter curve and a stronger focus on near-term policy tightening.

Source: Bloomberg

Fed projections move closer to rate hikes

The Fed’s updated projections gave the market another reason to reprice.

Of the 19 policymakers, nine now expect at least one rate hike this year. That is a major signal, even though the Fed did not raise rates at this meeting. It shows that the committee is moving closer to the view that tighter policy may be needed if inflation remains too high.

Source: Bloomberg

The policy statement was also changed. It was less than half as long as the previous one and included a pledge to “deliver price stability.” The shorter format matched Warsh’s push to reduce forward guidance and avoid locking the Fed into a detailed policy path.

Source: Federal Reserve

That shift matters for investors. Warsh is moving the Fed away from heavy signaling and toward greater flexibility. Markets may get fewer clues in advance, but each inflation print and labor-market report could become more important for pricing the next move.

Inflation remains too high for a dovish pivot

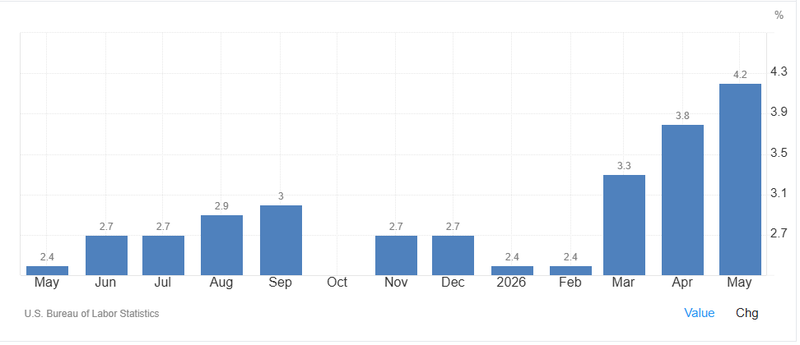

The Fed’s renewed focus on inflation comes after price pressures accelerated again.

Inflation has remained above the Fed’s 2% target for five years. The latest surge, driven partly by the Iran war’s oil shock, had already pushed investors away from earlier expectations for rate cuts. Businesses facing higher costs have been passing some of that pressure to consumers, while the economy has remained more resilient than expected.

Source: TradingEconomics

Energy prices are no longer the only issue. Job growth has picked up, consumer spending has been supported by a record-setting stock rally, and the artificial-intelligence investment boom continues to pour capital into the economy.

That mix makes the Fed’s job harder. Lower oil prices after the US-Iran deal may ease some pressure, but stronger growth and sticky inflation mean policymakers cannot quickly return to a rate-cut narrative.

Warsh avoids giving his own rate path

Warsh delivered a hawkish inflation message, but he avoided giving markets a personal rate forecast.

He did not commit to raising rates and made clear that the Fed should not be bound by forecasts in an uncertain economy. He also declined to submit his own projection to the Fed’s dot plot, reinforcing his preference for less forward guidance.

That created a careful balance. Warsh reassured investors that inflation remains the priority, but he avoided boxing himself into a specific rate path. The Fed can still hike if the data demands it, but it is not pre-committing to a move.

The approach also gives Warsh room politically. President Donald Trump has pushed for lower rates, but Warsh’s message allowed the Fed to sound firm on inflation without directly declaring that higher rates are inevitable.

Fed communication is entering a new phase

Warsh also began changing how the Fed communicates.

The shorter statement and the removal of forward guidance marked the first clear signs of his planned overhaul. He also announced five task forces that will review different parts of how the central bank works, including the data used to forecast the economy and the way policy is implemented.

Those task forces are expected to deliver findings by the end of the year. That timeline suggests Warsh wants reform, but not a sudden shock to the institution. The first step is controlled change, not an immediate restructuring of the Fed.

For markets, the communication shift is important. Less forward guidance means investors may need to rely more heavily on incoming data and less on explicit Fed signaling. That could increase volatility around inflation, jobs and wage reports.

Fed independence gets a first market test

Warsh’s debut also carried a political dimension.

He took over after months of pressure on the Fed from the Trump administration, including criticism of Jerome Powell and calls for lower rates. That made his first meeting a test of central-bank independence as much as a test of monetary policy.

The market reaction suggests investors took comfort from the Fed’s inflation message. A stronger commitment to price stability helped ease concern that policy could be shaped by White House pressure rather than economic data.

Still, Warsh is walking a fine line. He must preserve credibility with bond investors while avoiding an unnecessary confrontation with the administration. His first meeting managed that balance, but future decisions will be harder if inflation remains high and political pressure for lower rates intensifies.