Kevin Warsh faces first Fed test as markets bet on rate hikes by December

Federal Reserve Chair Kevin Warsh enters his first major policy meeting with markets still pricing the risk of rate hikes by December. But the US-Iran peace framework has changed part of the outlook. Lower oil prices could ease inflation expectations, giving Warsh more room to sound balanced rather than aggressively hawkish in his first press conference.

The Fed is expected to hold rates at 3.5% to 3.75%.

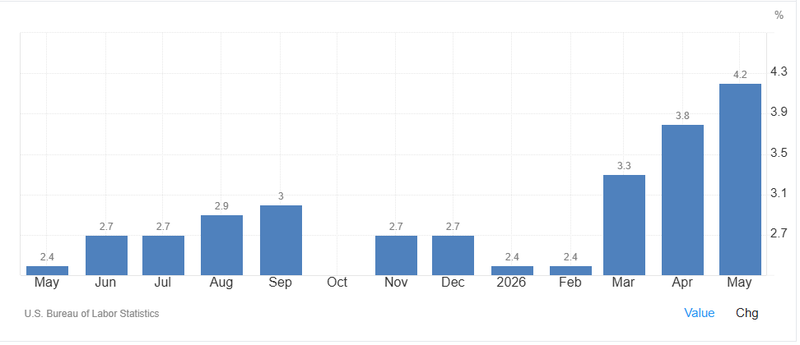

US CPI rose 4.2% in May, the fastest pace since April 2023.

Traders still price about a 60% chance of a 25-basis-point rate hike by December.

Lower oil prices after the US-Iran peace deal could soften inflation expectations.

Warsh faces his first major Fed test

Kevin Warsh is only three weeks into his role as Federal Reserve chair, but his first major policy test has already arrived.

The Fed is widely expected to keep interest rates unchanged this week in a range of 3.5% to 3.75%. The decision itself may not surprise markets. The real focus will be on Warsh’s first press conference, the Fed’s updated statement and the new economic forecasts.

Markets want to know whether the Fed is preparing to return to inflation-fighting mode, or whether the recent easing in oil prices after the US-Iran peace framework gives policymakers more room to wait.

That difference matters. Until recently, investors were moving away from rate-cut expectations and pricing a growing chance that the Fed may need to raise rates again by December. Now, the decline in oil prices has introduced a more balanced question: does the Fed still need to sound aggressively hawkish if one of the biggest inflation risks is starting to fade?

Inflation remains the Fed’s main problem

The inflation data still looks uncomfortable.

US consumer prices rose 4.2% year over year in May, the fastest annual increase since April 2023. Inflation has also remained above the Fed’s 2% target for the past five years, leaving policymakers with limited room to declare victory.

Source: TradningEconomics

The earlier surge in oil prices after the Iran war made the problem more serious. Higher energy costs fed directly into business expenses, transportation costs and consumer prices. That pushed investors to question whether inflation could become more persistent and whether the Fed would need to tighten policy again.

This is why bond markets reacted sharply. Traders moved away from expectations for rate cuts this year and began pricing the opposite risk. Two-year Treasury yields rose above 4%, while 30-year Treasury yields recently reached their highest level since 2007.

Those moves sent a clear message: if inflation stays high, markets believe rates may need to move higher.

Source: Bloomberg

The Iran peace deal changes part of the equation

The new factor is the US-Iran peace framework.

The agreement to halt the conflict has helped reduce immediate fears of a wider energy shock. As oil prices declined, the market began to reassess whether the inflation threat from energy would be as severe as feared.

This does not remove the inflation problem. CPI is still far above target, and the Fed cannot base policy on one move in oil prices. But lower crude prices can change the tone of the discussion. If energy prices remain under control, the pressure on headline inflation may ease in the coming months.

That gives Warsh more flexibility.

Before the peace framework, a hawkish message looked almost unavoidable. After the decline in oil, Warsh can acknowledge inflation risks while avoiding a strong commitment to rate hikes. He can keep the door open to tightening if inflation remains sticky, while also leaving space for rate cuts if price pressures cool faster than expected.

Markets still price rate-hike risk

The peace framework has reduced some pressure, but it has not erased rate-hike expectations.

Traders still price about a 60% chance of a 25-basis-point rate increase by December. That shows investors are not ready to believe the inflation risk has disappeared.

The Fed’s April meeting also showed that policymakers were already debating a tougher stance. Many officials warned that rate hikes could become necessary if inflation remained elevated. Some also wanted to remove the Fed’s bias toward lowering rates from the statement. Three officials dissented because they objected to the wording.

That internal divide makes Warsh’s first meeting more important. He has to guide a Fed that is not fully united, while also managing a market that is already testing his inflation credibility.

Trump wants lower rates, but the bond market wants proof

Warsh is also caught between the White House and the bond market.

President Donald Trump has repeatedly argued that the Fed should lower interest rates and has said that raising rates would be the wrong move. That creates a political challenge for Warsh from the start.

Markets are watching whether he will defend the Fed’s independence or appear too close to the administration’s preference for easier policy. The concern is especially sensitive after months of political pressure on the central bank, including attacks on Jerome Powell’s leadership and an effort to remove Governor Lisa Cook.

The bond market is asking for something different from the White House. It wants evidence that the Fed is still willing to fight inflation if needed.

This is where the lower oil price helps Warsh. It gives him a way to avoid looking politically weak without sounding unnecessarily aggressive. He can say the Fed remains data-dependent, recognizes inflation risks and will respond if price pressures persist, while also noting that lower energy prices could reduce the need for immediate tightening.

Warsh’s policy views remain a question

Warsh’s own views add another layer of uncertainty.

During his earlier term as a Fed governor from 2006 to 2011, he was known as a hawkish voice. That history may reassure investors worried about inflation. But in recent years, he became a sharp critic of the central bank and argued that artificial intelligence could create a significant disinflationary force by lifting productivity.

That point matters now because the US economy is also being supported by a strong AI investment boom. AI spending may help productivity over time, but it is also adding fuel to an already resilient economy through heavy capital investment.

Warsh has been largely quiet on monetary policy since being sworn in. That silence makes his first press conference more important. Markets do not only want to hear what the Fed does now. They want to understand how Warsh thinks about inflation, energy prices, AI productivity and the balance between growth and price stability.

Balance sheet policy could pressure long-term yields

Interest rates are not the only issue.

Warsh has also supported a broader shakeup at the Fed, including changes to inflation assessment, public communication and closer coordination with the Treasury Department. He has also advocated reducing the Fed’s large bond holdings.

That balance-sheet question matters for markets. If the Fed shrinks its bond portfolio more aggressively, private investors would need to absorb more Treasury supply. That could put upward pressure on long-term yields, especially with the government already facing heavy borrowing needs.

So even if Warsh avoids sounding hawkish on rate hikes, investors will still watch whether his balance-sheet approach tightens financial conditions through the long end of the yield curve.

What Warsh needs to deliver

Warsh does not need to announce a rate hike this week. Markets do not expect one.

He needs to deliver a credible framework.

The strongest message would be balanced: inflation is too high, the Fed is prepared to act if price pressures remain persistent, but the decline in oil prices after the US-Iran peace framework may reduce the urgency for an immediate hawkish pivot.

That tone would help Warsh in two ways. It would reassure bond investors that the Fed is not ignoring inflation, while also giving him room to avoid clashing immediately with the White House over higher rates.

The wrong message would be to sound too confident that inflation will fade without action. That could push Treasury yields higher again and raise doubts about the Fed’s credibility under new leadership.