Oil jumps 10% as Hormuz closed and U.S. fuel markets tighten

Return of strikes between the U.S. and Iran, along with United States reinstating Iran naval blockade around the Strait of Hormuz, has pushed oil higher by 10%. But the bigger issue is that this shock is hitting a market where inventories are already thin and refined-product margins are flashing stress.

U.S. Strategic Petroleum Reserve levels are near 316.5 million barrels.

OPEC cut its 2026 demand growth forecast for a third straight month to 780,000 barrels per day.

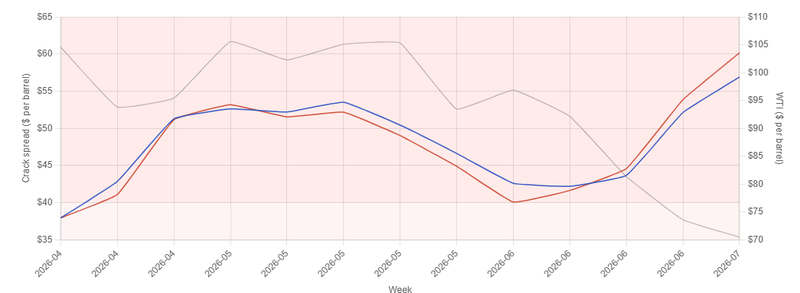

The 3-2-1 crack spread hit a record $64.58 per barrel.

The inventory cushion is too thin

The issue is not only that oil is rising. It is where it is rising from.

The U.S. Strategic Petroleum Reserve has fallen to roughly 316.5 million barrels. When combined with commercial inventories, total U.S. crude stocks are now at their lowest levels since 1984. That matters because inventories are the market’s shock absorber. When supply risk returns, traders immediately look at how much stored crude is available to soften the hit.

This time, the cushion is much thinner

The earlier release of around 172 million barrels helped stabilize fuel prices during previous periods of conflict and inflation pressure. But that support came at a cost. It left the U.S. with less stored crude available now, just as Hormuz risk is returning to the centre of the market. So, the latest price move is fear buying. It is the market realizing that the world’s largest oil consumer has less room to absorb another disruption than it did before.

![US - Strategic Petroleum Reserve [SPR]](https://eq-cdn.equiti-me.com/website/images/US_-_Strategic_Petroleum_Reserve_SPR.width-800.png)

Source: MacroMicro

Fuel margins are sending a stronger warning

The crude price matters, but the refining market may be sending a stronger signal.

The 3-2-1 crack spread has jumped to a record $64.58 per barrel. Diesel margins have also moved above $60 per barrel for the first time since the 2022 dislocation. These are not normal margin levels. They show that stress is not only in crude supply. It is also in the products that households, companies and transport networks use.

Inflation risk becomes more direct

Consumers do not buy crude. They buy gasoline, diesel, and heating fuel. Diesel matters especially because it runs through freight, agriculture, logistics and industry. If diesel margins stay elevated, the pressure can move quickly from energy screens into transport costs and inflation expectations.

That is why central banks will not ignore this move if it lasts. A brief crude spike can be dismissed as temporary. A sustained rise in refined-product margins is harder to brush aside because it reaches the real economy faster.

Source: Data4poeple

OPEC’s demand warning complicates the rally

On one side, supply risk is back. U.S.-Iran tensions have returned, Hormuz is once again a market risk, inventories are low and fuel margins are already tight.

On the other side, OPEC has cut its 2026 global demand-growth forecast for the third month in a row, bringing it down to 780,000 barrels per day because of macroeconomic headwinds.

In a normal market, weaker demand forecasts would weigh on crude. But this is not a normal demand-led rally. It is a supply-risk rally landing on top of a tight physical backdrop.

That is why oil can rise even when the demand picture looks softer. Traders are not paying only for future consumption. They are paying for the risk that near-term supply confidence has been rebuilt too quickly.

Hormuz is back in the price

The Strait of Hormuz is once again the pressure point.

Even as Gulf production recovers and tanker traffic slowly returns, the market cannot fully ignore the risk of another disruption. A full closure is not the base case, especially after Oman agreed to keep access open from its side of the Strait. But oil does not need full closure to move higher. Higher insurance costs, delayed cargo, rerouted flows or fresh military risk around shipping lanes can be enough.

The new toll structure adds another layer. If vessels moving through Hormuz under U.S. protection face a 20% fee, the market will treat that as an added cost of maritime security. It may not stop crude from moving, but it can make every barrel passing through the region more expensive.

That is enough to bring a risk premium back into crude

This is what makes the latest 10% jump different from a normal momentum move. Oil is not simply reacting to stronger demand or speculative buying. It is reacting to a market that relaxed too quickly after earlier relief. Hormuz risk faded from the price, inventories stayed thin, and fuel margins were already stretched.