US yields face a new pressure point as Fed risk meets Japan intervention fears

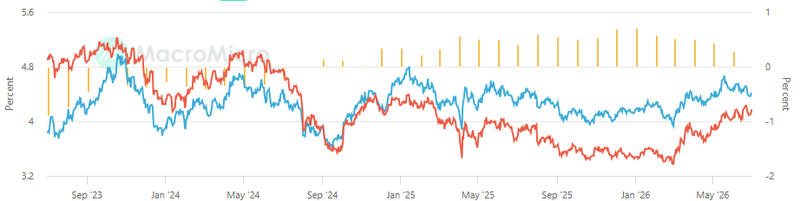

The yield curve remains relatively flat, with the 2-year yield near 4.18% and the 10-year yield around 4.46%. That small gap tells a bigger story. Short-term yields are being held up by the risk of another Fed hike, while long-term yields are carrying a premium for debt issuance, resilient growth and the possibility that foreign demand becomes less reliable.

The 2-year yield, near 4.18%, reflects the market’s concern that Fed policy may stay restrictive.

The 10-year yield of around 4.46% shows investors still want compensation for long-term risks.

A September Fed hike would likely put a firmer floor under short-term yields.

The yield curve is flat, but not calm

The narrow gap between the 2-year and 10-year yields shows that the Treasury market is caught between two different pressures.

At the front end, investors are still pricing the risk that the Fed may not be finished. If September rate-hike expectations continue to rise, the 2-year yield has little reason to fall meaningfully. It is the part of the curve most directly tied to the expected policy rate. So, if markets start revising the terminal rate higher, the front end becomes sticky. It does not need a major inflation shock to stay elevated. It only needs enough data to stop investors from pricing relief.

That is why the 2-year yield near 4.18% matters

It is not just a number. It reflects a market that is no longer confident the Fed can step back quickly. A September hike would reinforce that message and create a firmer floor under short-term yields. In that environment, every strong payroll print, every sticky inflation reading and every hawkish Fed signal becomes harder for the bond market to ignore.

Source: Trading economic

The 10-year yield is telling a different story

At 4.46%, it is not only tracking Fed expectations. It is carrying a longer-term risk premium. Investors are looking at sustained Treasury issuance, large fiscal deficits, resilient US growth and the possibility that inflation does not fall smoothly back to target. They are demanding more compensation to lend money to the US government for ten years.

A flat curve usually signals caution about future growth. But this is not a clean growth-scare curve. Long-term yields are still high because investors are also worried about supply and inflation persistence. In other words, the market is not saying the economy is collapsing. It is saying the government needs to borrow heavily, the Fed may stay restrictive, and investors want to be paid for holding duration.

Source: Trading economic

Japan turns yen defense into a Treasury risk

The second pressure is coming from outside the US, and it may become more important if USD/JPY keeps rising.

Japan remains one of the largest foreign holders of US government debt. For years, that position helped make Japanese demand a stabilizing force in the Treasury market. But if Japanese authorities are forced to defend the yen repeatedly, investors may need to think about Japan differently.

The question is not only whether Tokyo intervenes

The deeper question is what Tokyo has to sell if intervention becomes sustained.

To support the yen, authorities may need to use foreign reserves. A meaningful part of those reserves is held in US government bonds. One intervention operation may not change the Treasury market. But repeated intervention is different. If Japan becomes a more active seller of Treasuries to fund yen purchases, the pressure would not stay inside the foreign-exchange market. It could spill into US bonds.

That matters because the Treasury market is already dealing with heavy issuance. When supply is large, the market depends on steady demand from domestic investors, foreign reserve managers, banks, pension funds and asset managers. If one of the world’s largest foreign holders becomes less of a buyer, or more of a seller, investors may demand a higher yield to absorb the extra pressure.

Fed is already pressuring Treasury yields

The US yield curve may look flat, but the forces underneath it are not simple.

The 2-year yield is being held up by the risk of another Fed hike. A September move would likely keep short-term yields close to their cycle highs, especially if inflation and labour data remain firm. The 10-year yield is carrying a different burden: debt issuance, growth resilience, inflation uncertainty and the need for investors to absorb more duration.

The pressure is coming from both ends; the Fed is keeping the front-end firm. Debt supply and foreign-reserve risk are keeping the long end exposed.

That is why the Treasury market remains fragile. It is not only waiting for the next inflation report or Fed speech. It is also watching whether Japan’s currency problem becomes a US bond-market problem.

Source: MacroMicro