Warsh faces first Fed credibility test as markets price tightening

Kevin Warsh is starting his Fed chairmanship with a difficult contradiction. Oil prices have almost returned to pre-war levels, which should normally support the deflation trade. Yet markets are still pricing a meaningful chance of another rate hike by September. That tells us investors are no longer reacting only to energy inflation. They are trying to understand whether Warsh has changed the Fed’s reaction function.

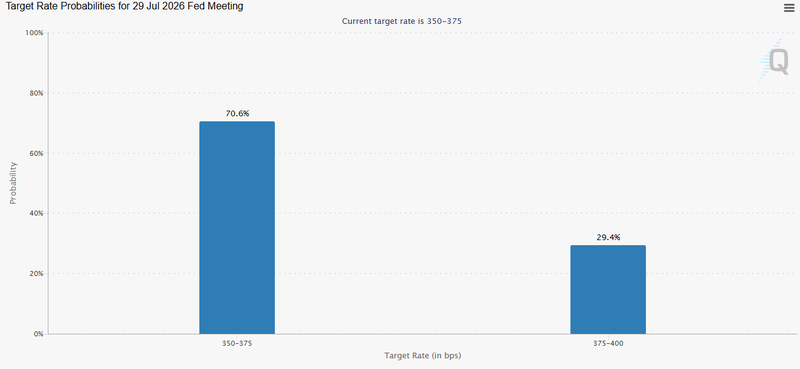

Markets see around 70% chance the Fed holds rates in July.

September still carries about a 61% probability of a rate hike.

NFP this week and CPI on July 14 are the next major tests for the deflation trade.

Markets are pricing a new Fed reaction function

The strange part of the current market setup is that Fed tightening expectations have risen while one of the clearest inflation shocks has faded.

The reopening of supply routes happened faster than markets expected. Oil prices are now almost back to where they were before the war began. Normally, that would help the deflation story. Lower oil reduces pressure on headline inflation, lowers inflation expectations, and gives the Fed more space to wait before tightening again.

But markets are not behaving as if the inflation problem has disappeared.

A July hold is still the base case, with probability around 70%. But the September meeting is different. A 61% probability of a hike shows that investors believe the Fed may still be willing to tighten later this year, even with energy prices falling sharply.

The market is not only pricing oil anymore. It is pricing Warsh

After his first meeting as Fed chair, investors seem to believe the Fed has become more willing to raise rates if the data stays firm. In other words, the inflation shock may be fading, but the policy reaction function may have become tougher.

Source: CME Group

Under a more guided Fed, softer energy prices might have been enough for traders to lean back into the deflation trade. Under Warsh, the bar is different. If the Fed communicates less and leaves markets to price decisions from the data, then every major release becomes more important. Markets cannot wait for the chair to guide them gently toward the next meeting. They must move ahead of the data.

This is why NFP and CPI now carry so much weight

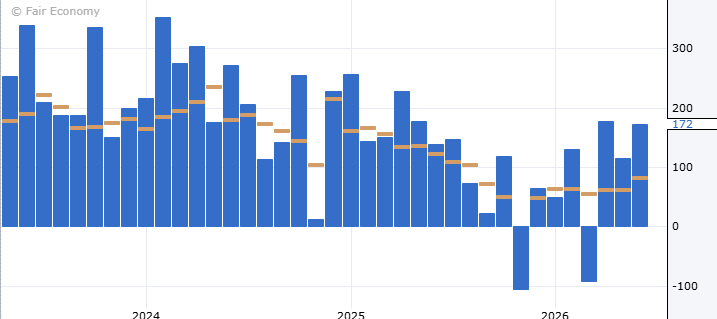

This week’s NFP report will test whether the labour market is cooling enough to reduce pressure on the Fed. Markets expect job growth to slow to around 114,000 from 172,000 previously, so the direction already points to some loss of momentum. But the details matter. If payrolls come in stronger than expected and wage growth stays firm, the market will read that as confirmation that September hike risk is real. A strong labour market gives the Fed room to stay restrictive, especially under a chair trying to rebuild inflation credibility.

Source: Forex factory

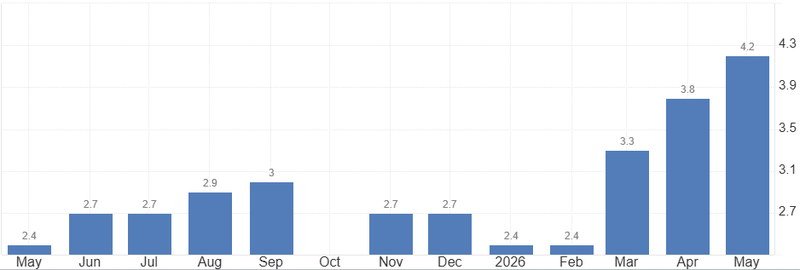

The July 14 CPI report is the bigger test for the deflation trade

Oil can help the headline number, but the Fed will be more focused on whether inflation pressure is cooling beneath the surface. If core inflation, shelter or services remain sticky, falling energy will not be enough to change the policy debate. In that case, markets may keep pricing a Fed that is willing to hike again.

But if NFP softens and CPI confirms broader disinflation, the current pricing could look too hawkish. That would challenge the idea that Warsh can keep the market focused on tightening when the data is moving in the opposite direction.

Source: U.S. Bureau of Labor Statistics

Warsh’s balance-sheet ambition faces a reserve problem

Rates are only one part of the story.

Warsh also wants the Fed’s balance sheet to be smaller. This week’s public remarks will matter because investors want to know how serious he is about shrinking it, and how quickly he thinks the Fed can move.

The idea is simple in principle. A smaller balance sheet means the Fed has a smaller footprint in financial markets. It also fits Warsh’s broader view that central banks should not provide too much liquidity for too long.

The biggest hurdle reserves in the banking system. The Fed cannot shrink the balance sheet without thinking about how many reserves banks need for money markets to function smoothly. The memory of 2019 still matters. Back then, reserve scarcity created stress in short-term funding markets and forced the Fed to step in. Since COVID, that episode has shaped balance-sheet management.

That is why the Fed must be careful

If Warsh pushes too hard, the market may not see it as discipline. It may see it as a liquidity risk. A smaller balance sheet can tighten financial conditions even without another rate hike. That matters at a time when markets are already pricing September tightening and waiting for NFP and CPI.

He has one vote out of twelve. He may be chair, but he still needs the committee. If he wants to reshape the Fed, he must persuade other officials that smaller reserves and less guidance will not create unnecessary market stress. That will not be easy if he starts with limited credibility inside the committee.

Less guidance can make the Fed look more disciplined. But it can also leave markets guessing. And when markets guess, they often price the risk first and wait for clarification later. That may be why rate expectations have moved higher even as oil prices have fallen.