Why is one CPI report not enough for the Fed

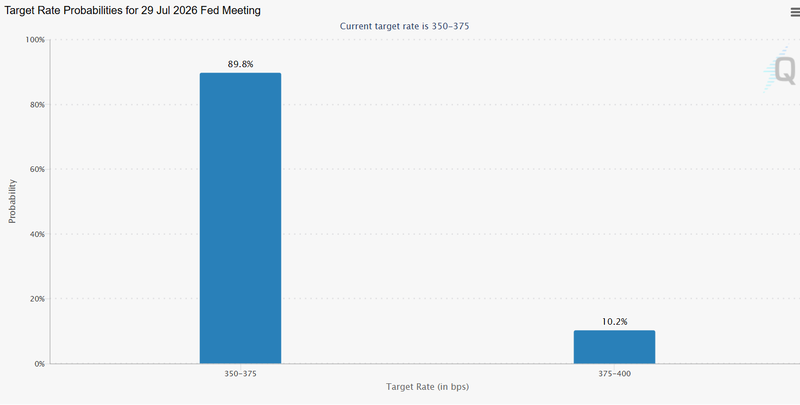

June's inflation report gave markets exactly what they wanted. Headline inflation came in softer than expected, and traders quickly moved to price a much lower chance of another rate hike. By the end of the week, futures were implying roughly an 90% probability that the Federal Reserve will leave rates unchanged in July, a sharp shift from what had looked like a genuine coin toss only days earlier.

Markets now see July as a likely pause after the softer June CPI.

The July inflation report may be the first to reflect higher oil prices.

Fed Chair Kevin Warsh continues to argue that one inflation report is not enough to change policy.

The market heard "pause"

The June CPI report gave investors the excuse they were looking for. Softer inflation immediately pushed Treasury yields lower, rate-hike expectations faded, and markets moved quickly to price a much more patient Fed. The probability of rates staying unchanged at the next meeting jumped to around 90%, roughly 70% before the release. One inflation report was enough to change the conversation.

June inflation was measured before oil prices surged again. Since then, renewed tensions between the United States and Iran have lifted crude sharply, bringing fuel costs back into focus. If those higher prices persist, the July CPI report, due in mid-August, could look very different. Markets may already be celebrating an inflation trend that has yet to survive its next test.

Source: CME Group

July could tell a different story

The next inflation report matters far more than the last one.

Energy prices rarely feed through immediately, but they eventually show up in transport costs, logistics, manufacturing and, ultimately, consumer prices. If crude remains elevated through July, some of that pressure is likely to begin appearing in the next CPI release.

That leaves markets in an awkward position. Investors have largely embraced the idea that inflation is heading steadily lower.

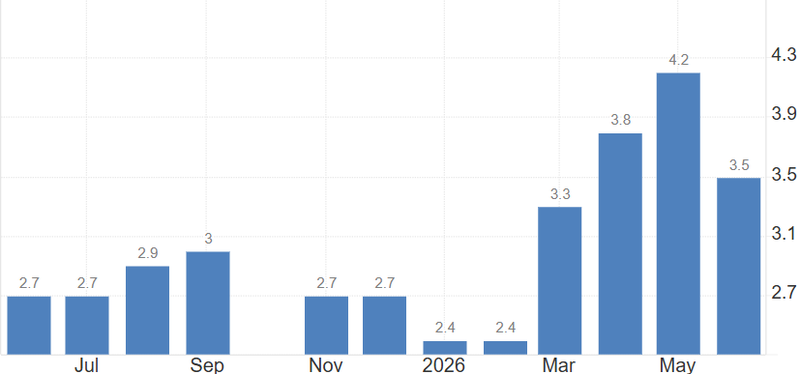

Source: U.S. Bureau of Labor Statistics

Trump wants lower rates. The Fed is not ready

Trump believes the Fed has already done enough. He has argued that holding rates steady is preferable to another hike and said he expects inflation to be lower by the end of the year, creating room for eventual rate cuts.

However, Kevin Warsh is sending a different message. He refused to rule out further tightening when questioned by lawmakers, but he also refused to promise another hike. Instead, he returned to what has become the Fed's central argument: one month's data changes very little.

Calling the June CPI report "just one datapoint," Warsh warned against cherry-picking favourable numbers while inflation remains above target. His focus is not the next market reaction but protecting the Fed's credibility if inflation proves more persistent than expected.

That is where the gap opens between Wall Street and the Federal Reserve. Investors are already pricing a prolonged pause. The Fed is still waiting to see whether June was the beginning of a trend or simply a temporary improvement.

The Fed's challenge is changing

A few months ago, the question was whether inflation was still accelerating.

The labour market has cooled without collapsing, but energy prices are rising again, and services inflation has not disappeared. That combination makes the next few months far more complicated than the June CPI report alone suggests.

If July inflation stays soft despite higher oil prices, confidence that the Fed has finished tightening will grow quickly.

If it doesn't, markets may have to abandon the idea that lower inflation automatically means easier monetary policy. The Fed has already made it clear that it is more comfortable keeping rates high for longer than declaring victory too early.