Yen intervention could hit harder as Japan’s flows turn supportive

Japan’s currency backdrop is shifting in favor of the yen. Trade and investment flows have turned positive this year, speculative short positions remain near record levels, and the yen is deeply undervalued by purchasing-power measures. That mix could make any future intervention by Japanese authorities more effective than previous attempts to support the currency.

Japan’s trade and investment flow balance has turned positive this year.

The flow balance is at its highest level since at least 1996.

The yen is about 50% undervalued versus purchasing-power parity.

Japan spent a record ¥11.73 trillion on intervention through May 27.

Yen support may be stronger this time

Japan’s authorities may have a more favorable backdrop if they decide to step into the foreign-exchange market again to support the yen.

The key change is in Japan’s trade and investment flows. The 12-month rolling balance of goods and services trade, direct investment and portfolio investment has turned positive this year. That is important because a positive balance usually creates natural demand for the yen.

It can mean exporters are converting more foreign-currency proceeds back into yen. It can also mean Japanese investors are selling fewer yen to buy overseas assets, or that foreign investors are creating more yen demand as they buy Japanese bonds and stocks.

This flow balance has climbed to its highest level since at least 1996, based on Bloomberg-compiled data. That suggests the currency is no longer being driven only by interest-rate differentials, which have been one of the main arguments behind bearish yen positioning.

A possible weakness in the yen-bear case

The yen has been under heavy pressure because Japan’s interest rates remain low compared with other major economies. That rate gap has encouraged investors to borrow or sell yen and buy higher-yielding currencies.

But the flow data points to a potential weakness in that bearish case.

If Japan’s external flows are becoming more supportive, then the yen may have a stronger base than rate differentials alone suggest. That could make intervention more powerful because official yen buying would be working with a more favorable underlying flow trend, rather than fighting against it.

Still, the relationship is not perfect. Trade and investment flows often affect currency markets with a lag, and they do not move one-for-one with exchange rates. But the direction of travel matters, especially when positioning is already stretched.

Hedging flows can limit yen strength — or amplify it

One important complication is hedging.

A large share of foreign inflows into Japanese bonds and equities may be hedged. That means foreign investors buying Japanese assets may also sell yen forward to protect themselves from currency risk. In the short term, those hedges can limit upward pressure on the yen.

But hedging can work in both directions.

If the yen starts to rally, investors who had hedged by selling yen may unwind those positions. That creates yen buying and can accelerate the move. In that scenario, what initially looked like a drag on yen strength could become fuel for a larger rally.

This is why intervention risk matters when speculative positioning is crowded. A sudden official push can force investors to reassess hedges and bearish currency bets at the same time.

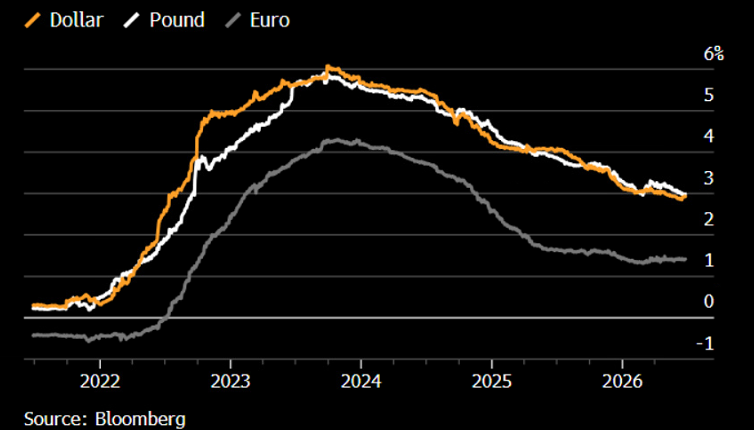

Hedging returns have fallen from 2023 peaks

The incentive to stay short yen through hedged positions has also weakened.

The yield from three-month yen hedges has fallen sharply from its 2023 peaks. It now stands at about 3% for dollar- and pound-based investors and around 1.4% for eurozone investors.

Source: Bloomberg

Those returns may still be attractive, but they are less compelling than they were at the height of the yen carry trade. The question for investors is whether the remaining carry is enough to justify continued bearish yen exposure at a time when valuations are stretched and intervention risk is rising.

As hedging returns shrink, the risk-reward balance for betting against the yen becomes less one-sided.

Yen valuation looks extremely stretched

Valuation is another reason the yen-bear trade may be vulnerable.

The yen is about 50% undervalued against the level implied by the difference in wholesale inflation between Japan and the US. That points to the most extreme overselling of the currency in Bloomberg-compiled data going back to 1982.

This does not mean the yen cannot weaken further. Currency markets can stay stretched for long periods, especially when interest-rate gaps remain wide.

But it does mean the asymmetry is changing. When a currency is this undervalued, the downside case becomes more dependent on momentum and carry, while the upside risk from intervention, short covering or a shift in flows becomes more dangerous.

That gives Japanese authorities a stronger argument if they choose to intervene.

Officials keep intervention threat alive

Japan has continued to warn markets that action remains possible.

Finance Minister Satsuki Katayama spoke by phone with US Treasury Secretary Scott Bessent last week and said both countries shared a clear understanding that bold action should be taken if necessary.

That language keeps the threat of intervention alive. It also matters because coordination, or at least understanding from the US side, can affect how markets interpret Japan’s willingness to act.

Japan’s Ministry of Finance has already shown it is prepared to spend heavily. It spent a record ¥11.73 trillion on intervention in the month through May 27.

That scale signals that authorities are not treating yen weakness as a minor issue. If they intervene again, markets will likely assume they are prepared to use significant firepower.

Crowded short yen trades raise squeeze risk

Positioning may be the most explosive part of the setup.

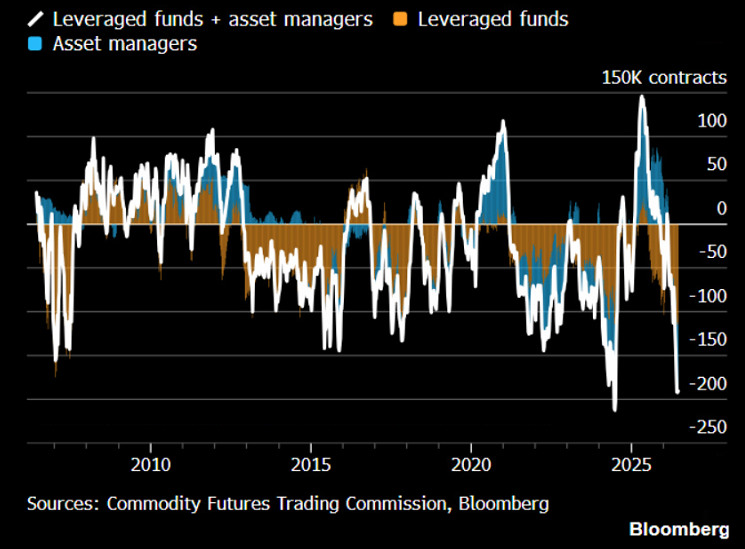

Hedge funds and asset managers together hold near-record bearish wagers on the yen, according to the latest Commodity Futures Trading Commission data. When short positions are this crowded, a sharp yen rally can force investors to close trades quickly.

Source: Bloomberg

That is how a short squeeze starts.

If authorities intervene while flows are turning supportive and valuation is already stretched, short yen positions could unwind rapidly. Investors who sold the yen for carry may be forced to buy it back, creating a feedback loop that pushes the currency higher.

This does not guarantee a sustained yen rally. But it does increase the risk that any move triggered by intervention becomes larger than expected.