Daily discussion thread for July 14, 2026

US inflation cooled more than expected in June, easing immediate Federal Reserve interest rate hike fears and lifting US equities. Meanwhile, robust Chinese trade data supported global growth optimism, while Japan’s industrial production contracted unexpectedly, signalling renewed manufacturing weakness.

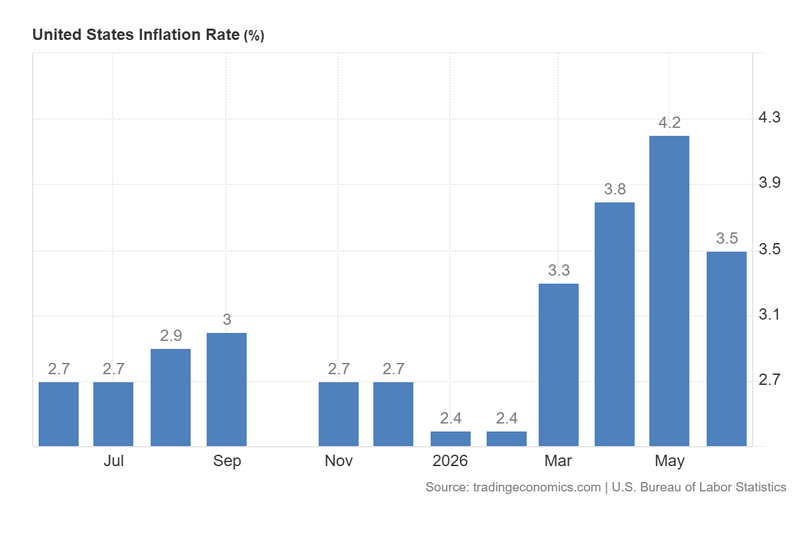

US headline inflation slowed to 3.5% in June, undershooting consensus forecasts and lowering expectations of an immediate interest rate hike by the Federal Reserve.

China’s trade surplus expanded to $125.62 billion, driven by export (+27%) and import (+36%) growth that significantly outpaced market expectations.

Japan’s industrial production contracted by 2.1%, marking the first decline in six months and highlighting underlying vulnerability in the manufacturing sector.

US inflation rate decelerates below analyst forecasts

According to data from the US Bureau of Labor Statistics, the headline year-on-year inflation rate decelerated from 4.2% in May to 3.5% in June, undershooting market forecasts which had anticipated a 3.8% level. The current reading represents the lowest level in three months, effectively reducing the probability of an immediate interest rate hike by the Federal Reserve at its upcoming July meeting. Concurrently, according to the CME FedWatch Tool, the market-implied probability of a rate increase at the September meeting now stands as the predominant likelihood at 50%, marking a significant decline from recent days when the probability exceeded 70%.

An analysis by Trading Economics indicates that the deceleration in headline inflation was primarily driven by an easing in energy costs, which slowed from a year-on-year rate of 23.5% in May to 15.7% in June. This moderation followed the US-Iran ceasefire agreement, which had begun to normalise energy flows through the Strait of Hormuz, resulting in a 5.7% contraction in monthly energy prices. Meanwhile, core inflation—which excludes the volatile components of energy and unprocessed food—eased from 2.9% to 2.6% over the same period.

Concurrently, the US Federal Reserve Chairman Kevin Warsh declared that the Fed’s objective remains to bring inflation back to the 2% target, independently of White House pressures for lower borrowing costs. Testifying before Congress, Chairman Warsh strongly defended the central bank’s independence and expressed confidence regarding future economic performance. Market participants are now closely monitoring the geopolitical dynamics of the US-Iran conflict in the Middle East to assess how current instability within this key maritime corridor develop in the coming days and weeks, given its direct impact on crude oil prices.

Following the economic releases, US benchmark equity indices rose in tandem. The S&P 500 index advanced by 0.38% to close at 7,543 points, the Nasdaq 100 increased by 1.10% to 29,586 points, while the Dow Jones Industrial Average appreciated marginally by 0.02% to finish at 52,513 points. Conversely, the US Dollar Index (DXY) declined by 0.33% to 100.94 points as expectations of a more restrictive monetary policy stance by the Federal Reserve softened.

Figure 1. US Inflation Rate (2025-2026). Source: Data from the US Bureau of Labor Statistics; Figure obtained from Trading Economics.

China’s balance of trade increases amid rising exports and imports

The General Administration of Customs of China reported that the nation's trade surplus expanded firmly from $105.43 billion in May to $125.62 billion in June, surpassing analyst estimates of $121 billion. This current level represents the highest surplus recorded since January 2025, signalling significant momentum for Chinese international trade. The report revealed that the surplus was underpinned by a 27% year-on-year increase in exports, alongside a 36% surge in imports—with both metrics comfortably exceeding market expectations. Furthermore, the data indicated that the prominent improvement in exports was heavily driven by rising global demand for artificial intelligence (AI) data centre hardware.

In response to the trade data, the FTSE China A50 index rose by 1.91% to 15,076 points, while the Hang Seng index advanced by 0.65% to close at 24,357 points.

Japanese industrial production marks first contraction in six months

According to data released by the Ministry of Economy, Trade and Industry (METI) of Japan, industrial production fell by 2.1%, down sharply from the previous reading which had shown an acceleration of 2.0%. The current figure marks the lowest level since November 2025, reflecting a complex operating environment for Japanese industry. An analysis by Trading Economics highlights that the most pronounced declines occurred within general-purpose and business-oriented machinery, which fell from 4.4% to –6.0%; electrical machinery and information and communication electronics equipment, which dropped from 2.7% to –5.1%; and production machinery, which slid from 0.4% to –3.5%.

However, following the updates, the Nikkei 225 equity index appreciated by 0.74% at 67,743 points, while the Japanese yen strengthened marginally by 0.15% to trade at ¥162.20 per US dollar.