Daily discussion thread for July 15, 2026

Middle East tensions remained elevated, supporting crude oil prices despite limited overall gains. Concurrently, China’s activity data showed marked improvement, the Bank of Canada held interest rates steady, and a softer US producer price inflation reading eased upward pressure on the US dollar.

Brent crude rose by 0.26% and WTI by 0.28% as escalating US-Iran tensions and associated energy supply risks kept market participants on high alert.

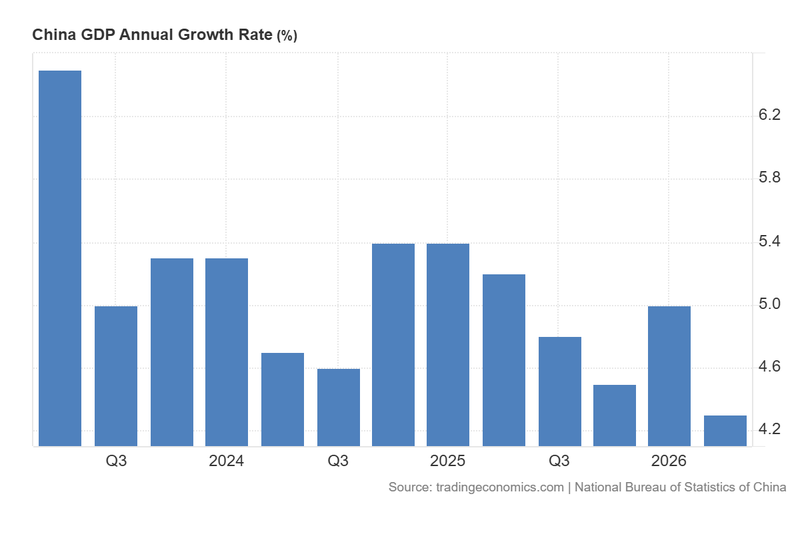

China’s industrial output advanced by 5.3% and retail sales expanded by 1.0% year-on-year, though second-quarter GDP growth slowed to a modest 0.9%.

The Bank of Canada maintained its benchmark interest rate at 2.25% amidst a complex backdrop of rising inflation, stagnant growth, and geopolitical uncertainty.

US PPI slowed to 5.5% year-on-year, printing below market forecasts, which helped lift the S&P 500 and weighed on the US Dollar Index (DXY).

Geopolitical tensions persist in the Middle East, but oil prices advance slightly

Geopolitical friction between the United States and Iran remains highly elevated in the Middle East. According to Reuters reports, the US has imposed a naval blockade on Iranian ports following targeted strikes against coastal defences and missile sites. In response, Tehran has threatened to halt regional energy exports, characterising the stand-off as an "existential war" with Washington. In turn, Iran has launched attacks against US military installations in several Middle Eastern countries. This rhetoric highlights how the ongoing escalation could result in a prolonged conflict if both parties maintain an offensive posture.

Furthermore, the US continues to warn of potential subsequent military action if Iran does not return to the negotiating table. Conversely, Tehran maintains that a balanced agreement cannot be achieved under the duress of active threats. Given the current instability, commodity analysts warn of potential complications regarding the Red Sea corridor in Yemen—a vital maritime shipping route for global energy supply chains. Should Iran’s Houthi allies engage more directly in the conflict, the threat of a severe energy supply disruption could significantly worsen the current market environment.

At the market close, global oil benchmarks Brent and WTI recorded marginal appreciations. The Brent crude futures contract (BRNU6) advanced by 0.26% to settle at $84.95 per barrel, while the West Texas Intermediate futures contract (CLQ6) rose by 0.28% to close at $79.57 per barrel.

China’s industrial production and retail sales accelerate, but GDP growth rate eases

Chinese macroeconomic indicators delivered mixed signals, characterized by accelerating industrial production and retail sales alongside a moderating Gross Domestic Product (GDP) growth rate. According to data released by the National Bureau of Statistics of China, industrial production advanced from 4.5% in May to 5.3% in June on a year-on-year basis, outperforming the analyst consensus forecast of 4.6%. Concurrently, retail sales recovered from a prior contraction of 0.6% to expand by 1.0% over the same period, suggesting that domestic consumer demand may be exhibiting early signs of a turnaround.

However, aggregate growth faced headwinds as the second-quarter GDP growth rate decelerated. The official report indicated that the Chinese economy expanded at a rate of 0.9% in Q2, down from the 1.3% growth recorded in Q1, marking the lowest quarterly expansion since Q2 2024. The data suggests that soft domestic demand and consumer confidence anxieties—compounded by the geopolitical instability in the Middle East—served as the primary detractors from growth.

Nevertheless, following the macroeconomic releases, Chinese equity indices rallied in tandem as market participants prioritised the stronger industrial and retail figures over the softer GDP print. The FTSE China A50 index advanced by 1.06% to 15,232 points, while the Hang Seng index appreciated by 1.27% to close at 24,658 points, supported by ongoing expectations of government stimulus to cushion the wider economy.

Figure 1. China GDP Annual Growth Rate (2023-2026). Source: Data from the National Bureau of Statistics of China. Figure obtained from Trading Economics.

BoC maintains steady interest rates in line with market expectations

The Bank of Canada (BoC) elected to keep its benchmark interest rate unchanged at 2.25%, matching consensus analyst forecasts. The domestic Canadian economy continues to feel the secondary effects of the ongoing conflict in the Middle East, as well as broader geopolitical friction involving the US, which has clouded forward-looking economic projections.

Although the domestic unemployment rate has retreated to 6.5% since peaking at 7.1% in September 2025, first-quarter GDP growth completely stagnated at 0%. Meanwhile, the headline inflation rate accelerated to 3.2% in May, remaining visibly above the BoC’s official 1% to 3% target range. This stagflationary combination complicates future policy options for the Canadian central bank, which chose not to provide explicit forward guidance regarding its upcoming monetary policy decisions due to prevailing economic and geopolitical uncertainties. At the closing bell, the Canadian dollar appreciated by 0.19% against the greenback, with the USD/CAD currency pair settling at 1.4032.

US PPI decelerates below forecasts

The US Bureau of Labour Statistics (BLS) reported that the Producer Price Index (PPI) eased from 6.0% in May to 5.5% in June, undershooting the market consensus forecast which had anticipated an increase to 6.2%. The report highlighted that the disinflationary print was primarily driven by a sharp 12% monthly decline in gasoline prices. This drop appears tied to the temporary US-Iran ceasefire period, which had successfully normalised energy transit through the crucial Strait of Hormuz.

However, the primary concern for forward looking models is how factory-gate prices will react in the upcoming July reading to the renewed escalation in the US-Iran conflict, which has driven crude oil benchmarks up by approximately 20% over the last fortnight.

Following the inflation update, US equity benchmarks closed the session mixed: the S&P 500 index appreciated by 0.38% to 7,572 points and the Dow Jones Industrial Average rose by 0.29% to 52,664, whereas the technology-heavy Nasdaq 100 index fell by 0.28% to close at 29,502. In the currency markets, the US Dollar Index (DXY) experienced downward pressure, dropping by 0.45% to finish the session at 100.48 points.