DXY surge reflects a Fed regime shift more than a simple rally

The dollar’s move is no longer just a reaction to stronger US data. DXY trading at a 52-week high suggests markets are starting to price a deeper policy shift after Kevin Warsh’s debut remarks. His focus on price stability, rejection of forward guidance, and cautious stance on future decisions are changing how investors think about the Fed’s reaction function.

DXY is trading at a 52-week high.

Warsh emphasized price stability and rejected forward guidance.

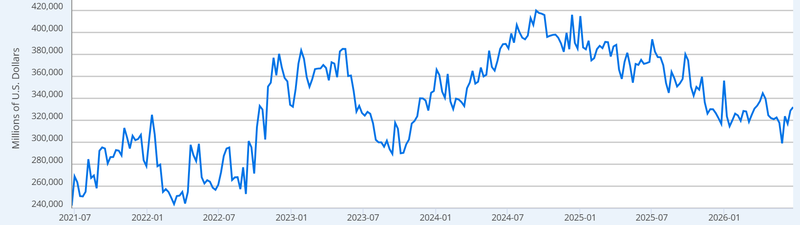

Foreign central banks still hold about $315 billion in the Fed’s Foreign Repo Pool.

The dollar is pricing a different Fed

The closest historical parallel is not 2018 or 2022. Those were tightening cycles. This looks more like a possible change in doctrine.

When Paul Volcker took over the Fed in 1979, the market did not immediately understand that the rules had changed. Investors kept looking for a policy reversal because they were used to a Fed that would eventually protect growth and markets. But Volcker’s priority was different. He made price stability the centre of the framework, and it took months for investors to fully accept that the Fed’s purpose had shifted.

Warsh is not Volcker, and today’s inflation backdrop is different

But the market reaction is similar in one important way: investors are trying to decide whether this is just another Fed cycle, or the start of a different operating style.

His first message was clear enough. Price stability comes first. The Fed should not overuse forward guidance. Future decisions will depend on data, not pre-committed signals. That kind of Fed is harder for markets to lean against. It gives less comfort. It allows rates and the dollar to adjust more freely.

The Foreign Repo Pool shows dollar demand is still defensive

The $315 billion still sitting in the Foreign Repo Pool matters because it represents risk-free dollar cash parked directly at the Federal Reserve by foreign central banks and official institutions. That is not speculative money chasing a trade. It is official-sector liquidity management.

When DXY accelerates to a 52-week high, foreign central banks face a more difficult environment. Their local currencies weaken, imported inflation pressure rises, and intervention risk increases. The Japanese yen is the clearest example. A stronger dollar pushes USD/JPY higher, forcing markets to ask whether Tokyo will have to defend the currency again.

Source: FRED

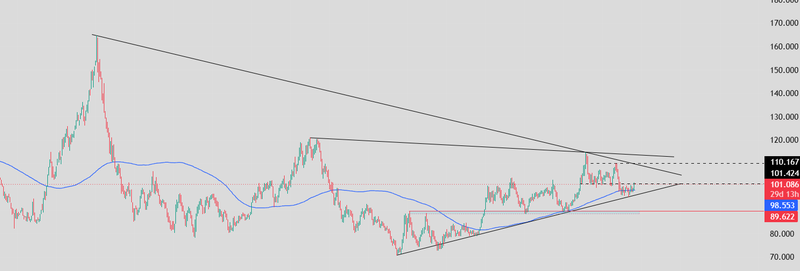

Technical outlook

DXY is at the point where the market needs to decide.

For months, the dollar has been moving inside a wide compression range. Sellers are still defending the broader downtrend that started from the 163 peak, while buyers have continued to build higher lows from the 72–75 area. That is why the chart matters now. The dollar is no longer moving freely in either direction. It is being squeezed between long-term resistance from above and steady demand from below.

Price is now trading around 101, near its 52-week high, and still sits above the 126-day moving average around 98.50. That keeps the recovery alive. But this is not yet a clean breakout. The dollar still needs to clear 101.40 with conviction before traders can say that buyers have taken control. Until then, this move remains a test of resistance rather than confirmation of a new bullish phase.

The bigger level is 110.20. That is where the long-term descending trendline meets previous swing resistance. If DXY reaches that area, the market will have to decide whether the dollar is only rebounding inside a larger downtrend or whether the structure is starting to change. A sustained break above 110.20 would be important because it would show that the old downtrend is losing influence.

On the downside, 98.50 is the first level that needs to hold. It is not just a moving average. It is the line that separates a healthy pullback from a failed recovery. If DXY loses 98.50 and slips below the rising trendline, the recent sequence of higher lows would start to break down. That would put 95 back in focus first, followed by 89.60, the level where buyers have returned several times over the past year.

Scenarios ahead

The stronger scenario starts with DXY holding above 98.50 and breaking through 101.40. That would suggest the market is no longer only defending support but starting to build pressure for a larger upside move. In that case, 110.20 becomes the real test. A move above that level would mark a meaningful shift in structure and could confirm that the dollar is moving out of consolidation.

The weaker scenario begins with failure below 98.50. If that happens, the market would likely treat the latest recovery as another failed attempt to break the broader downtrend. The first move could be toward 95, but the more important test would be 89.60. A break below that area would put sellers firmly back in control.

For now, DXY is not giving a final answer. It is compressed, and that usually means the next move matters more than the last one. The dollar is either preparing to break out of a long period of hesitation, or it is about to prove that the broader downtrend still has control.

Source: Trading view