NFP report puts Fed policy in focus

The US Non-Farm Payrolls report may not decide the Federal Reserve’s next move on its own, but it could determine how much room policymakers have to keep focusing on inflation.

US payrolls are expected to rise by around 85,000 in May.

The unemployment rate is seen holding at 4.3%.

Wage growth is expected at 0.3% month over month.

NFP becomes a key test for Fed policy

The US Non-Farm Payrolls report is back at the center of market attention, but the meaning of the data has changed.

Earlier this year, every soft labour-market print encouraged speculation that the Federal Reserve could begin cutting interest rates. That narrative has faded. Elevated oil prices, renewed energy-driven inflation concerns and a more cautious Fed have shifted the debate away from rate cuts and toward a more uncomfortable question: could inflation eventually force another rate hike?

That is why today’s NFP report matters for traders. The jobs data may not trigger an immediate Fed policy shift, but it can decide how much freedom the central bank has to stay focused on inflation. A resilient labour market gives policymakers more room to keep policy restrictive. A weaker labour market limits that room and could make officials more cautious.

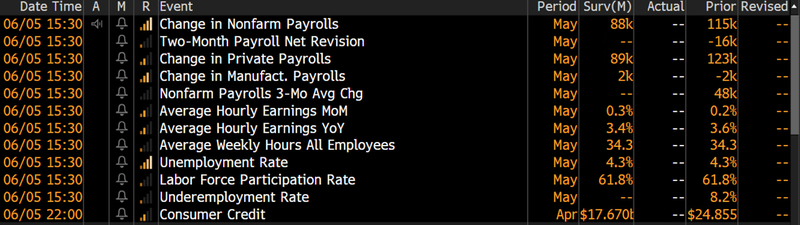

US jobs data expectations

Markets enter the report with expectations for moderate job growth, steady unemployment and slightly firmer wage gains.

Source: Bloomberg

The consensus points to a cooling, but not collapsing, labour market. That is an important distinction. A slower pace of hiring would not automatically weaken the Fed’s inflation concerns, especially with oil prices still threatening to keep headline inflation under pressure.

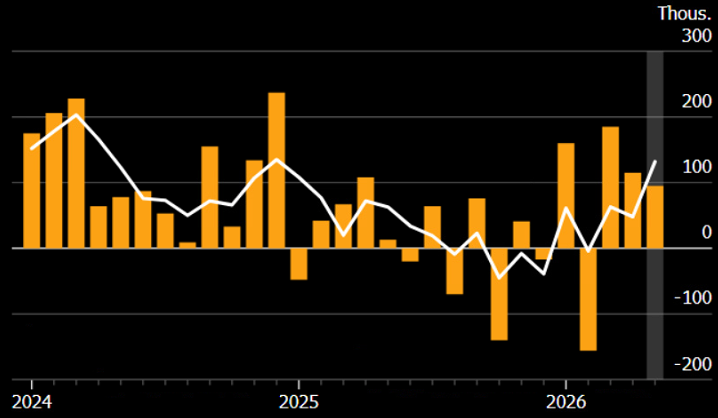

Scenario one: NFP comes close to expectations

A payrolls print near expectations would probably leave the Fed and markets in roughly the same position.

If job growth lands around the 85,000 to 96,000 range, unemployment holds at 4.3%, and average hourly earnings rise by 0.3% month over month, the report would confirm a labour market that is slowing but still stable.

Source: Bloomberg

That outcome would not give the Fed a strong reason to shift its tone. Policymakers would likely continue watching inflation developments, especially energy prices, while markets could maintain roughly balanced odds around the possibility of a rate hike later this year.

Scenario two: Strong jobs data supports a hawkish Fed

A stronger-than-expected NFP report would carry a more hawkish message, especially if it comes with faster wage growth or a lower unemployment rate.

Strong payroll growth alone would show that the US labour market remains resilient. But the real market reaction would depend on the details. If hiring accelerates while wages rise faster than expected, investors could conclude that inflation risks are becoming more persistent.

That combination would not guarantee another Fed rate hike, but it would make it easier for policymakers to maintain a tightening bias. It would also make it harder for markets to dismiss the risk of higher interest rates later this year.

Scenario three: Softer payrolls may not be enough for a Fed pivot

A softer NFP report would raise concerns about the economy, but it may not be enough to change the Fed’s policy direction.

A moderate miss in payrolls would likely make officials more careful about discussing future hikes. However, as long as unemployment remains stable and wage growth does not collapse, inflation concerns would remain the bigger issue.

The Fed is not only looking at labour-market weakness. It is also watching whether inflation expectations become harder to control. With oil prices elevated, a slightly weaker jobs report may reduce the probability of aggressive tightening, but it may not revive the rate-cut narrative.

A very weak report would change the market conversation

The most important downside scenario would be a genuinely weak labour-market report.

A negative payrolls print, a sharp rise in unemployment or a clear slowdown in wages would challenge the current market view that the next Fed move could still be higher. That kind of report would signal that growth risks are becoming harder to ignore.

In that case, rate-hike expectations could fall quickly, Treasury yields could move lower, and the dollar could come under pressure. Gold would likely find stronger support in that environment, especially if investors start rebuilding expectations for a more cautious Fed.

This is the only scenario that could meaningfully reopen the door to a more dovish policy debate.

Why Gold traders should watch the Fed reaction, not only the headline number

The headline NFP number matters, but the Fed reaction function matters more.

Gold’s next breakout will depend on whether the jobs report gives the Fed enough confidence to keep fighting inflation or forces policymakers to acknowledge rising labour-market risk. Strong employment gives the Fed room to stay hawkish. Weak employment narrows that room.

That makes wage growth and unemployment just as important as the payrolls number itself. A solid jobs print with firm wages would support higher-for-longer policy expectations. A soft payrolls number with stable wages may produce only a limited market reaction. A broad labour-market deterioration would be the clearest bullish signal for Gold.

Source: TradingView

Gold outlook: inflation hedge or rate-sensitive asset?

Gold is currently caught between two powerful forces.

On one side, energy-driven inflation and geopolitical uncertainty can support demand for Gold as a hedge. On the other side, higher Treasury yields and a stronger dollar can limit upside momentum. This is why today’s NFP report is so important: it may decide which force dominates in the short term.

If the data strengthens the case for a hawkish Fed, Gold may struggle to extend gains. If the data weakens rate-hike expectations, Gold could regain momentum. If the report lands close to expectations, traders may quickly shift attention back to oil prices, inflation data and Fed commentary.