Could Japan's credit squeeze spark the next carry trade shock?

Japan’s exit from ultra-loose policy is no longer only a domestic rates story. It’s starting to change credit pricing, yen funding and the risk of a disorderly carry trade unwind. The Bank of Japan is trying to normalise policy gradually, but markets are already testing what happens when an economy built around cheap money begins to face higher funding costs.

Q3 will test how much tightening Japan’s weaker borrowers can absorb.

Japanese yields have reached 30-year highs, while the US-Japan 10-year yield spread has narrowed to around 1.69%, its lowest level since 2022.

Q3 is likely to bring another BoJ rate hike to around 1.25%.

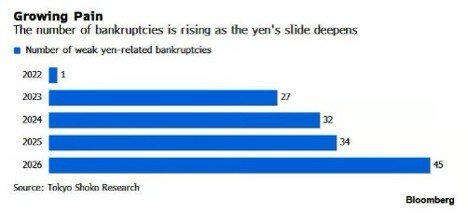

Credit risk is returning to Japan

After raising its policy rate to 1% in June, the Bank of Japan is making borrowing less effortless than it once was. Officials including Naoki Tamura are still arguing that rates should move gradually toward a neutral level near 2%, meaning companies can no longer assume capital will stay extremely cheap.

The pressure is already showing. Between January and June, 45 Japanese companies declared bankruptcy due to currency depreciation. That was a 32.3% increase from a year earlier and the highest first-half total in four years.

This is not a broad corporate crisis yet, but it is a clear warning. A weaker yen is lifting import costs, while higher rates are making refinancing more expensive. Smaller firms, importers and highly indebted borrowers are likely to feel the squeeze first. That is usually how credit stress begins. Not with the strongest companies, but with firms facing thin margins, weak pricing power and limited access to cheap refinancing.

Q3 will test how much tightening Japan’s weaker borrowers can absorb. If the BoJ hikes again while the yen stays under pressure without intervention, credit risk could move from a slow repricing into a more visible market concern.

Source: Tokyo Shoko Research

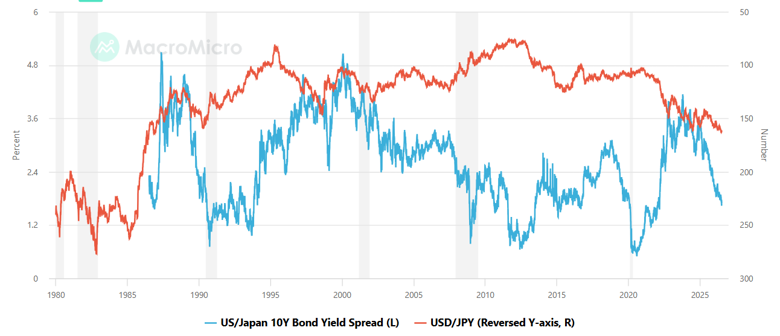

The end of easy yen funding

For years, the yen made the carry trade straightforward. Investors could borrow cheaply in Japan and invest that money in higher-yielding markets overseas. It worked because Japanese interest rates stayed close to zero and global appetite for risk remained strong.

That backdrop is starting to change. Japanese yields have reached 30-year highs, while the US-Japan 10-year yield spread has narrowed to around 1.69%, its lowest level since 2022. As that gap shrinks, borrowing in yen and taking currency risk elsewhere becomes less attractive. A gradual unwind would likely be manageable. But if the yen strengthens quickly or markets start pricing in another BoJ rate hike more aggressively, leveraged carry trades could unwind much faster.

Japanese pension funds, insurers and asset managers also play an important role. As domestic yields become more attractive, more capital could stay in Japan instead of flowing overseas. That would reduce demand for the global bonds and risk assets that have benefited from years of cheap yen funding.

Source: MacroMicro

Currency intervention risk is rising

A weaker yen supports exporters, but it also raises import costs and puts more pressure on households and smaller businesses. If the currency weakens further, especially towards levels officials consider excessive, the risk of intervention will rise again. Policymakers would likely begin with verbal warnings, but markets know Japan can step in directly if volatility becomes disorderly.

The opposite risk matters too. A sharp rally in the yen, driven by a carry trade unwind, could tighten global financial conditions quickly. That would not be a normal currency move. It would be a forced adjustment in funding markets.

Q3 is likely to bring another BoJ rate hike to around 1.25%, while the US-Japan 10-year yield spread is likely to remain under pressure. There is also a growing likelihood of real FX intervention, rather than just verbal warnings. If yen weakness continues to push up import costs and add to credit stress, policymakers may have little choice but to tighten policy while also stepping into the currency market. That combination would increase the risk of a sharper carry trade unwind, especially if leveraged investors are forced to cut yen-funded positions quickly.