Amazon vs SpaceX: which stock has the stronger investment case?

Amazon and SpaceX are both trying to own the next layer of global infrastructure, but they are very different investments. Amazon is the more mature business. It has multiple profit engines, including AWS, advertising, subscriptions and e-commerce scale. SpaceX is the more explosive growth story, built around Starlink, launch dominance, defense contracts, and a much bigger long-term vision tied to satellites, AI infrastructure and space logistics.

SpaceX depends heavily on Starlink as its main profit engine.

Amazon has several mature cash-flow sources, led by AWS.

Starlink is far ahead of Amazon Leo in satellite scale and customer adoption.

SpaceX has the stronger growth story

SpaceX’s advantage starts with execution.

Starlink has become the clear leader in satellite internet. With more than 10,000 active satellites in orbit and over 12 million customers globally, SpaceX is not just building a future network. It already has one. That gives the company a major first-mover advantage in low-earth-orbit internet, especially in areas where traditional broadband is weak, expensive or unavailable.

This matters because Starlink is not a side project anymore. It is becoming the profit engine that helps support the rest of SpaceX. Launch services, Starship development, defense contracts and AI infrastructure are all capital-heavy areas. Starlink gives SpaceX something many aerospace companies never had: a recurring consumer and enterprise revenue stream.

That is why investors are willing to pay attention. SpaceX is not only a rocket company. It is becoming a global connectivity company with aerospace economics on one side and subscription economics on the other.

But that creates risk

If Starlink is carrying much of the profit story, then SpaceX depends heavily on one segment to fund several expensive ambitions at the same time. Building rockets, satellites, launch systems and AI infrastructure is not cheap. The company may have huge upside, but it also has a high demand for capital.

That makes valuation more sensitive. If Starlink keeps scaling, the stock can justify a premium. If growth slows or margins come under pressure, investors may start asking whether SpaceX is trying to fund too many moonshots at once.

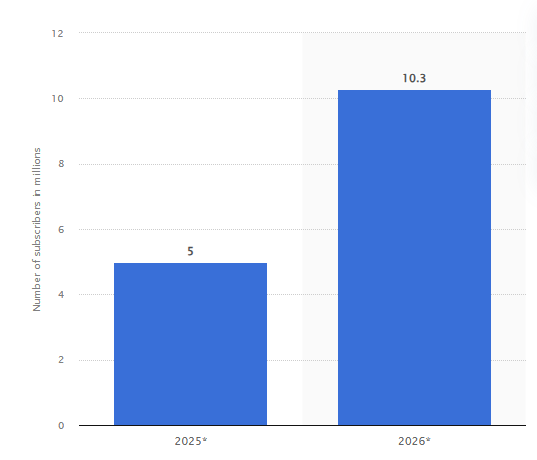

Source: Statista

Amazon has a stronger financial base

Amazon’s case is different. It is not as clean or exciting as SpaceX’s growth story, but it has something SpaceX does not have on the same scale: multiple established profit engines.

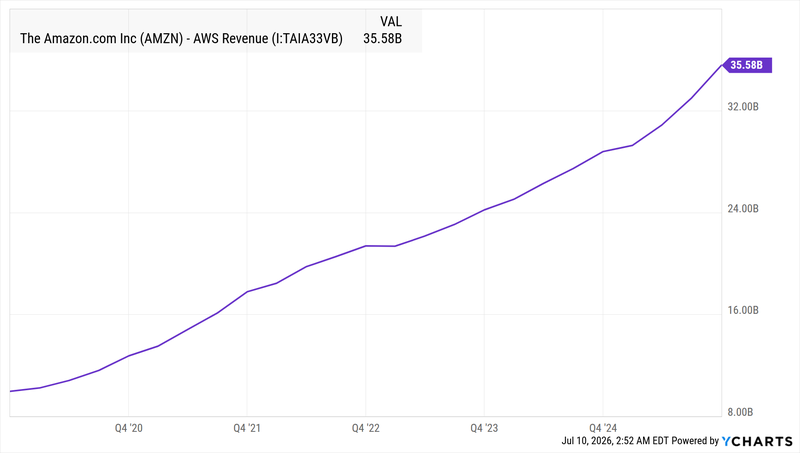

AWS remains the centre of Amazon’s earnings power, with revenue reaching a record $35.59 billion. That gives Amazon a deep cash-flow base to fund its aggressive push into artificial intelligence infrastructure. The company’s planned $200 billion investment in AI and data-centre capacity is enormous, but it is backed by a business model that already produces serious operating income.

Source: Ycharts

Biggest difference between Amazon and SpaceX

SpaceX is using Starlink to support a wider infrastructure empire. Amazon is using AWS, advertising, retail scale and enterprise relationships to fund its next cycle of AI growth. The funding base is broader, more mature and less dependent on one segment.

Amazon Leo is still behind Starlink. With more than 390 satellites in orbit, it has crossed an important milestone, but it remains far smaller than SpaceX’s satellite network. Amazon is not winning the satellite race today.

Leo can strengthen Amazon’s cloud, logistics, enterprise connectivity and government-services ecosystem over time. It can become another layer around AWS rather than a standalone profit engine from day one. That gives Amazon more flexibility. It can afford to be patient because the core business is already large and profitable.

The strategic difference is simple

SpaceX is building for a multi-planetary future. Amazon is building deeper infrastructure on Earth.

That difference shapes the investment case. SpaceX offers a more dramatic upside if Starlink, Starship and AI infrastructure are all scale successful. It is the higher-conviction, higher-risk story. Investors are paying for dominance in satellite internet, launch capability, defense relevance and a future that could extend far beyond today’s business lines.

Amazon is less dramatic, but more balanced. It already has the customers, cloud infrastructure, enterprise relationships, advertising reach and cash flow to keep investing through cycles. Its AI push may be expensive, but it is not starting from zero. AWS gives Amazon a clear seat at the AI infrastructure table.

Which stock looks better?

My view if investors are focused on stability, Amazon has the stronger case. It has diversified earnings, a proven cloud business, and enough cash-flow strength to fund AI and satellite infrastructure without relying on one growth engine.

However the investors focused on upside, SpaceX is the more powerful story. Starlink’s scale, launch dominance and first-mover satellite advantage give it a growth profile that Amazon cannot easily match. But that upside comes with more execution risk and heavier dependence on Starlink’s continued profitability.

Amazon looks like a safer long-term infrastructure stock, while SpaceX looks like the higher-upside but higher-risk bet. Amazon has the better financial base today. SpaceX has a more ambitious future. The better stock depends on whether investors want durability or maximum growth potential.