ECB faces a difficult inflation trade-off as energy relief weakens the case for urgency

The European Central Bank is no longer dealing with the worst version of the energy shock, but it is not dealing with a clean inflation story either. Chief Economist Philip Lane said the recent fall in energy prices has moved actual oil data away from the ECB’s stricter “adverse” baseline. That gives policymakers less pressure to rush into another hike immediately.

Energy prices have fallen away from the ECB’s adverse scenario.

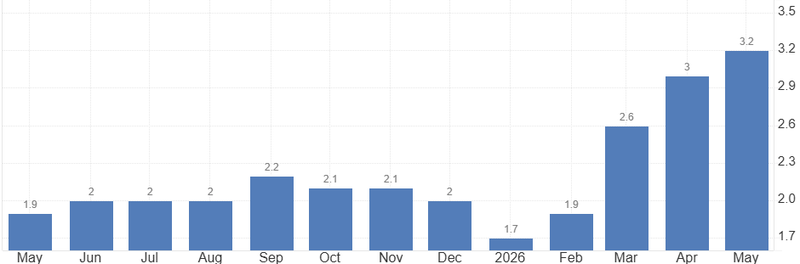

Inflation could remain above 2% in the first half of 2027.

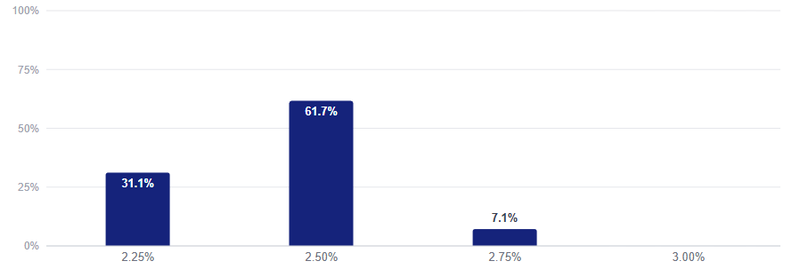

Markets expect the ECB to hold in July but see a 61% chance of a September hike.

Energy relief helps, but it does not end the inflation problem

The fallback in energy prices matters because energy was the main reason the ECB became more nervous in the first place. Higher oil and gas prices threatened to push headline inflation higher, feed into transport and production costs, and eventually reach food, goods and services.

Now that oil has eased, the most aggressive version of that risk looks less likely. Lane’s point is important: the data has moved away from the stricter adverse scenario. That gives the ECB more room to wait in July instead of rushing into another increase.

But this is not a dovish victory

The ECB still expects inflation to average around 3.0% in 2026, while real GDP expands by only 0.8%. That is the uncomfortable part. Inflation is too high, but growth is too weak. This is not the kind of economy where the central bank can tighten without consequences.

Source: Eurostat

Lagarde is defending credibility, not just fighting oil

Christine Lagarde described the recent hike as a necessary decision. That wording matters because the ECB is trying to show that it will not ignore inflation just because growth is soft.

The central bank was criticized in the past for reacting too slowly to inflation. Now it is trying to avoid the opposite mistake: waiting until price pressures become more embedded. That is why the ECB continues to repeat that policy will remain data-dependent and decided meeting by meeting.

But “data-dependent” cuts both ways

If inflation stays sticky, the ECB can justify another hike. If energy prices keep falling and growth weakens further, a second hike becomes harder to defend. The market understands this tension. That is why July is expected to be held, while September still carries a meaningful hike probability.

A September hike is alive because the inflation story is not clean

Markets are pricing the July meeting as a pause, but the September meeting is different. A 61% probability of a hike shows that investors still believe the ECB may need to act again if inflation fails to cool.

The reason is simple: the inflation problem has moved beyond energy alone.

Even if oil prices ease, the earlier shock can still pass through the economy with a delay. Firms may raise prices to protect margins. Workers may push for higher wages to recover lost purchasing power. Services inflation may stay firm even after energy prices fall.

This is the ECB’s real fear. Not one oil spike. A slower, wider inflation process that survives after the original energy shock fades. That is why Lane’s energy relief does not close the debate. It only buys time.

Source: ECB watch

Weak growth makes the decision harder

The growth backdrop is what makes this cycle so difficult.

A scenario of 3.0% inflation and 0.8% real GDP growth is not a comfortable mix. It means the ECB is fighting inflation in an economy that is already struggling to build momentum. That is why many Members of the European Parliament reacted with skepticism and concern after the 25-basis-point hike.

Their concern is not difficult to understand

Higher rates may help contain inflation expectations, but they also raise borrowing costs for households, businesses and governments. In a weak economy, that can weigh on investment, consumption and confidence. If the ECB tightens too much, it risks deepening stagnation. If it does too little, it risks allowing inflation to stay above target for too long.

That is the trap. The ECB is not choosing between a good option and a bad one. It is choosing which risk it is more willing to carry.