Microsoft AI spending remains heavy, but productivity signals are improving

Microsoft’s AI strategy is beginning to show more tangible progress, even if investors have not fully rewarded the stock for it yet. The market has spent much of the past year questioning whether the company’s aggressive AI investment cycle can generate enough returns to justify the scale of spending. That concern has not disappeared. But the latest operational signals suggest the debate may be starting to shift.

Microsoft reduced the time needed to bring new GPU capacity online by nearly 20%.

Inference throughput improved by roughly 40% across Microsoft’s most heavily used Copilot models.

Q4 capital expenditure is expected to exceed $40 billion as the company continues expanding data center capacity.

Microsoft’s AI strategy is starting to show real progress

Microsoft has been one of the clearest winners of the AI infrastructure cycle, but that position has come with a cost. Investors have grown more sensitive to the size of AI-related capital expenditures, especially as the company continues to build new data centers, secure GPU supplies, and expand cloud capacity.

That is why the recent efficiency signals matter

Microsoft reduced the time needed to bring new GPU capacity online by almost 20%. That is not just an operational improvement. It means the company can potentially turn capital spending into usable AI infrastructure faster than before. In a market where demand for compute remains high, faster deployment can become a competitive advantage.

The same applies to data center execution. Delivering one of its newest data centers six weeks ahead of schedule suggests that Microsoft is improving the pace of its AI buildout. For investors, this matters because delays in infrastructure delivery can weaken the connection between spending and revenue. Faster delivery helps close that gap.

The 40% improvement in inference throughput across heavily used Copilot models is also important. It points to better efficiency in the way Microsoft runs AI workloads. If the company can serve more AI usage with the same or better infrastructure base, the economics of its AI products could improve over time.

The capex debate is changing

The market’s concern around Microsoft is not that the company lacks demand, cash flow, or strategic position. The concern is that AI spending has become so large that investors need clearer evidence of return.

That is where the capex debate becomes more interesting

Microsoft expects Q4 capital expenditure to exceed $40 billion. This is a large number, and it keeps pressure on free cash flow expectations. It also raises the bar for management. When spending rises this quickly, investors do not only want to hear that AI demand is strong. They want to see that the infrastructure being built is used efficiently and converted into revenue.

This is why the latest operational improvements are useful for the bull case. Faster GPU deployment, earlier data center delivery, and stronger inference throughput all support the idea that Microsoft’s AI investment is not simply getting bigger. It may also be getting better.

A company can spend heavily and still destroy value if the investment does not generate enough return. But a company that spends heavily while improving utilization, deployment speed, and model efficiency can change how the market views that spending. The same capex number can look very different if investors believe it is building a stronger long-term platform rather than only pressuring margins.

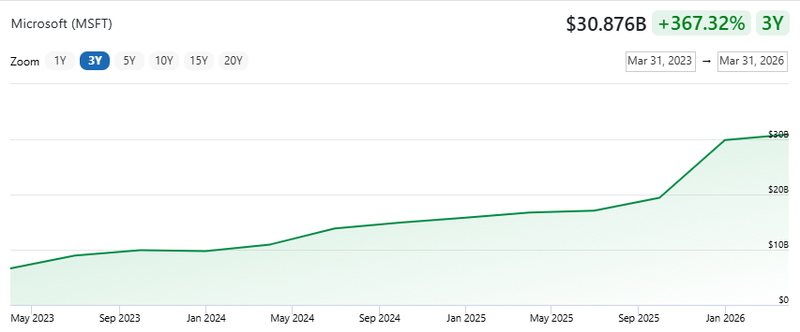

Source: Finance chart

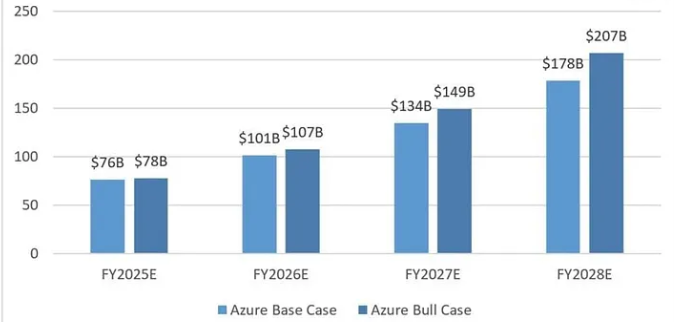

Azure remains the key proof point

Azure is still the center of the story. Microsoft’s Azure annual revenue baseline stands near $75 billion, giving the company a large foundation from which AI demand can scale.

That makes Azure performance one of the most important signals for the stock. If Azure once again outperforms expectations, it will strengthen the argument that Microsoft’s AI infrastructure buildout is translating into real cloud growth. But revenue growth alone may not be enough. Investors will also listen closely to comments on utilization rates, capacity availability, and how quickly new infrastructure is being deployed.

Azure’s growth outlook also shows why the AI debate cannot be reduced to capex alone. If AI continues to add around 10 percentage points to Azure growth over the next two years.

Even if non-AI cloud demand slows, Azure could remain on a path toward roughly $206.7 billion in revenue by FY2028. That would support the idea that AI is not only increasing Microsoft’s spending needs but also helping protect and extend the growth profile of its cloud business.

Source: Medium