Microsoft’s AI selloff: dip, reset or warning Signal?

Microsoft’s sharp decline has turned one of the market’s most reliable technology leaders into a major debate over artificial intelligence spending, free cash flow and valuation. After a reported 30% to 35% drop, a 52-week low and a $613 billion rout, investors are asking whether the selloff is a healthy reset in AI expectations or a warning signal for the broader US tech trade.

Microsoft has reportedly fallen around 30% to 35% from its peak.

The stock recently dropped to a 52-week low near $353.

AI-related capital expenditure is expected to reach about $190 billion this fiscal year.

Microsoft’s latest revenue rose 18%, while operating income increased 20% to $38.4 billion.

Microsoft becomes the market’s AI-capex test case

Microsoft has become one of the clearest tests of the artificial-intelligence trade.

The stock has gone through a sharp repricing after months of investor concern over the cost of AI infrastructure. Recent market coverage points to a decline of roughly 30% to 35%, a fall to a 52-week low, and a reported $613 billion loss in market value during the selloff. At one point, Microsoft was on track for its worst monthly performance since 2000.

That kind of move matters beyond one company. Microsoft is a major weight in the Nasdaq 100 and S&P 500, a key driver of US technology sentiment, and one of the most important proxies for the AI investment cycle.

The central question is simple: is Microsoft being punished for spending too much on AI, or is the market underestimating how much future earnings power that spending can create?

The selloff is about AI spending, not business weakness

Microsoft’s decline has not been driven by collapsing fundamentals.

The company’s latest quarterly numbers remained strong. Revenue rose 18% year over year, or 15% in constant currency. Intelligent Cloud, where Azure is reported, grew 30%. Productivity and business software revenue increased 17%. Operating income rose 20% to $38.4 billion.

Those figures do not look like a company losing relevance.

The pressure is coming from the other side of the equation: spending. Microsoft expects capital expenditure of about $190 billion in the current fiscal year, largely tied to artificial-intelligence infrastructure. That is more than 60% above last year’s level and far above earlier expectations.

Investors are therefore not questioning whether Microsoft is still a high-quality business. They are questioning whether the company can turn massive AI spending into enough revenue, margin and free cash flow to justify the investment.

AI capex is compressing the valuation debate

Microsoft’s AI strategy is expensive because it touches almost every part of the business.

The company is integrating Copilot into its productivity software, expanding Azure’s AI capabilities, building infrastructure for enterprise customers and deepening its exposure to OpenAI-related demand. More than one-third of Microsoft’s revenue is now viewed as directly or indirectly linked to AI.

That gives the company major upside if AI adoption continues. It also makes Microsoft vulnerable if investors begin to believe AI monetisation is moving too slowly.

This is why the stock has become a “buy the dip or value trap?” debate. Bulls see a company investing heavily ahead of a long growth cycle. Skeptics see rising capital intensity, pressure on free cash flow and uncertainty over when AI revenue will fully catch up with infrastructure costs.

The bullish case: growth is still strong

The bullish argument starts with Microsoft’s execution.

Azure demand remains strong, and management has indicated that customer demand continues to exceed available supply. That is important because it suggests the company is not building AI infrastructure without demand. The constraint is capacity, not lack of customers.

Microsoft’s AI business has also shown rapid growth. Annual recurring revenue tied to AI reportedly grew 123% to $37 billion in the latest quarter, while the cloud computing division grew at a 40% pace. Paid Copilot adoption is also improving, with more than 20 million users compared with about 15 million paid seats one quarter earlier.

These numbers support the view that AI is already becoming a commercial business, not only a long-term promise.

There is also a broader industry signal. For the second consecutive quarter, and reportedly for the first time, AI revenue exceeded the depreciation cost of the equipment supporting it. That does not settle the profitability debate, but it suggests the AI infrastructure cycle is beginning to show more financial traction.

The bearish case: valuation and cash flow still matter

The bearish case is not that Microsoft is a weak company.

The concern is that even great companies can become expensive when expectations are too high. AI infrastructure requires huge upfront spending, and investors are watching whether that spending reduces free cash flow flexibility.

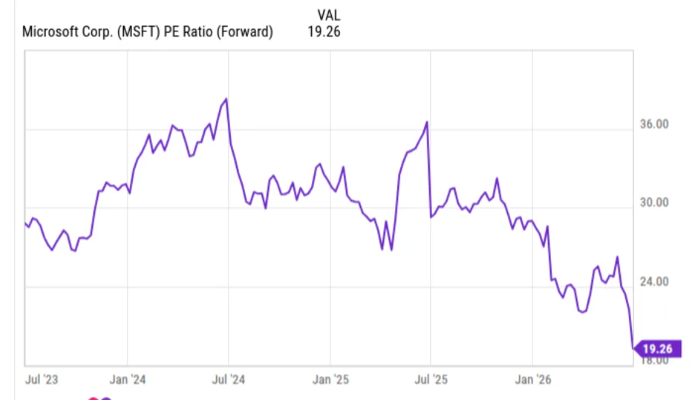

Some retail investor debates have focused on free cash flow multiples, including concerns around whether a roughly 39-times FCF valuation still leaves too much optimism priced in. Others argue that Microsoft may look cheaper on forward earnings, with one valuation snapshot showing the stock around 19.3 times forward earnings versus roughly 21.5 times for the S&P 500.

Source: Ycharts

That split explains the debate. On earnings, Microsoft may look unusually attractive compared with the broader market. On free cash flow, the AI capex cycle makes the picture more complicated.

For traders, the risk is that Microsoft can remain a high-quality company while the stock still struggles if markets demand clearer evidence of AI returns.

Why Microsoft matters for Nasdaq 100 traders

Microsoft’s selloff is not just a single-stock story.

Because of its size, Microsoft can influence the direction of the Nasdaq 100, S&P 500 and broader US technology sentiment. When MSFT weakens, it can pressure index momentum, especially if investors start reducing exposure to other AI-linked mega-cap names.

The stock has also become a proxy for the market’s willingness to finance heavy AI investment. If investors reward Microsoft’s spending, that supports the broader AI trade. If they continue to punish the stock, it could signal a tougher environment for other companies with large data-center, cloud and AI infrastructure budgets.

For CFD traders, this matters because Microsoft can affect both single-stock price action and index-level volatility. However, leverage can amplify losses as well as gains, so risk management is essential when trading around high-volatility technology moves, earnings releases or major guidance updates.

Key levels and watchpoints

Recent price action gives traders several important reference points.

The stock fell from around the low-to-mid $500s during its stronger period to the $370s during the latest repricing, with one recent low near $353. It has since rebounded toward the $390 area, but the broader trend remains fragile until investors gain more confidence in the AI spending outlook.

The first major watchpoint is earnings. Markets will focus on Azure growth, Copilot adoption, AI annual recurring revenue, margins, and whether management changes its capex guidance.

The second is free cash flow. If Microsoft can show that AI revenue is scaling faster than infrastructure costs, the stock may regain support. If capex keeps rising faster than cash generation, the valuation debate could remain difficult.

The third is broader AI sentiment. Nvidia, Amazon, Alphabet, Meta and OpenAI-related news can all influence how investors price Microsoft’s AI exposure.

OpenAI exposure adds another layer

Microsoft’s OpenAI relationship remains an important part of the investment case.

Investors continue to watch whether OpenAI’s growth, product expansion or potential IPO narrative could indirectly support Microsoft’s valuation. Microsoft benefits from enterprise AI demand, Azure infrastructure usage and its integration of AI tools across software products.

But this relationship also adds complexity. The market will want to see whether AI partnerships translate into durable, high-margin revenue rather than only higher spending.

That is why Microsoft’s next few quarters are so important. The company needs to prove that AI is not only a strategic advantage, but also a financial engine.