PCE inflation could decide whether the Fed hikes by autumn

The next PCE inflation reading has become more than another data point. It may decide whether markets keep treating the Federal Reserve’s hawkish shift as a warning or start pricing it as a real policy path. The problem is that inflation is no longer moving in a clean direction. If PCE pushes toward 3.4%, and especially if later readings point toward the 4.0% to 4.1% range, the market will have a harder time believing the Fed can stay on hold for long.

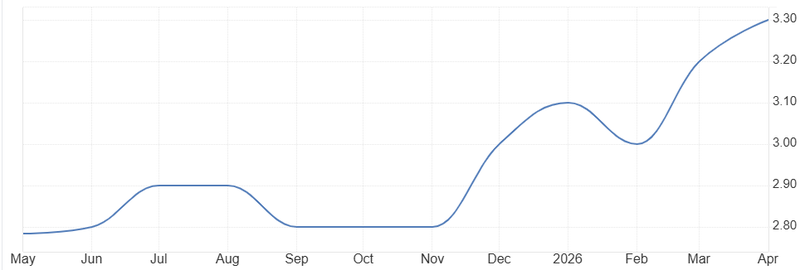

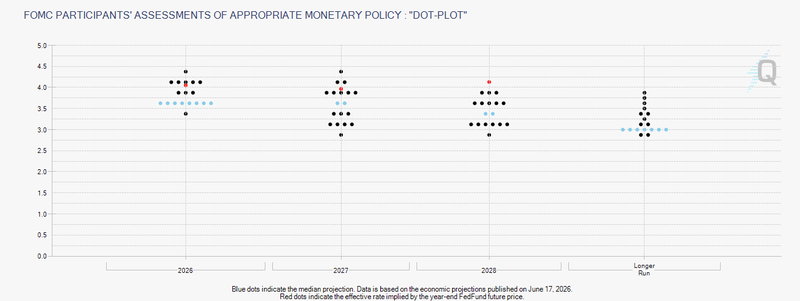

The Fed dot plot now points to a 3.8% year-end rate.

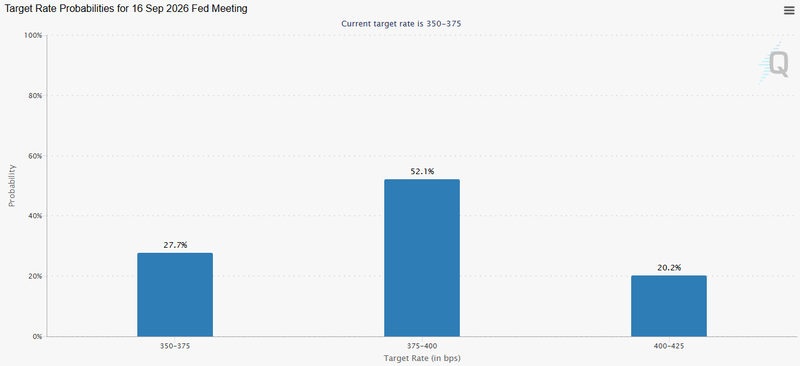

Markets are pricing a 68% chance of a September rate hike.

Nine of eighteen officials expect at least one hike before December.

PCE is now the Fed’s real test

PCE inflation matters because it has long been the Fed’s preferred inflation measure. Under Jerome Powell, it was the inflation report markets watched most closely because it shaped how the Fed judged underlying price pressure. CPI often created the first market reaction, but PCE carried more weight inside the policy debate because it gave officials a broader view of consumer prices and spending behaviour.

The question now is whether PCE keeps the same importance under Kevin Warsh.

Warsh is expected to change parts of the Fed’s communication regime, especially by relying less on heavy forward guidance and more on incoming data. But that does not make PCE less important. It may make it even more important.

If the Fed gives fewer hints about future decisions, markets will lean harder on the data that the Fed itself watches most closely. And PCE is still the cleanest test of whether inflation is moving back toward target or beginning to accelerate again.

The issue is not only whether one inflation reading comes in high.

The real issue is whether inflation starts to look persistent again. If PCE moves toward 3.4%, markets may see that as uncomfortable but still manageable. If later readings point toward 4.0% or 4.1%, the Fed’s patience becomes much harder to defend.

Source: U.S. Bureau of Economic

Why Warsh’s message made markets nervous

Warsh’s first policy message made this cycle more difficult because he did not give markets the comfort of clear guidance.

He did not strongly signal the next move. He did not push investors toward a specific meeting. He left the decision open and tied it to upcoming economic reports.

That sounds responsible, but it also creates a pricing problem.

When the Fed refuses to guide the market, traders have to price the risk themselves. And when inflation is above target, that risk usually leans toward higher rates. This is why September pricing has become so important. A 68% probability of a hike does not mean a move is guaranteed, but it shows that markets now see the autumn meeting as live.

Source: CME Group

The dot plot changed the debate

The updated Fed dot plot made the hawkish shift more visible.

The new projections removed expectations for 2026 rate cuts and pushed the median year-end rate projection to 3.8%. More importantly, nine of eighteen officials now expect at least one quarter-point hike before December.

That matters because the debate inside the Fed has clearly changed.

Earlier, markets were focused on when policy might ease. Now, the question is whether policy is tight enough. If half the committee already sees a hike as likely, then the next inflation surprise does not need to change the whole Fed. It only needs to strengthen the hawkish side that already exists.

Source: CME Group

That is why PCE carries so much weight

It will either calm the market or give the hawks more evidence. Why higher inflation would force a harder Fed choice

The Fed can live with slow progress. It cannot easily ignore renewed acceleration.

If inflation is sticky but gradually moving lower, Warsh can argue that current policy is restrictive enough and that the Fed should wait. But if inflation moves higher again, especially toward the 4% area, that argument becomes weaker.

Staying on hold starts to look risky

The Fed would not only be fighting inflation. It would also be defending its credibility. After the earlier inflation shock, officials are sensitive to the idea that they waited too long. A stronger PCE reading would bring that fear back.

It is not only about the number itself. It is about what the number says about the Fed’s reaction function.

For now, markets are pricing one rate hike this year. That still leaves room for patience. But the balance is fragile. If PCE inflation rises toward 3.4% and later points toward 4.0%–4.1%, the September hike probability could rise further, and the market may start pricing a more aggressive path.

A softer PCE reading would give Warsh room to stay patient. Stronger reading would make patience look harder to justify.