S&P 500 calm looks fragile as dollar funding stress builds underneath

S&P 500 remains near 7,483, equities are not yet showing panic, and the surface of the market still looks orderly. But the stress is not starting in equities. It is showing up in the dollar, in FX volatility, and in the cost of offshore funding. That matters because major equity breaks often begin away from the equity screen.

The S&P 500 remains steady, nearly 7,483 despite growing FX stress.

A stronger dollar tightens global financial conditions and raises funding pressure.

The US Dollar Index is trading at a 52-week high.

Stronger dollar turns S&P 500 calm into a liquidity risk

The index remains near 7,483, major equity volatility has not yet broken out, and investors are still leaning on familiar support from mega-cap leadership, AI momentum and passive flows. But the first signs of stress are not always visible in equities. They often appear first in the currency market, where dollar funding, hedging costs and cross-border leverage are priced in real time.

That is why the dollar matters so much now

The US Dollar Index is trading at a 52-week high. For US investors, that may look like a sign of relative strength. For the global system, it is also a tightening force. A stronger dollar makes dollar liabilities more expensive for borrowers outside the US. It weakens local-currency balance sheets, lifts hedging costs and forces foreign institutions to find more dollars to maintain the same positions.

This is where equity risk begins to build

Global banks and investors often fund in dollars and deploy capital into local markets or cross-border portfolios. That structure works when dollar liquidity is easy and currencies are stable. But when the dollar rises quickly, leverage ratios deteriorate. Margin pressure increases. Funding costs rise. The first response is not always to sell the worst asset. It is often to sell the most liquid asset.

That is why the S&P 500 can become part of the funding story

US equities are deep, liquid and widely held. In a dollar squeeze, they can become a source of cash even if investors still like the long-term earnings story. This is not about suddenly turning bearish on America’s largest companies. It is about balance-sheet mechanics. When dollars are needed, liquid winners are often sold first.

History gives this argument more weight

In 2007, the EUR/USD cross-currency basis began to blow out in August, showing that foreign institutions were paying a higher premium to access dollars. The S&P 500 did not reach its major peak until October. The funding market was already warning that institutional dollar liquidity was tightening, even while equities still looked resilient.

The same pattern appeared in 2020, only faster. Offshore dollar pressure and commercial-paper stress began building in early February. The S&P 500 did not top until February 19. Once the liquidity shock became visible, the equity move was violent.

Source: LeadLag

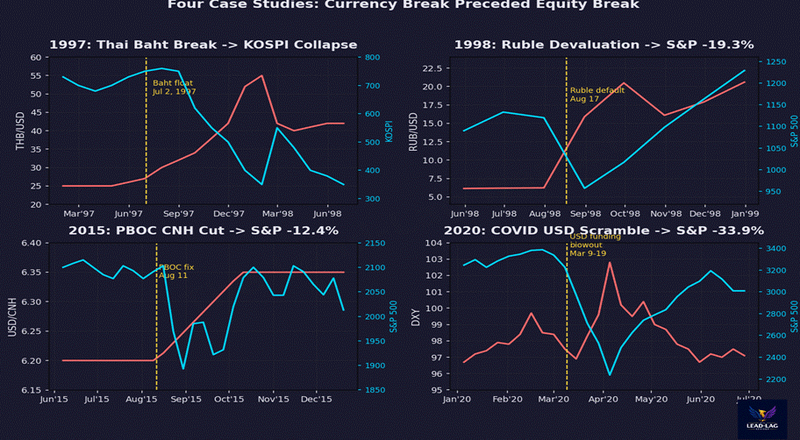

Currency markets are flashing before stocks

Before major stock-market drawdowns, stress often appears first in currencies. That is not because FX traders know the future. It is because currency markets sit closer to funding pressure, dollar shortages, capital flight and reserve management. When global investors start reducing risk, the first signs often show up in exchange rates and funding spreads before they appear in equity indices.

History shows this pattern clearly. Before the 2008 equity peak, the EUR/USD cross-currency basis had already moved sharply, signaling rising stress in dollar funding. In 2020, currency funding pressure also appeared before equities fully priced the shock. In 1997, the Thai baht’s collapse warned that pressure was spreading through Asia well before the S&P 500 felt the full impact later that year.

Source: LeadLag

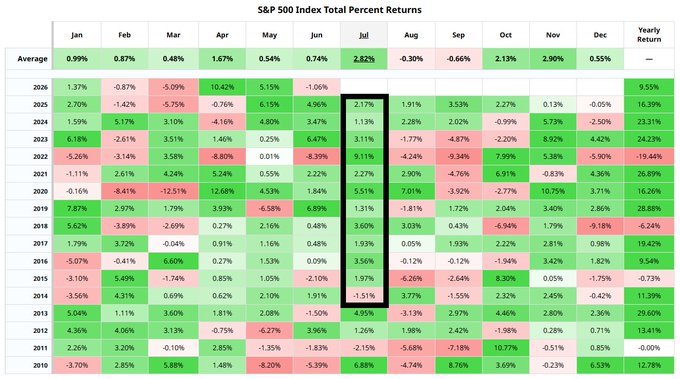

July seasonality supports the S&P 500

Seasonality helps explain why equity investors may still feel comfortable, but it does not cancel the FX warning. Since 2015, July has usually been a strong month for the S&P 500, with the index finishing higher each time. The dollar has been less predictable, with DXY posting six positive Julys and five negative ones over the same period.

That difference matters. Stocks may enter July with a favourable seasonal backdrop, but the dollar can still change the tone quickly. If profit-taking continued and fed supports the DXY strengthens, the market may face a tighter liquidity backdrop than the S&P 500’s July record suggests.

Source: Bar chart

None of this guarantees an equity sell-off tomorrow

FX stress does not guarantee an immediate equity sell-off. But it does challenge the idea that a calm S&P 500 means the system is calm. Currency markets are closer to the plumbing. They reflect the need for dollars before equity investors are forced to price the consequences.

There is one global financial cycle, not many separate ones. It moves with dollar liquidity, volatility and risk appetite. Countries can have different exchange-rate regimes and different domestic stories, but when dollar liquidity tightens, the pressure travels through the same channels: funding costs, hedging markets, reserve flows, credit conditions and eventually risk assets.

For the S&P 500, the risk is not only that a stronger dollar hurts foreign earnings translation. That is the surface-level concern. The deeper issue is that a stronger dollar can force global balance sheets to reduce risk. If investors need dollars, they may sell what can be sold quickly. The S&P 500 sits at the center of that liquidity pool.