BoE holds rates steady as unemployment improves; Canadian PPI hits multi-year high

The Bank of England held interest rates at 3.75% amid steady 2.8% inflation and falling unemployment. Concurrently, Canada's annual PPI reached a multi-year high of 13.6% due to Middle East supply issues. Meanwhile, US stock markets rebounded as dropping oil prices fuelled optimism for the reopening of the Strait of Hormuz.

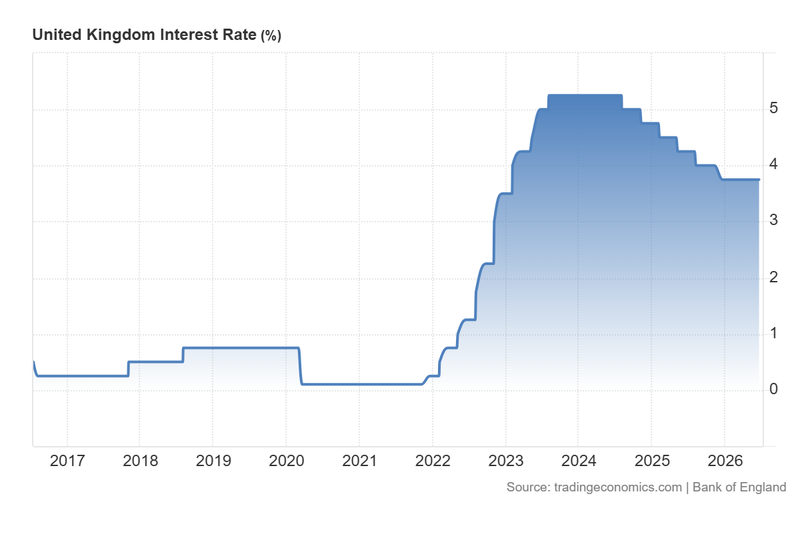

The Bank of England unanimously voted 7-2 to keep interest rates steady at 3.75%, remaining vigilant against elevated domestic inflation pressures.

UK unemployment fell to 4.9% while annual inflation held at 2.8% in May, easing immediate pressure on the central bank for ahead policy adjustments.

Canada's annual Producer Price Index surged to 13.6%, a multi-year peak driven by soaring costs in chemicals, energy, and petroleum products.

US indexes rallied, with the S&P 500 hitting 7,500, as a drop in oil benchmarks sparked optimism over the reopening of the Strait of Hormuz.

BoE maintains rates as unemployment declines and inflation remains steady

The Bank of England (BoE) opted to leave the Bank Rate unchanged at 3.75%, matching market consensus. The Monetary Policy Committee (MPC) decision revealed a 7–2 split, with the majority voting to maintain the status quo against a minority of two members who advocated for a 25-basis-point increase. While the UK central bank anticipates economic relief should Middle East tensions subside—particularly given ongoing negotiations between the US and Iran—it continues to view current inflation levels as uncomfortably elevated. Consequently, policymakers said that they remain firmly committed to dampening persistent price pressures.

Furthermore, data released yesterday by the Office for National Statistics (ONS) showed that the headline consumer price index (CPI) inflation rate remained unchanged in May at 2.8%. Simultaneously, by today the ONS reported that the unemployment rate fell from 5.0% in March to 4.9% in April. Taken together, these economic indicators reduce the immediate pressure on the BoE to alter its current monetary policy trajectory. Nevertheless, market analysts still anticipate a rate hike later in 2026, though the central bank is highly likely to await further macroeconomic data and a formal resolution of the geopolitical conflict in the Middle East.

In foreign exchange markets, the British pound depreciated sharply against the US dollar, shedding 0.64% to trade at $1.3207. This marks the second consecutive session of declines for the GBP/USD pair, influenced by a reduction in domestic policy pressure on the BoE, and a more restrictive tone adopted by the Federal Reserve. Meanwhile, the UK’s benchmark FTSE 100 index fell by 1.04% to close at 10,399 points.

Figure 1. United Kingdom Interest Rate (2016–2026). Source: Data from the Bank of England; Figure obtained from Trading Economics.

Canadian PPI reaches a level not seen since June 2022

According to data compiled by Statistics Canada, the Producer Price Index accelerated sharply from 11.1% in the previous month to 13.6% in annual terms for April, representing its highest level since June 2022. Conversely, the month-on-month PPI advanced by 1.2%, crossing the wires below the analyst forecast of +1.8% and trailing the previous monthly reading of 1.6%.

An analysis provided by Trading Economics indicates that the most significant upward pressure originated from raw materials, led by chemical products (+7.0%), energy and petroleum products (+2.5%), and primary non-ferrous metal products (+1.1%). These broad-based increases are directly linked to ongoing energy supply chain disruptions in the Middle East, which have driven up commodity prices across multiple industrial sectors.

Following the statistical releases from Ottawa, the USD/CAD currency pair advanced 0.25% to 1.4128. This move reflected a strengthening US Dollar Index (DXY) compounded by short-term weakness in the Canadian dollar.

US stock market rebounds amid hopes of a Strait of Hormuz reopening

US equity markets staged a synchronized recovery by the closing bell, buoyed by growing expectations that the Middle East conflict might reach a diplomatic resolution, potentially leading to the reopening of the Strait of Hormuz. This optimism was strongly reinforced by a sharp correction in the energy markets, where both the Brent and West Texas Intermediate (WTI) crude benchmarks accumulated a 12% decline over the preceding five sessions.

Market participants are now keenly focused on Friday, when the Strait of Hormuz is officially anticipated to resume maritime operations. Investors calculate that a normalization of the energy supply chain would fundamentally ease global inflationary pressures, thereby lowering the probability that the Federal Reserve will feel compelled to implement more restrictive monetary tightening measures in its upcoming policy decisions.

At the market close, the S&P 500 index gained 1.08% to finish at 7,500 points, the Dow Jones Industrial Average crept up by 0.14% to 51,570, and the tech-heavy Nasdaq 100 appreciated by 2.48% to settle at 30,406 points.