US nonfarm payrolls slow, while unemployment falls

US payroll growth slowed sharply in June, signalling weaker hiring despite a lower unemployment rate. Markets pared near-term Fed hike expectations, weighing on the dollar while yields stayed firm. US equities diverged as tech sold off, while Eurozone unemployment remained steady and the euro strengthened.

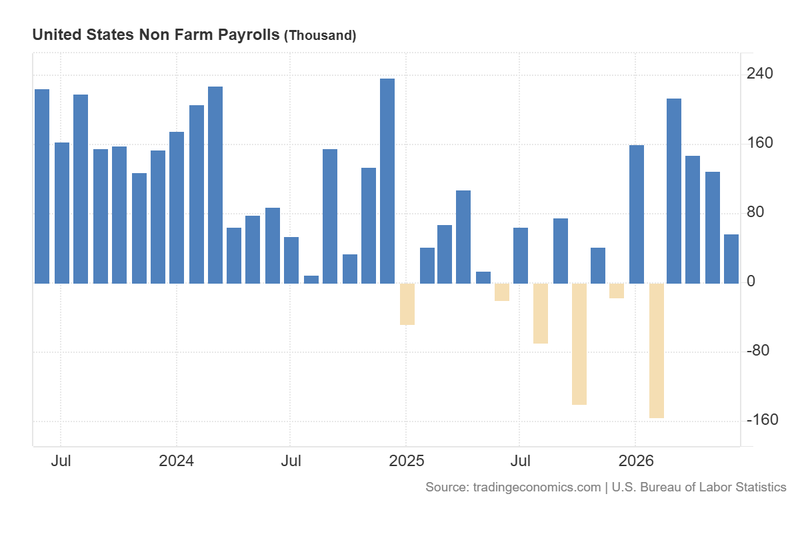

US nonfarm payrolls slowed to 57K in June, well below 110K forecasts and the weakest gain since February 2026. In turn, unemployment rate fell to 4.2%, the lowest since June 2025.

Fed hike expectations shifted from September to October, pushing DXY down 0.56% while yields held near 4.48%.

Eurozone unemployment stayed at 6.2%, below forecasts, supporting the euro’s 0.49% rise to $1.1432.

US payroll growth slows sharply despite lower unemployment

According to data released by the US Bureau of Labor Statistics (BLS), non-farm payrolls slowed from a revised 129,000 in May to 57,000 in June, significantly below market expectations of approximately 110,000. The June reading represents the weakest pace of job creation since February 2026 and suggests a moderation in labour-market momentum. The slowdown may reflect the impact of heightened uncertainty surrounding the Middle East conflict, together with concerns that persistently restrictive monetary conditions could weigh on business confidence and hiring decisions.

The BLS report showed that the strongest employment gains were recorded in professional and business services (+36,000), social assistance (+25,000) and health care (+22,000). By contrast, leisure and hospitality lost 61,000 jobs, marking the largest decline among the major sectors.

At the same time, the unemployment rate declined from 4.3% in May to 4.2% in June, below market expectations for an unchanged reading. This was the lowest rate since June 2025. However, the apparent improvement should be interpreted with caution, as it could be partly driven by a decline in labour-force participation rather than stronger employment growth. Consequently, the June employment report delivered mixed signals, with hiring activity weakening while the headline unemployment rate moved lower.

Following the release, US equity markets closed with mixed performances. The Nasdaq 100 fell 1.61% to 29,329 points, while the S&P 500 remained broadly unchanged near 7,483 points. In contrast, the Dow Jones Industrial Average advanced 1.14% to 52,905 points, reaching a fresh record high. This divergence may reflect investor rotation away from high-growth technology stocks amid growing concerns about valuations in artificial intelligence-related companies, while more defensive and cyclical sectors attracted inflows.

Meanwhile, the CME FedWatch Tool showed a notable adjustment in interest-rate expectations. Market-implied probabilities suggested that a rate increase at the September Federal Reserve meeting was no longer the most likely outcome, as investors reassessed the strength of the labour market following the weaker-than-expected payroll figures. Expectations subsequently shifted towards a potential 25-basis-point rate increase in October, indicating that market participants attributed greater significance to the slowdown in job creation than to the decline in the unemployment rate.

As a result, the US Dollar Index (DXY) fell 0.56% to 100.85, reflecting reduced expectations for near-term monetary tightening. In contrast, US Treasury yields edged higher to around 4.48%, suggesting that inflation concerns and longer-term policy expectations continued to provide support for bond yields.

Figure 1. US Non Farm Payrolls (2023-2026). Source: Data from the US Bureau of Labour Statistics. Figure obtained from Trading Economics.

Eurozone unemployment rate remains stable below expectations

According to Eurostat, the euro area's unemployment rate remained unchanged at 6.2% in May, outperforming market expectations of 6.3%. The current reading remains close to the lowest levels observed over the past decade, highlighting the resilience of the Eurozone labour market and suggesting limited labour-market pressure on the European Central Bank (ECB), whose primary focus remains the containment of inflation.

Data compiled by Trading Economics indicate that Germany (3.8%) and the Netherlands (3.9%) recorded the lowest harmonised unemployment rates within the Eurozone. By contrast, Spain (10.3%), France (8.2%) and Italy (5.0%) continued to exhibit comparatively higher levels of unemployment.

Despite persistent economic headwinds and weak growth dynamics across parts of the region, labour-market conditions remain relatively robust, providing an important source of support for household consumption and broader economic activity. At market close, the euro appreciated by 0.49% versus the US dollar at $1.1432.