Alphabet’s AI spending tests how much cash flow investors are willing to trust

Alphabet is becoming one of the clearest tests of the AI investment cycle. The company is raising $84.75 billion in equity capital to fund a much larger buildout in AI and compute infrastructure, while full-year capital expenditure guidance has moved to $180–$190 billion.

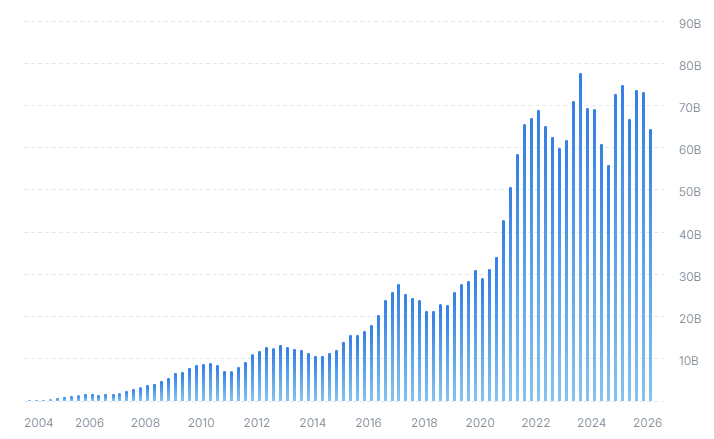

Last twelve months’ free cash flow at around $95.40 billion.

Projected 2030 free cash flow reaching about $187.49 billion.

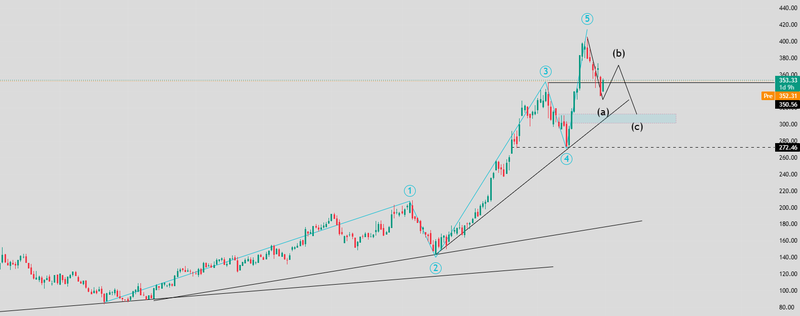

Wave C could pull the price toward 271–280

Cash flow is the reason the market still listens

Last twelve months’ free cash flow at around $95.40 billion. This gives Alphabet an advantage that many AI infrastructure firms lack: the ability to fund much of the AI race from operating strength, rather than relying solely on debt, dilution, or investor optimism.

But the equity raise shifts the discussion When a company like Alphabet raises this much capital, investors will not view it as a liquidity issue. They will interpret it as a sign that the AI expansion is growing bigger, faster, and more costly than initial models predicted. This is important because the market is no longer rewarding AI spending automatically. It wants to see if each additional dollar of CapEx can produce lasting revenue, stronger cloud margins, better model profit, and a greater competitive edge.

Alphabet joins the Dow as AI reshapes the index

Alphabet’s addition to the Dow Jones Industrial Average is more than a routine index reshuffle. By replacing Verizon Communications, the Dow is giving greater weight to businesses driving artificial intelligence, cloud computing and digital advertising. The change also means Alphabet will become part of more index-tracking portfolios, creating another source of long-term demand for the stock. It reflects how much the market has changed over the past few years, with AI and digital infrastructure now playing a much larger role in shaping the direction of major US equity indices.

This is where valuation becomes more sensitive

The current model employs a two-stage Free Cash Flow to Equity method, combining analyst forecasts with long-term projections from Simply Wall St. Those estimates remain strong. Free cash flow is expected to stay in the tens of billions in the interim years, with projected 2030 free cash flow reaching about $187.49 billion. That kind of figure explains why investors can still defend a high valuation. If Alphabet’s spending on AI infrastructure generates the expected cash-flow growth, today’s CapEx wave might appear as a necessary investment rather than excess.

The risk is timing

Alphabet is spending now based on cash flows expected in the future. If AI demand keeps rising and cloud monetization improves, the market may accept the short-term dilution and capital intensity. However, if revenue growth slows or if returns from AI infrastructure take longer to materialize, investors may begin applying a heavier discount to those future cash flows. Alphabet has the earning power to pursue AI aggressively. The question is whether the market believes the next phase of free cash flow will arrive quickly enough to justify today’s level of spending.

Source: Alpha spread

Technical outlook

Alphabet has moved into a correction after a strong rally, but the bigger chart has not broken yet. The stock recently pushed to a fresh high near 400 before profit-taking pulled it back toward the 350–353 area. Short-term momentum has clearly cooled, but the broader trend is still being protected by the rising trendline that has guided the move higher for more than a year.

The key area now is 350–353. This zone matters because it was resistance before the breakout and is now being tested as support. That is often where the market decides whether a rally still has strength or whether the breakout has failed. If buyers continue to defend this area, the decline would look more like a normal reset after an extended move rather than the beginning of a deeper reversal.

Source: Trading view

Scenarios ahead

The constructive scenario requires Alphabet to hold the 350–353 region and rebuild momentum from there. If buyers regain control, the first upside target would be the 380 area, followed by a retest of the recent high near 400. A clean break above 400 would put the stock back into new-high territory and confirm that the broader bullish trend is still in control.

The weaker scenario is a deeper corrective structure. In that case, wave A could extend toward the 300–310 demand zone, where previous buying interest appeared and where the rising trendline begins to matter again. This area would be the first real test of whether the broader uptrend still has support beneath it.

If Alphabet rebounds from that zone but fails to reclaim 350–360, the move would likely be treated as wave B rather than a full recovery. That would mean the stock is only retesting former support as resistance, not restarting the uptrend. As long as price remains below the recent swing high and cannot recover the 350–353 zone with conviction, the correction would remain active.

Wave C would then become the main downside risk. A deeper leg could pull the stock toward 271–280, which is the most important support zone below the current market. That area combines horizontal support with the longer-term rising trendline. If buyers defend it, Alphabet’s long-term bullish structure would remain alive even after a deeper correction. If it fails, the market will have to reassess the whole trend.

Source: Trading view