Eurozone inflation slows more than expected; Euro weakens

Eurozone inflation slowed more than expected in June, easing pressure on the ECB as both headline and core readings declined, although inflation remains above target. The euro weakened against the dollar as softer data contrasted with expectations of further Federal Reserve tightening.

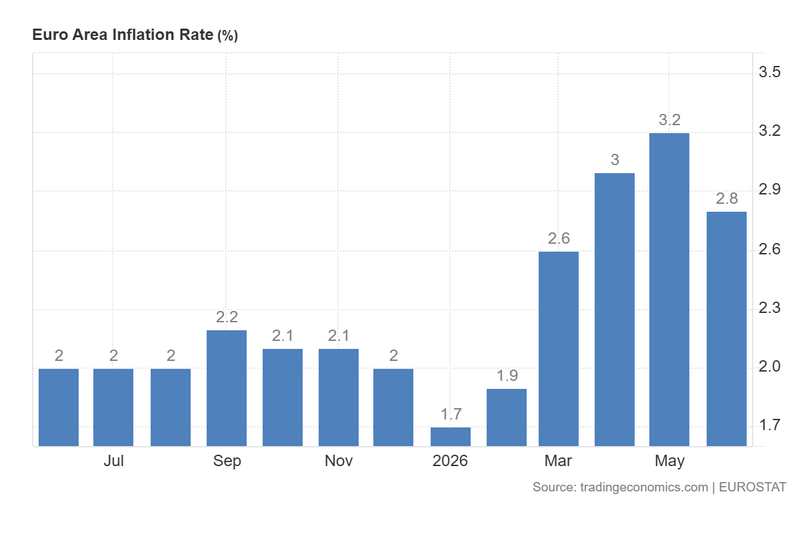

Eurozone headline inflation slowed to 2.8% in June, below the 3.0% forecast and down from 3.2% in May.

Core inflation eased to 2.4%, also below expectations, as energy, services, and food pressures moderated.

The euro fell by 0.36% to around $1.1377, as softer inflation reduced pressure for aggressive ECB tightening.

Eurozone inflation decelerates faster than forecast; euro declines

According to data released by Eurostat, euro area annual headline inflation decelerated from 3.2% in May to 2.8% in June, based on preliminary figures, coming in below analysts’ expectations of 3.0%. In turn, core inflation—which excludes the more volatile components of energy and unprocessed food—slowed from 2.6% to 2.4% over the same period, also below market expectations for an unchanged reading. Eurostat data showed that the most relevant moderation came from energy inflation, services, and food, alcohol, and tobacco, while non-energy industrial goods remained stable. At the country level, inflation decelerated notably in Germany, France, and Italy, while Spain’s rate remained unchanged.

The latest inflation figures reduce some pressure on the European Central Bank (ECB). At the same time, the labour market continues to show resilience, with the euro area unemployment rate standing at 6.3%, close to historically low levels. However, growth conditions remain fragile, as euro area GDP contracted by 0.2% in the first quarter of 2026 on a quarter-on-quarter basis, signalling that the region continues to face difficulties in terms of economic momentum. Additionally, current inflation levels remain above the ECB’s 2% target.

Following the inflation release, the euro weakened against the US dollar by 0.36%, trading near $1.1377, as markets interpreted the softer inflation data as reducing the need for more aggressive ECB tightening. By contrast, expectations that the Federal Reserve could raise interest rates later in the year have continued to support the US dollar, widening the relative monetary policy divergence between the two central banks.

Figure 1. Euro Area Inflation Rate (2025–2026). Source: Data from Eurostat; figure obtained from Trading Economics.

Technical analysis of the EUR/USD pair

From a technical standpoint, the EUR/USD pair is signalling a period of weakness. Key observations include:

- Trend context: Over the long term, the pair is currently trading below its 50-day, 100-day, and 200-day Simple Moving Averages (SMAs), reflecting a period of market uncertainty.

- Resistance levels: Should the short-term resistance at $1.1480 be breached to the upside, the next major technical ceiling is identified at $1.1650—a level where the 200-day SMA converges. A decisive breakout above this level would signal the potential for a further extension towards higher valuations.

- Support levels: If the structural pivot point at $1.1250 is compromised, the next critical floor is situated at $1.0850. A breach of the $1.0850 zone would significantly increase the probability of a deeper market correction.

- Momentum indicators: The Moving Average Convergence Divergence (MACD) is exhibiting a bullish divergence, suggesting that a potential short-term recovery could occur. In turn, the Relative Strength Index (RSI) is trading in oversold territory, reinforcing the possibility of a short-term rebound or consolidation phase.

Figure 2. EUR/USD Pair (2025–2026). Source: Data from the Intercontinental Exchange (ICE); own analysis conducted via TradingView.