Oil market turns back to inventories as war premium fades

Oil’s sell-off is not only about geopolitics anymore. The market is starting to look again at the physical balance, On one side, the fear premium is fading. Supply routes that looked vulnerable during the height of the Middle East crisis are reopening, and traders are no longer pricing the same level of immediate disruption around Hormuz. That has allowed crude prices to fall as the market removes part of the war premium built into prices.

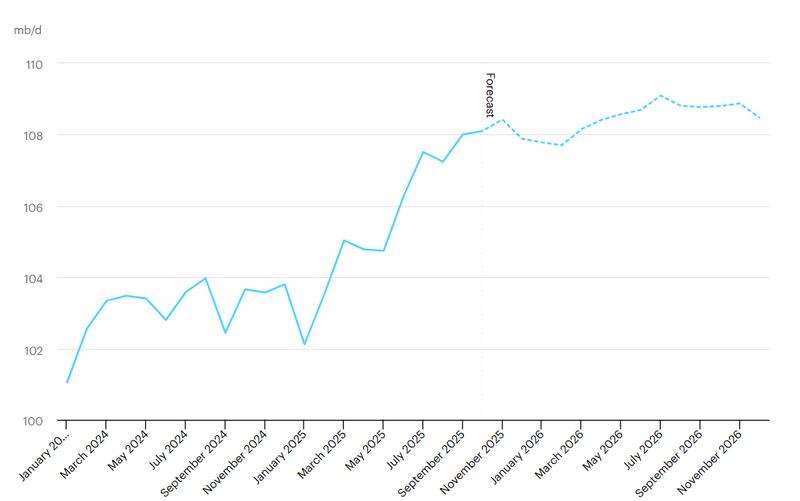

The IEA has already forecasted a large oil surplus in 2027.

The market is shifting from war-risk pricing back toward balance-sheet fundamentals.

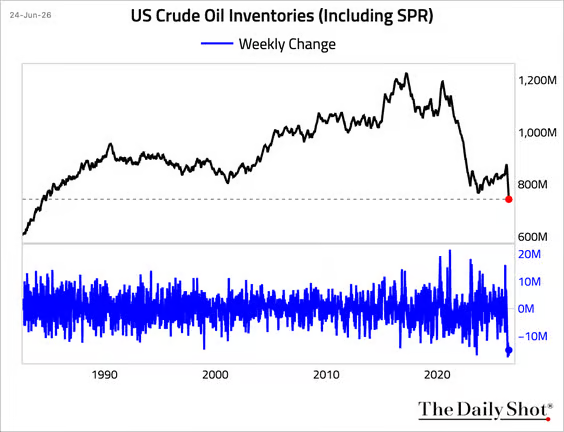

US crude inventories, including strategic reserves, are at their lowest level since 1984.

Oil is no longer trading only on war risk

Inventories remain the part of the oil story that prevents traders from becoming too relaxed. US crude inventories, including strategic reserves, are at their lowest level since 1984, while stockpiles at Cushing, the key US pricing hub, are close to operational minimum levels. That matters because inventories are not just a statistic. They are the market’s shock absorber. When storage is healthy, traders can look through temporary disruptions because the system has enough barrels to bridge the gap. When storage is thin, even a small logistical problem can move prices more sharply.

If stocks there sit too close to minimum operating levels, the market becomes more sensitive to refinery demand, pipeline flows and regional supply imbalances. This does not mean oil must rally immediately. It means the downside is not completely clean. A market with low inventories can still fall when war premium fades, but it falls with less protection underneath.

That is the uncomfortable part

The geopolitical bid is weakening, but the physical cushion is still not strong enough to make the market feel secure.In the near term, low inventories keep crude exposed to sudden rebounds if physical supply tightens again. In the medium term, the surplus forecast limits how far the market can lean into a durable rally once geopolitical risk fade. That is why the recent decline is not only a relief move. It is also the return of a colder question: if the war premium is coming out, what is left to support prices?

Source: Daily Shot

Inventories risk is back

he other side of the market is the International Energy Agency’s surplus forecast for 2027. That outlook was easy to ignore when traders were focused on Hormuz, shipping risk and the possibility of a wider regional disruption. In a crisis, the market prices the risk that barrels may not arrive next week. It does not spend much time worrying about oversupply next year. But now that supply routes are reopening and crude prices are falling, the surplus narrative is returning.

That changes the tone of the market

Falling prices are no longer only about relief from war risk. They also reflect the possibility that the market may be moving back toward a looser medium-term balance. This is what creates tension. Near-term inventories argue for caution, while the 2027 surplus forecast limits confidence in a durable rally. Oil is no longer trading one clean story. It is caught between a thin present and a potentially oversupplied future. If routes stay open and demand does not surprise strongly to the upside, the surplus argument will become harder to push aside. But with inventories this low, the market has not earned the right to ignore short-term supply risk either. Oil may be losing its war premium, but it has not rebuilt its safety buffer.

Source: IEA

Technical outlook

Oil is no longer trading like a market priced for disruption. After the US-Iran peace agreement, the price shows a clear unwind of the risk premium that pushed prices toward 119.50. That move was largely built on fear of supply disruption, shipping risk, and the possibility of a wider regional conflict. Now that those risks have eased, the market has quickly adjusted back toward more normal pricing conditions.

The fall toward 69.50 tells us that traders are no longer willing to pay the same premium for uncertainty. Technically, the most important area is now 68–72.50. This is where several signals meet: the former breakout zone, the 126-day moving average, and recent short-term support. That makes it a key decision area for the market.

If buyers defend this zone, oil can stabilize and begin to rebuild a base. But if this area fails, the chart starts to look much weaker because there is less technical support underneath until the market approaches the 60 area and then the major support around 55.20.

Scenarios ahead

The first scenario is stabilization. For that to develop, oil needs to hold above 68–70 and then recover above 72.50. That would show that the selling pressure is starting to fade and that the market is no longer only reacting to the removal of geopolitical risk. In that case, attention would shift back to demand, inventory data, OPEC+ policy, and global growth expectations. If price can reclaim 72.50, the next important level to watch would be 79.50, which may act as the first real resistance after the selloff.

The second scenario is a deeper correction. If oil breaks clearly below 68, it suggests that the peace agreement has removed most of the geopolitical premium and that the market is now exposed to softer demand concerns and supply-side pressure. In that case, 60 becomes the first downside area to watch, followed by 55.20 as the bigger structural support. Overall, oil is at an important turning point. Holding the current zone could lead to stabilization, while losing it would keep sellers in control.

Source: Trading view