US-Iran framework could reshape oil risk

US-Iran 14-point framework has eased some of the most immediate fears around Middle East energy disruption, the Strait of Hormuz may reopen under the draft agreement, yet questions over who controls the waterway, when frozen Iranian assets are released, and how quickly the deal can be formalized still leave oil markets exposed to political risk.

A formal signing is expected in Switzerland on Friday.

A rise in the US oil surplus could strengthen America’s role as a balancing force.

The Strait of Hormuz remains the key market issue.

US-Iran framework lowers immediate oil risk

The reported US-Iran framework has changed the tone in crude, but not because traders suddenly believe the region is stable.

It changed the tone because the market now has a reason to reduce the worst-case scenario. For weeks, the main fear was that military pressure between Washington and Tehran could spill into the Strait of Hormuz. That risk matters because Hormuz is not just a political headline. It is one of the most important energy routes in the world, and any serious disruption there would quickly feed into shipping costs, insurance premiums, refinery planning and physical supply expectations.

The market is not pricing a durable settlement yet. It is pricing a pause in escalation risk. That is an important difference. A pause can cool prices. A durable deal can change the entire risk structure. The framework has delivered the first part, but not yet the second.

Hormuz is still the real test

The Strait of Hormuz remains the detail that will decide whether this framework becomes a genuine relief for oil markets or just another temporary headline.

Trump has said the strait will reopen permanently and toll-free. For oil consumers, refiners and shipping companies, that is the sentence they want to hear. It suggests lower transport risk, more predictable cargo flows and less pressure on global supply chains.

Iranian state media, however, has described the reopening as taking place under Iranian arrangements.

That phrase is where the market problem begins

If Hormuz is open but the rules are unclear, oil traders will not treat the risk as fully gone. Tankers can move through a waterway, but insurers still need to price the political risk around that movement. Refiners can plan cargoes, but they need confidence those cargoes will not become hostage to the next dispute. Buyers can return to normal routes, but only if they believe the route is commercially neutral, not politically conditional.

Frozen assets could slow down the next stage

The frozen-assets issue may become the first real test of whether the framework can survive beyond the headline.

Iran’s Deputy Foreign Minister Kazem Gharibabadi has said the 60-day talks will not begin until the US releases billions in frozen assets, reportedly up to $24 billion. From Tehran’s perspective, this money is not a side issue. It is proof that Washington is serious about sanctions relief and not only asking Iran to make concessions first.

The US appears to reject that sequence

American officials are treating the deal more like a pay-for-performance arrangement. In that version, Iran must implement its commitments before any major funds are released.

That is not a technical disagreement. It is the core trust problem inside the framework.

Iran wants cash before deeper talks. The US wants compliance before cash. Both positions make political sense for their own side, but together they create a fragile starting point. If the first stage after the signing becomes a dispute over sequencing, the oil market may quickly move from relief back to caution.

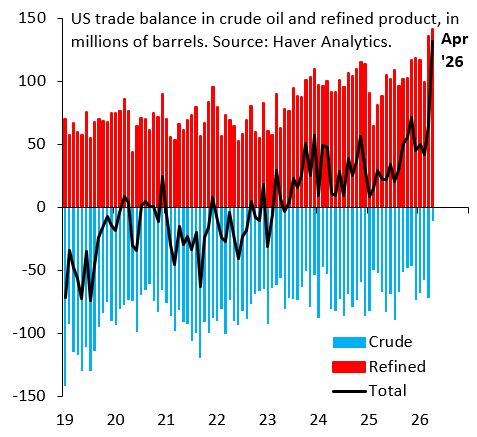

The US oil surplus changes the backdrop

The monthly US oil surplus reportedly rose to 131 million barrels from 65 million in March. This should not be treated as a normal monthly swing. It points to a broader shift in trade flows and to the US having more ability to act as a balancing force during a period of global disruption.

That matters because every Middle East crisis forces the same question: if supply from the region becomes less reliable, where does the market find flexibility?

The US cannot replace the Strait of Hormuz. The volumes moving through the route are too large, and the potential shortage from any serious disruption would be measured in tens of millions of barrels per week and hundreds of millions of barrels over a month. No single producer can close that gap completely.

The point is that a larger US surplus can absorb part of the shock. It gives the market more time, gives buyers more optionality and gives global trade flows more room to adjust before panic takes over. That is exactly why the April shift matters. The US did not remove the Hormuz risk, but it helped reduce the sense that the market had no buffer if the situation deteriorated.

A stronger US surplus gives Washington more leverage and gives traders a reason to believe that any disruption may still be painful, but not automatically uncontrollable. The US is not only entering the talks as a political power. It is entering them with a stronger energy position than in many previous Middle East crises.

Source: Strategic Petroleum Reserve