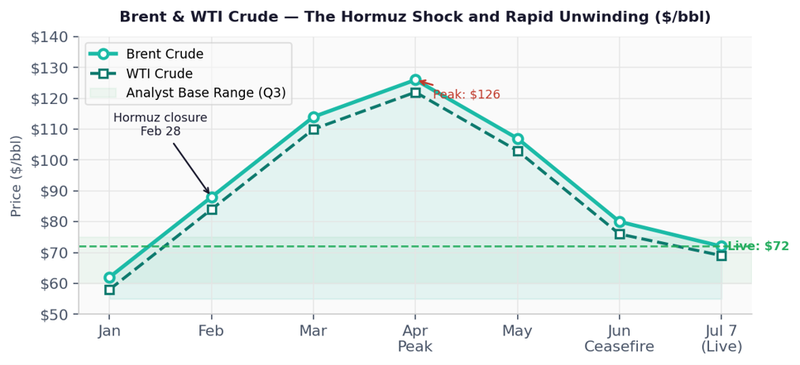

Oil's rapid reversal after the Strait of Hormuz crisis

Oil enters the third quarter in a very different position from where it began the year. After surging above $120 a barrel on fears of a major supply disruption, prices have fallen sharply as geopolitical tensions eased and underlying market fundamentals re-emerged. The focus now shifts to whether recovering supply, inventory levels and global demand will keep prices under pressure in the months ahead.

Brent climbed above $100 for the first time since 2022.

EIA revised its global oil demand forecast from growth of 1.2 million barrels per day in February to a contraction of 1.1 million barrels per day in June.

Oil inventories declined by an estimated 6.3 million barrels per day during the second quarter.

A market that has gone full circle

Few markets have seen a bigger turnaround than crude oil in the first half of 2026. Brent opened the year near $62 a barrel, elevated compared with previous yearly openings but still consistent with the structural oversupply that defined 2025, when OPEC+ was managing excess production through voluntary cuts while struggling with weak compliance.

Within six weeks of the United States and Israel launching air operations against Iran on 28 February, Brent had climbed above $100 for the first time since 2022 and peaked above $126 in April. The Strait of Hormuz, the waterway through which roughly 20% of global seaborne crude oil and liquefied petroleum gas trade passes, was closed to most tanker traffic. The largest disruption to global energy supply since the crises of the 1970s had arrived without warning.

By 7 July 2026, Brent was trading near $72 a barrel, not far from where it started the year. That full reversal, completed in roughly 22 weeks, is one of the clearest examples of how quickly commodity markets can reprice. It also highlights how geopolitical shocks, market mechanics and structural supply forces interact once acute disruption begins to fade. Understanding why oil has now given back its conflict-related risk premium is more useful for assessing the third-quarter outlook than simply knowing where prices peaked.

Why did oil prices fall so quickly?

The drop from $126 to $72 was driven by several factors. The US-Iran ceasefire framework, signed in mid-June, which included a 60-day ceasefire and the reopening of the Strait of Hormuz, removed the catastrophic risk that had kept prices elevated. Even before the ceasefire, demand destruction was accelerating faster than the US Energy Information Administration (EIA) had projected. The agency revised its global oil demand forecast from growth of 1.2 million barrels per day in February to a contraction of 1.1 million barrels per day in June, a swing of 2.3 million barrels per day in just four months.

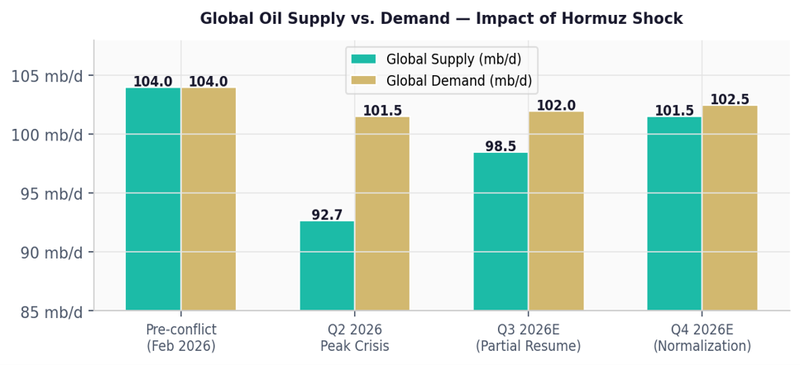

At the same time, Atlantic Basin producers moved quickly to fill the gap left by Middle Eastern exporters. The International Energy Agency (IEA) raised its 2026 supply growth forecast for the Americas by more than 600,000 barrels per day, with the United States reaching record production of 13.6 million barrels per day alongside rising output from Brazil and Canada. The structural oversupply that defined 2025 never disappeared. The conflict merely masked it for a few months.

Supply is returning faster than expected

As of 7 July, the recovery in the Strait of Hormuz is progressing faster than many institutions expected in their June forecasts. At least eight Japanese vessels have exited the strait via a route near Iran, including five very large crude carriers capable of transporting up to 2 million barrels each.

Saudi Aramco's exports are approaching pre-war levels, and the company cut the August price of its Arab Light grade for Asian buyers by $11 a barrel to a discount of $1.50 against the regional benchmark. That pricing structure has not been seen since the oil price wars of 2020 and 2015, signalling that Riyadh is prioritising market share over price defence.

OPEC+ has also approved an additional quota increase of 188,000 barrels per day for August, its fourth consecutive monthly increase, bringing cumulative production increases since April to roughly 800,000 barrels per day.

Low inventories are still supporting prices

The main challenge to the bearish third-quarter outlook is the remaining inventory deficit. OECD oil inventories declined by an estimated 6.3 million barrels per day during the second quarter, an exceptional drawdown that reduced days of forward cover to their lowest level since 2003. Even as navigation through the Strait of Hormuz resumes, rebuilding those inventories will take time.

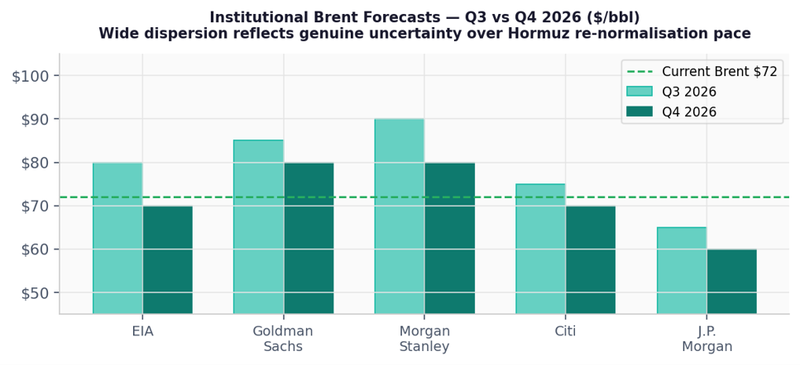

The market will need a sustained supply surplus before crude stocks return to levels that ease upward pressure on prices. The US Energy Information Administration's base case sees Brent averaging around $80 a barrel in the third quarter before declining towards $70 a barrel by year-end.

What traders should watch next

For traders, the third-quarter outlook remains structurally bearish, but with meaningful upside risks tied to geopolitical events. The base case, continued recovery in Hormuz, OPEC+ gradually unwinding its production cuts and a partial recovery from demand destruction, points to Brent trading within a $68 to $80 range during the quarter. The main downside risk is a faster-than-expected inventory rebuild, which could accelerate a move back towards the pre-conflict $60 area.

The clearest upside risk is a breakdown of the US-Iran ceasefire framework. That possibility cannot be dismissed. Formal negotiations have already been frozen once, and Iran was linked to an attack on a vessel in the Gulf of Oman after the memorandum of understanding was signed. Markets have now removed almost all the geopolitical risk premium from oil prices. That also means any credible sign of renewed escalation would likely be priced in quickly. Traders holding short positions should keep that risk firmly built into their position management.