The ECB faces a difficult third quarter

The European Central Bank enters Q3 facing one of the toughest policy balancing acts among the world's major central banks. The ECB's June decision marked a clear shift. Policymakers raised key interest rates by 25 basis points. ECB could justify pausing after June's rate hike. But if gas prices remain elevated, food prices rise further or wage settlements accelerate, policymakers may be forced to raise rates again despite weak growth.

ECB's next monetary policy meeting scheduled for July 22-23, incoming inflation, energy, PMI and wage data will be closely watched by markets.

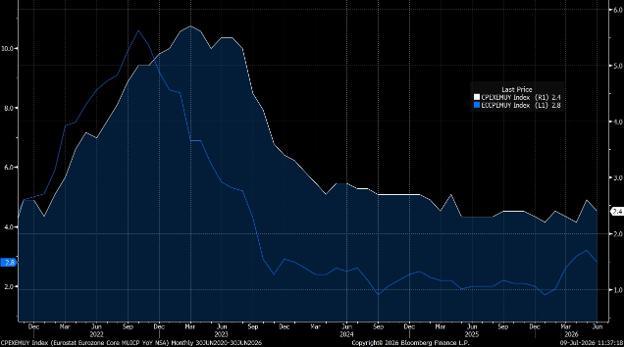

Eurozone inflation eased to an estimated 2.8% in June from 3.2% in May.

The ECB's real test in Q3 is whether the energy shock begins to feed into wages, services prices and longer-term inflation expectations.

A difficult balance between energy inflation and weak growth

The European Central Bank enters Q3 facing one of the toughest policy balancing acts among the world's major central banks. After raising interest rates by 25 basis points in June, the ECB is no longer focused solely on the final stage of bringing inflation down. It is now dealing with a fresh energy-driven inflation shock linked to the Middle East conflict, while growth across the euro area remains fragile. With the ECB's next monetary policy meeting scheduled for July 22-23, incoming inflation, energy, PMI and wage data will be closely watched by markets.

Source: Bloomberg

Inflation remains the ECB's biggest challenge

The ECB's June decision marked a clear shift. Policymakers raised key interest rates by 25 basis points, citing higher energy prices and the need to keep medium-term inflation anchored around its 2% target. The latest Eurosystem staff projections forecast headline inflation averaging 3.0% in 2026, 2.3% in 2027 and returning to 2.0% only in 2028. Core inflation is also expected to remain sticky, averaging 2.5% in both 2026 and 2027 before easing to 2.2% in 2028.

However, the case for another immediate rate hike is less clear. Eurozone inflation eased to an estimated 2.8% in June from 3.2% in May, while the services PMI improved but remained weak at 49.4, still signalling contraction. The composite PMI rose to 50.0, pointing to stabilisation rather than a strong recovery. Together, these figures suggest the euro area economy is not overheating but instead absorbing an external energy-driven price shock.

Source: Bloomberg

Why the ECB is likely to remain cautious

This is where the policy challenge becomes more nuanced. The ECB is unlikely to react to the headline inflation rate alone. Instead, it will focus on how broad and persistent the inflation shock proves to be. A temporary rise in oil or gas prices reduces consumers' real incomes and weakens demand. Raising interest rates too aggressively in response risks deepening the slowdown without increasing energy supply.

This was also the central argument in the Bloomberg Opinion piece, which warned that Europe is already facing higher energy costs and that tightening policy too quickly could worsen the demand shock, particularly for manufacturers already under pressure from the loss of cheap Russian gas and Chinese overcapacity. The analysis also noted that longer-term inflation expectations remained close to the ECB's 2% target, supporting a cautious rather than automatic tightening response.

What should traders watch?

The ECB's real test in Q3 is not whether inflation is above target, it clearly is. The bigger question is whether the energy shock begins to feed into wages, services prices and longer-term inflation expectations. If those expectations remain anchored and core inflation continues to moderate, the ECB could justify pausing after June's rate hike. But if gas prices remain elevated, food prices rise further or wage settlements accelerate, policymakers may be forced to raise rates again despite weak growth.

Our base case is that the ECB will maintain a tightening bias while avoiding any pre-commitment to another rate hike in July. The likely message is one of data dependence and vigilance. For markets, this means the euro could remain supported by interest rate differentials during periods of hawkish repricing. However, European equities, particularly industrials and other rate-sensitive sectors, remain vulnerable if investors conclude that the ECB is tightening into a stagflationary shock rather than responding to genuine demand-led inflation.