BoE faces a harder June decision as inflation risks return

The Bank of England is moving into its June 18 meeting with a much less comfortable inflation story than it had hoped for. UK inflation eased to 2.8% in April, but the relief is not clear.

Megan Greene says the case for a rate hike is getting stronger.

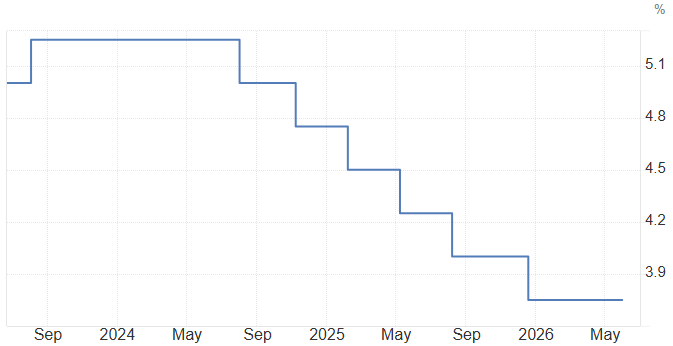

The OECD expects the BoE to hold rates steady before cutting in 2027.

Inflation has cooled, but energy shocks could push it higher again.

Quantitative tightening has already reduced banking reserves sharply.

The rate-cut story is no longer simple

Only a short time ago, the BoE debate looked mostly about when rate cuts could restart. That is no longer the cleanest way to look at it.

MPC member Megan Greene has now argued that the case for raising rates is strengthening as the Middle East conflict drags on. Her concern is not just that energy prices rise for a few weeks.

The bigger risk is that higher energy costs feed into wider price-setting behaviour, wage demands and inflation expectations. That matters because central banks can usually look through temporary energy shocks. But they have a harder time ignoring repeated shocks that start to change how households and businesses behave.

Source: Bank of England

Greene is warning against waiting too long

Greene’s message is important because it challenges the idea that the BoE can simply wait and observe. She has suggested that a move from 3.75% to 4.0% may become necessary if inflation risks continue to build.

The argument is straightforward. If the BoE waits until the inflation shock is fully visible in the data, it may already be too late. By then, businesses may have raised prices again, workers may have pushed harder for wage increases, and inflation expectations may have become more difficult to control.

The OECD sees a different path

The OECD is taking a more cautious view. It expects the BoE to keep rates steady for the rest of the year before delivering a quarter-point cut to 3.5% in 2027.

That difference matters. Greene is focused on inflation risk from geopolitics. The OECD is looking more at the broader economy and the possibility that high rates are already doing enough to slow demand. This leaves markets with two very different stories. One says the BoE may need to tighten again to protect credibility. The other says the central bank should avoid overreacting to energy volatility and wait for inflation to settle.

QT is quietly changing the background

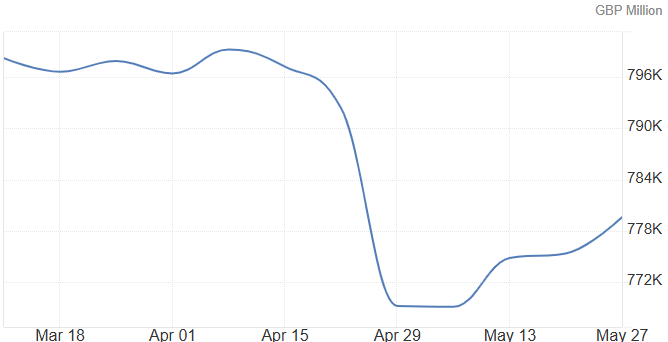

Bailey also updated lawmakers on quantitative tightening, noting that the BoE’s stock of banking reserves has fallen to roughly £640 billion from a peak of around £980 billion.

That is important because QT is already tightening financial conditions in the background. Even if the Bank Rate stays at 3.75%, the shrinking reserve base means the BoE is still withdrawing liquidity from the system. This gives policymakers another reason to move carefully. Raising rates while continuing QT could send a strong anti-inflation message, but it could also increase pressure on an economy that is not exactly strong.

Source: Bank of England

The BoE is caught between credibility and caution

For now, the BoE’s problem is that neither option looks easy. Holding rates steadily risks looking too relaxed if energy-driven inflation becomes persistent. Hiking to 4.0% risks tightening into a fragile economy, especially when QT is already doing some of the work.

That is why the June meeting now feels more sensitive. Inflation has come down, but not enough to give the BoE comfort. Geopolitical risk is still feeding into energy prices. And policymakers are divided between acting early and waiting for clearer evidence.

The BoE may still hold rates steady, but the tone around that decision is becoming more hawkish. The market is no longer debating only when cuts arrive. It is now being forced to ask whether the next move could still be up.