BOJ bond-buying pause leaves yen exposed to intervention risk

The Bank of Japan is trying to manage two risks at the same time. Inflation pressure is rising, the yen is weak, and crude costs are feeding into domestic prices. But the BOJ also does not want long-term Japanese bond yields to rise too quickly, especially after years of heavy central-bank support.

BOJ paused its bond-buying taper to avoid a sharp rise in long-term yields.

Deputy Governor Ryozo Himino warned inflation could overshoot the 2% target.

Yen weakness has brought intervention risk back into focus.

BOJ is trying to control the pace of normalization

The BOJ’s decision to pause its bond-buying taper should not be read as a simple dovish signal.

Japan is no longer in the old zero-rate world, but it is also not ready for a disorderly bond-market adjustment. By keeping monthly Japanese Government Bond purchases around 2 trillion yen, the BOJ is trying to stop long-term yields from rising too sharply while it continues moving slowly toward policy normalization.

That balance matters.

If the BOJ tightens too aggressively, bond yields could climb in a way that pressures households, companies and government financing costs. But if it moves too slowly, the yen may weaken further, import costs may rise, and inflation could become harder to contain.

Inflation pressure is harder to ignore

The inflation story is becoming more uncomfortable for the BOJ.

Deputy Governor Ryozo Himino warned that underlying inflation risks overshooting the 2% target. That matters because Japan’s inflation pressure is no longer only about one temporary shock. Higher crude prices, yen weakness and rising wholesale costs are starting to create a broader policy problem.

Japan is especially sensitive to this because it imports much of its energy. When oil prices rise and the yen weakens at the same time, companies pay more for fuel, raw materials and imported goods. Those costs first appear in wholesale prices, but they can gradually move into consumer prices as firms pass them on.

That is why the BOJ cannot simply ignore the currency.

A weak yen may help exporters, but it also makes daily costs more painful for households. Once that pressure becomes political, the central bank’s patience becomes harder to defend.

Source: Ministry of Internal Affairs & Communications

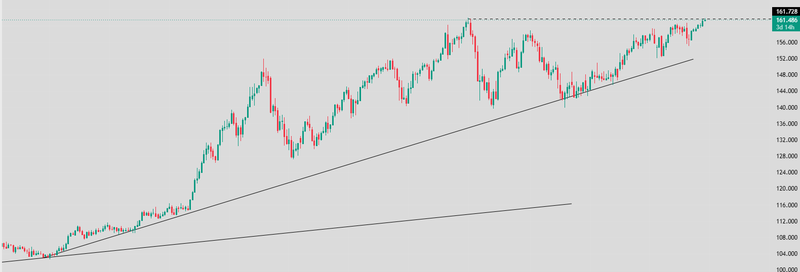

Yen weakness brings intervention risk back

After Finance Minister Katayama and US Treasury Secretary Bessent held an emergency online meeting, USD/JPY quickly moved lower. The move was not necessarily a sign that direct intervention had already happened. It was more likely driven by verbal intervention and by market expectations that Japan could step in if the yen weakened further.

That meeting mattered because its signal that Japan is close to intervene in the currency market after coordinating closely with the United States.

The 161 area is especially important because it has become the level where markets start watching for possible action. It is around this zone that intervention fears tend to intensify, and traders now treat it less like a normal technical level and more like a policy threshold.

The interest-rate gap still supports the dollar against the yen, especially while US rates remain much higher than Japanese rates. But the closer USD/JPY moves toward that 161 area, the more unstable the upside becomes. The pair may rise for days on yield logic, then fall quickly if officials signal that the move has become excessive.

Source: Trading view

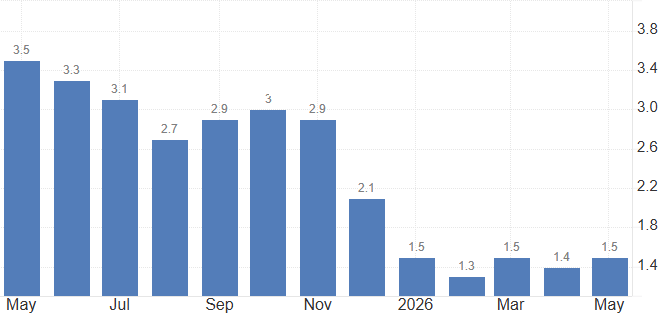

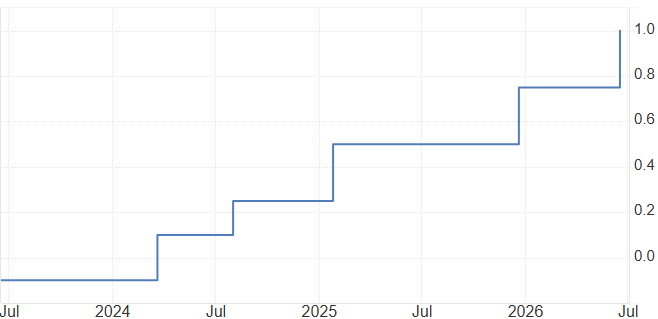

Why may September be so early

A September BOJ rate hike is possible, but it does not look like a clean base case.

The bank needs more time to evaluate third-quarter inflation data. Officials want to see how much summer consumer prices accelerate after the recent Middle East energy shock. If higher crude costs feed deeply into domestic prices, the case for another hike becomes stronger. If the pressure fades, the BOJ may prefer to wait.

That is why October looks more realistic, markets are still pricing a gradual tightening cycle, with a strong chance of another 25-basis-point hike to 1.25% by October. The BOJ does not want to fall behind inflation, but it also does not want to shock the JGB market.

Source: Bank of Japan