BOJ faces a harder choice as JGB yields test Japan’s policy limits

The Bank of Japan is being pulled in two directions at once. Inflation pressure is still strong enough to keep markets pricing another rate hike, but the bond market is already under heavy strain.

BOJ is facing pressure to soften its bond-tapering path.

Markets are pricing a high probability of another short-term rate hike.

The 10-year JGB yield recently reached around 2.58%.

Japan’s bond market is no longer calm

The rise in the 10-year JGB yield toward 2.58% is important because it shows investors are demanding more compensation to hold Japanese debt. Part of that is about inflation. Part of it is about the BOJ stepping away from years of ultra-loose policy. But part of it is also about confidence in Japan’s fiscal position. That is where the situation becomes more sensitive. Higher yields do not only affect traders. They also raise the cost of financing a government that already carries one of the largest debt burdens in the developed world.

Source: Trading economics

The BOJ may slow the taper, but not abandon tightening

The BOJ is now facing calls to pause or temper its bond-tapering programme for fiscal year 2027. That would mean slowing the pace at which the central bank reduces its bond purchases, giving the market more support at a time when yields are rising quickly.

That kind of move would not necessarily mean the BOJ is giving up on policy normalization. It may simply mean the central bank wants to separate two issues: short-term interest rates and bond-market functioning. BOJ could still raise rates while slowing quantitative tightening. That may sound contradictory, but it reflects the difficult balance Japan now faces. The central bank wants to fight inflation without creating disorder in the bond market.

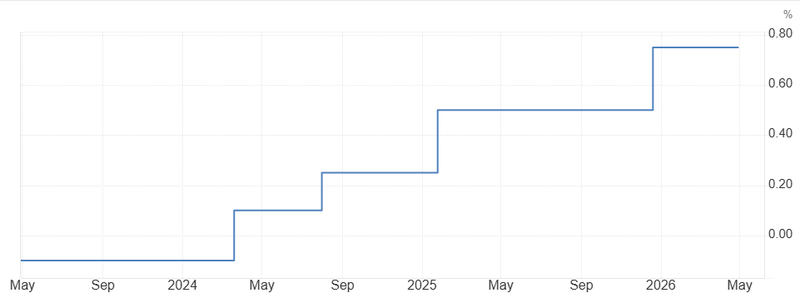

Rate-hike pressure is still there

Markets are still assigning a strong probability to another BOJ rate hike, with expectations focused on a possible move from 0.75% to 1%. Reuters reported that a June hike is widely expected, while the BOJ is also set to review its tapering strategy through March 2027 at its June meeting. That matters because inflation pressure has not disappeared. A weak yen, higher energy costs and Middle East-related risks are all making imported inflation harder to ignore. If the BOJ waits too long, it risks looking behind the curve again.

Source: Bank of Japan

The political pressure is becoming harder to ignore

The bond market is now creating a direct challenge for Prime Minister Sanae Takaichi’s government. Slower quantitative tightening could help ease pressure on JGB yields and limit the rise in debt-servicing costs, especially if fiscal spending remains heavy.

That is why this is no longer a clean central-bank story. It is becoming a policy coordination problem. The BOJ wants credibility on inflation. The government wants borrowing costs contained. Investors want reassurance that the bond market will not become unstable.

Japan is entering a more fragile policy phase

For now, the most likely path is not a dramatic reversal, but a softer version of normalization. The BOJ may still hike rates, but it may also signal more caution on bond tapering to avoid adding stress to an already volatile market.

That would show how delicate Japan’s transition has become. After years of ultra-low yields, the country is trying to move back toward normal monetary policy. But the move is happening at a time when inflation is sticky, global energy risks are high and government debt costs are rising. The message from the bond market is clear. Japan can still normalize policy, but it cannot do it carelessly. At 2.58% on the 10-year JGB, every BOJ decision now carries more weight than before.