Emerging markets are beating the S&P 500, is wall street missing the signal?

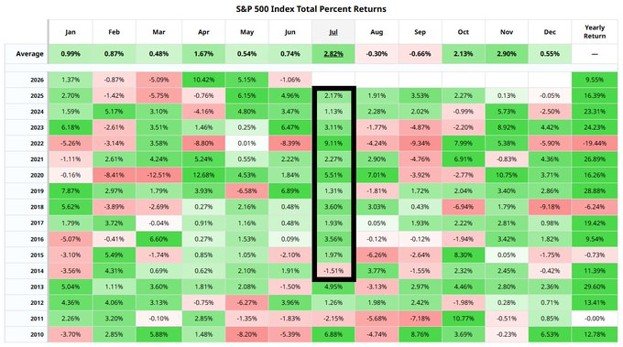

The S&P 500 enters July with a strong seasonal tailwind, but not with a clean macro setup. Since 2015, July has usually been kind to U.S. equities, with the S&P 500 finishing higher each time. That history helps explain why investors are still comfortable holding risk. But seasonality is only one part of the story

July has been supportive for the S&P 500, but August and September have been much harder months.

Credit spreads remain tight even as inflation pressure and Fed risk return.

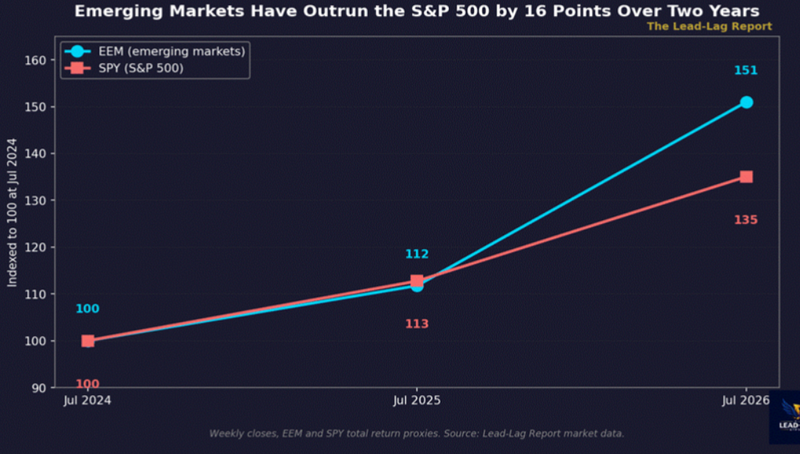

EEM has outperformed S&P500, rising about 51% over the last 2 years.

The market is pricing confidence, not caution

The S&P 500’s rally still looks strong on the surface. A 35% gain over two years is not a tired market. It shows investors still believe earnings strength, AI leadership and deep U.S. liquidity can keep valuations supported.

But the relative move in emerging markets is becoming harder to ignore. EEM climbed from 43.63 to 65.88 over the same two-year period, a gain of around 51%. Over the last twelve months alone, EEM is up roughly 35%, compared with about 20% for the S&P 500.

That does not mean the S&P 500 is suddenly weak. It means the market is starting to widen out. Investors are no longer looking only at the most crowded U.S. mega-cap trade. Some capital is clearly finding better value, cleaner positioning or stronger upside outside the U.S.

That is an important shift

For much of the rally, the market was comfortable paying a premium for U.S. exceptionalism. The S&P 500 had the AI story, the strongest earnings leadership and the deepest liquidity. But when emerging markets begin outperforming by that kind of margin, it suggests investors are starting to question whether all the good news is already priced into U.S. equities.

Source: LeadLag

The divergence is the signal

The market’s narrative still sounds bullish. Semiconductors remain strong. AI remains the dominant equity story. Geopolitical risk has eased enough for investors to stay focused on earnings rather than shock risk.

But the data is not as clean

Inflation is still sticky. Fed language is becoming less comfortable for risk assets. Credit spreads remain tight, which suggests investors are not pricing much stress. That combination can hold for a while, but it cannot stay disconnected forever.

If inflation cools and yields stay contained, the S&P 500 can continue to justify its valuation. But if inflation refuses to fall quickly and the Fed keeps the “higher for longer” message alive, the index will have to work much harder.

A strong semiconductor tape can hide a lot of pressure. It cannot erase the cost of capital. That is why the EEM move matters. It is not only about emerging markets doing well. It is about the possibility that investors are quietly looking for a less crowded trade while the S&P 500 still looks strong on the surface.

July helps, but it does not protect the market

July seasonality gives the S&P 500 cushion, but it is not protection.

Markets often behave well in July because positioning is supportive, earnings optimism builds, and liquidity is still manageable. But August and September are usually less forgiving. They tend to expose crowded trades, especially when investors enter late summer with high valuations and very little risk premium.

The S&P 500 is not entering late summer from a cheap level. It is entering with strong gains already priced in, tight credit spreads and a belief that the Fed will not need to tighten much further. If that belief is challenged, the adjustment could come faster than investors expect.

Source: Bar chart