Fed rate-hike returns as Logan questions whether policy is tight enough

The Federal Reserve debate is starting to shift again. For months, markets were mainly focused on when the next rate cut might arrive. Now, Dallas Fed President Lorie Logan is warning that the current policy rate may not be doing enough to restrain inflation

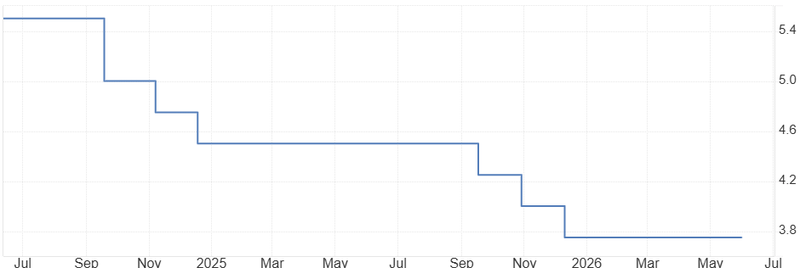

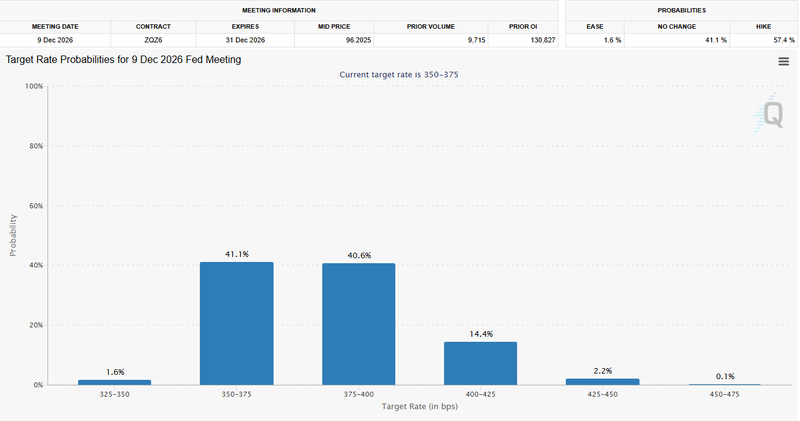

Markets are pricing a rising probability of a year-end rate increase.

Beige Book contacts reported prices rising at a moderate-to-strong pace.

Kevin Warsh may try to make the Fed speak with a more unified voice.

The Fed is no longer only debating cuts

The important part of Logan’s message is that she is not simply asking for patience. She is questioning whether policy is restrictive enough at all.

That matters because the Fed’s current target range of 3.5% to 3.75% was supposed to keep enough pressure on demand while inflation moved back toward 2%.

But the economy has not cooled down in a clean way. Corporate earnings remain resilient, AI-related spending is still feeding growth, and easier financial conditions are giving markets a sense of confidence that may work against the Fed’s inflation fight.

Source: federal Reserve

AI strength is becoming part of the inflation debate

The AI boom is usually discussed as a productivity story. Over time, it may help companies become more efficient and reduce costs. But Logan’s concern is more immediate. Right now, AI investment is also creating demand for data centres, power, construction, chips and skilled labour.

That can support growth, but it can also keep inflation pressure alive. If the demand boost arrives before the productivity benefits, the Fed may not get the disinflationary help it was hoping for. That is why strong markets are not automatically good news for policymakers. A booming AI sector may support the economy, but it can also make the Fed’s job harder.

The Beige Book adds to the concern

The latest Fed survey added another uncomfortable signal. Most regional districts reported that prices were rising at a moderate-to-strong pace, with inflation pressure spreading through areas linked to energy, transport, groceries and input costs.

This does not mean inflation is out of control. But it does mean the Fed has less room to sound relaxed. If price increases are broadening again, even slowly, policymakers will be more careful about suggesting that the next move is lower.

That is why market pricing has changed. Futures markets are now assigning a much higher probability to a rate increase by year-end, with some reports putting the implied chance around 55%.

Source: CME Group

Warsh may also change the Fed’s communication style

Kevin Warsh’s arrival adds another layer. He has long favoured a more disciplined communication style, and he is expected to push for a Fed that speaks with one clearer voice rather than a constant stream of competing speeches from regional presidents.

That could matter for markets. In recent years, investors have often reacted not only to Fed decisions, but to every individual official’s speech. A more restrained media presence could reduce noise, but it could also make each official signal more important.

For now, the message is clear. The rate-cut narrative has weakened, and the risk of another hike is back on the table. The Fed is facing an economy that is not weak enough to calm inflation fears, but not strong enough to ignore the damage from higher rates.

Add in AI-driven demand, strong earnings, geopolitical pressure on energy prices and a Beige Book showing broader price increases, and the policy path becomes much less comfortable. Logan’s warning may not guarantee a hike. But it does change the tone. The Fed is no longer only asking when it can ease. It is being forced to ask whether it eased too soon, and whether tighter policy may still be needed before inflation is truly under control.