Gold’s refusal to break shows the market is trading more than fear

If this were only a war-premium trade, gold should have followed crude lower as oil prices deflated this week. It did not. Instead, gold held firmly above $3,800 even as the dollar strengthened and yields jumped. That refusal matters because the market was stress-tested against the exact mix that normally hurts bullion: a firmer dollar, higher yields and a hawkish policy surprise.

Gold held firm even as the dollar strengthened and yields moved higher.

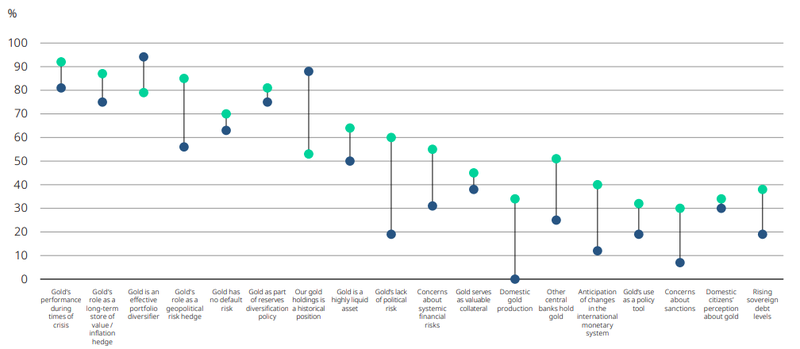

Central banks continue to hold gold for crisis protection, diversification and geopolitical hedging.

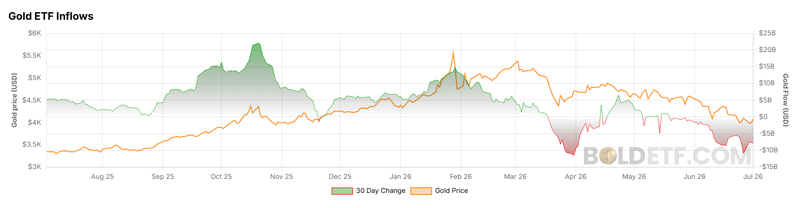

Thirty-day gold ETF flows are around negative $5 billion.

Gold does not behave like a simple war trade

The market often treats gold as a fear asset, but that explanation is too narrow for the current move.

Oil has fallen as supply fears eased, which should have weakened the geopolitical premium across commodities. If gold were only following that same fear channel, the metal should have sold off more aggressively. Instead, it held its ground. That tells us another force is supporting the market.

A deflating oil complex can lower the forward inflation path. If investors believe lower energy prices will reduce future inflation pressure, nominal yields may not need to rise as much. More importantly for gold, real yields can start to soften if the market believes the Fed will eventually face less inflation pressure. Gold cares about that difference. It does not trade only on whether yields rise today. It trades on whether the future path of real rates becomes easier or tighter.

The dollar has strengthened. Yields have jumped. A hawkish Fed surprise should have hurt gold more than almost anything else. But the metal still refused to break. That does not mean gold is immune to higher real yields. It means investors are not ready to abandon it just because the Fed story has become less comfortable.

Part of that is because the Fed itself has become a source of uncertainty

The market is still trying to understand the policy style under Kevin Warsh. If the Fed communicates less, gives fewer forward signals and leaves decisions more tied to incoming data, investors have less clarity about the future path of policy. Gold benefits from that uncertainty. It is the asset that does not depend on which chair controls the press conference, how the dot plot is framed, or whether markets correctly interpret the next inflation print.

Central-bank demand gives gold a deeper floor

Around 92% of respondents said gold’s performance during crises is a main reason for holding it, compared with 81% of advanced economy central banks. That is a strong signal. For reserve managers, gold is not just a price trade. It is insurance against events that do not fit neatly into a yield model.

Gold’s long-term role as a store of value and inflation hedge was cited by 84% of respondents, while 83% highlighted its role as a portfolio diversifier. Those numbers show that central banks are not holding gold for one reason. They are holding it because it works across different kinds of stress: inflation, sanctions risk, currency volatility, financial instability and geopolitical fragmentation.

Around 85% of emerging-market central banks see gold as a geopolitical hedge. That matters because emerging markets understand reserve vulnerability better than anyone. For them, gold is about returns. It is about control. It is an asset that sits outside another country’s payment system and outside another central bank’s promise.

Source: World Gold Council

ETF outflows have not destroyed the gold market

Thirty-day gold ETF flows are around negative $5 billion, which shows that some financial investors are reducing exposure. That pressure is real. ETF selling can weigh heavily on paper-market prices, especially when the dollar is strong and yields are rising. But ETF flows are not the whole gold market. They reflect tactical investor appetite, not the full reserve-demand story.

Western portfolio investors may be trimming gold because cash and bonds look more attractive in the short run. Central banks are still thinking in years, not weeks. They are not asking whether gold can outperform the S&P 500 next month. They are asking whether their reserves are too dependent on dollars, Treasuries and the Western financial system.

Source: Bold report