Gold trapped between central-bank demand and Fed rate risk

Gold is caught between two powerful forces. On one side, central banks are still sending a strong long-term signal of demand. On the other side, the Federal Reserve is becoming less friendly for non-yielding assets, with nearlyHalf of policymakers now pointing to at least one possible rate hike later this year.

Central banks still expect global gold reserves to rise.

Fed rate-hike risks are limiting gold’s upside.

Bank of China bought 10 tonnes of gold in May.

Central banks demand is important

According to the World Gold Council’s latest central bank survey, 89% of respondents expect global central bank gold reserves to increase over the next 12 months. Even more important, a record 45% expect their own institutions to increase gold holding over the same period. That matters because central banks do not usually buy gold for quick trade. They buy it for reserve diversification, currency protection and long-term balance-sheet security.

Gold is no longer being treated only as a crisis hedge. It is increasingly being treated as a strategic reserve asset. For many central banks, the argument is simple: gold carries no credit risk, is not tied to one government’s debt market, and can act as protection when confidence in paper assets weakens.

That does not mean gold moves higher every day. But it does mean the market has a deeper buyer underneath it than in previous cycles.

China’s buying keeps the story alive

The Bank of China reportedly bought 10 tonnes of gold in May, the largest monthly increase since December 2024. The number itself is not enough to change the whole market. The timing is what matters.

China bought after a strong multi-year rally. That suggests the motive is not simply price. If Beijing were only looking for a cheap entry, it could have waited for a deeper pullback. Instead, the purchase points to a broader reserve strategy: gradually increasing gold exposure while reducing reliance on traditional dollar-linked assets.

For traders, this matters because China is not just another buyer.

When one of the world’s largest reserve holders keeps adding gold, it strengthens the belief that official-sector demand is structural. It also reminds the market that gold is supported by more than ETF flows, jewellery demand or short-term positioning.

Gold is becoming a reserve asset for a world where sanctions, debt concerns and geopolitical fragmentation are harder to ignore.

Source: MacroMicro

Fed is blocking a clean rally

The problem is that gold does not trade only on reserve demand. It also trades against the dollar, Treasury yields and real rates. That is where the Federal Reserve becomes the obstacle.

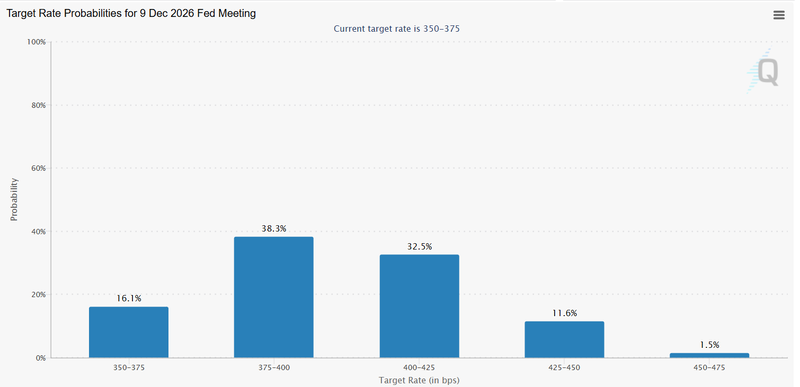

Nearly half of FOMC policymakers now expect at least one rate hike later this year. Markets have also moved in the same direction, with the probability of a December rate hike rising from around 70% to about 83%. That matters because gold does not pay interest. When rate expectations rise, cash and government bonds become harder to ignore.

This is the pressure point. Investors may still want gold for protection, but they also have to compare it with assets that offer income. Gold can have a strong long-term story and still struggle in the short term if real yields stay elevated. Traders may hesitate to chase the metal higher when the Fed is warning that policy could remain tight or become even tighter.

That is why the rally is not clean. Central-bank buying supports the downside, but Fed policy limits the upside. Gold is sitting between a structural bid and a monetary ceiling.

Source: CME Group

Oil has changed the safe-haven equation

Oil adds another layer because it affects both inflation and geopolitics.

Iran’s first crude exports in two months reportedly bypassed the fading US blockade, easing some fears around supply disruption. At first glance, that looks negative for gold because lower geopolitical stress can reduce safe-haven demand.

But the oil story is not that simple. If oil supply improves and energy prices ease, inflation pressure may cool. That could reduce the need for the Fed to keep policy aggressively tight, which would eventually help gold. But if the oil market remains unstable, inflation risks stay alive, and the Fed may have less room to sound dovish.

So gold is not just reacting to Middle East risk. It is reacting to what oil means for inflation, what inflation means for the Fed, and what the Fed means for real yields. That chain is what matters.

Lower geopolitical risk can weaken the safe-haven bid today. But lower oil-driven inflation can support gold later if it softens the Fed’s tone.

Gold still has a solid long-term foundation

Central banks are not behaving like short-term traders. They are increasing gold exposure because the reserve environment has changed. China’s 10-tonne purchase in May reinforces that message and keeps the official-sector demand story alive.

But the short-term driver is still the Fed

If policymakers continue to signal possible rate hikes, gold may struggle to build a clean breakout because real-rate pressure will remain in the way. If the Fed tone softens, especially if oil stabilizes and inflation fears cool, the same central-bank demand that is now supporting gold could become the base for a stronger move.

It has two stories pulling in opposite directions. The long-term reserve story is supportive. The short-term rate story is restrictive. Until one becomes stronger, gold may continue to trade in the middle, supported on dips but capped when rallies run too far.