UK CPI miss gives BOE more room to hold rates as oil prices fall

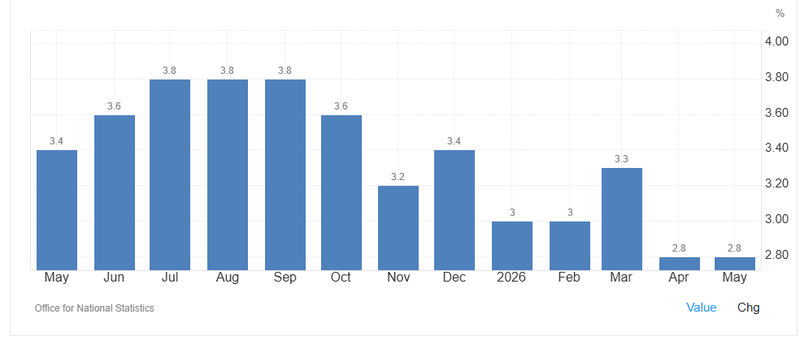

UK inflation came in softer than expected in May, strengthening the case for the Bank of England to keep interest rates steady. CPI held at 2.8%, below the 3% consensus forecast and well below the BOE’s earlier 3.3% projection, while falling oil prices after the US-Iran interim peace deal could reduce the risk of a renewed energy-driven inflation shock.

UK CPI held at 2.8% in May, below the 3% forecast.

The BOE had expected inflation to reach 3.3%.

Services inflation rose to 3.7% from 3.2%.

Food inflation fell to 2.2% from 3%.

UK inflation comes in softer than expected

UK inflation surprised to the downside in May, giving the Bank of England more room to maintain a wait-and-see approach on interest rates.

Consumer price inflation held steady at 2.8%, below both the 3% market consensus and the BOE’s earlier projection of 3.3%. The softer reading matters because policymakers had been preparing for the possibility that inflation could rise further this year, especially after higher energy prices threatened to feed into broader price pressures.

Source: TradingEconomics

The latest data does not remove the inflation problem completely. Domestic price pressures remain sticky in parts of the economy, especially services. But the headline miss reduces the urgency for the BOE to move toward another rate increase in the near term.

Services inflation remains the sticky part

The strongest upward pressure came from services.

Services inflation rose to 3.7% in May from 3.2% in April. That was above the 3.5% forecast and slightly higher than the 3.6% consensus view, though still below the BOE’s 3.9% expectation.

Airfares played a major role in the increase. Flight prices rose 10.3% in May, compared with a 5% fall during the same period last year. The move likely reflects the timing of Easter rather than a clear signal that higher energy costs are already feeding strongly into air travel prices.

There was also a base effect linked to the previous calculation error around the 2025 vehicle excise duty hike, which affected the annual comparison.

A narrower services measure watched by the BOE also moved higher. Excluding airfares, package holidays, education and accommodation services, annual services inflation rose to 3.9% from 3.4%. Another services gauge that removes volatile, indexed and regulated categories edged up to 3.8% from 3.7%.

These measures show why the BOE is unlikely to sound relaxed. The headline CPI miss helps, but underlying domestic inflation has not fully cooled.

Food and goods prices ease the pressure

The downside surprise was helped by softer food and goods inflation.

Food and non-alcoholic beverage inflation fell to 2.2% from 3%, a bigger decline than the expected move to 2.8%. Food prices matter for the BOE because households pay close attention to them when forming inflation expectations. A softer food reading can help reduce public concern that inflation is becoming entrenched again.

Core goods inflation also weakened, falling to 0.7% from 1.1%. The decline was concentrated in clothing and footwear, as well as furniture and household goods.

Those categories can be volatile, but the weakness suggests that supply-chain pressure from the Middle East conflict has so far had a limited impact on UK consumer goods prices. It may also show that weak demand is preventing companies from passing higher input costs fully to consumers.

That point is important because producer input costs have risen more sharply. The contrast between higher input inflation and subdued core goods inflation suggests firms may be absorbing some costs rather than pushing them directly into final prices.

Falling oil prices change the BOE outlook

The biggest shift in the inflation outlook may come from energy.

Before the US-Iran interim peace deal, inflation was expected to rise further this year and peak just below 3.5%. But the combination of the May CPI miss and the decline in oil and gas prices has created downside risk to that outlook.

If energy prices remain close to current levels, inflation could stay closer to 3% through the rest of the year rather than moving toward the earlier peak forecast. That would reduce the risk that the energy shock turns into a more persistent inflation problem.

For the BOE, this is a major development. A sustained fall in energy prices would give policymakers more space to hold rates steady instead of raising them again.

BOE may avoid a July rate hike

The latest data strengthens the case for patience.

A 25-basis-point rate hike in July had been a possible baseline if inflation continued to climb and energy prices stayed elevated. But softer headline CPI, lower food inflation and falling oil prices reduce the need for a near-term tightening move.

The BOE is still likely to remain cautious. Services inflation remains above 3.5%, and some underlying measures have ticked higher. That means policymakers cannot declare the inflation battle over.

Still, the balance of risks has changed. If the energy shock fades, the BOE can keep rates steady while waiting for clearer evidence on wages, services prices and demand.

What markets should watch next

The BOE’s next policy decision will be important not because rates are expected to move immediately, but because investors will look for guidance on how officials are reading the inflation mix.

The key question is whether policymakers focus more on sticky services inflation or on the softer headline CPI and lower energy prices.

A cautious hold would make sense. The BOE can acknowledge that domestic inflation remains sticky while also recognizing that falling oil and gas prices reduce the risk of a broader inflation surge.

Markets should watch three signals: whether the BOE keeps a tightening bias, whether it points to downside risks from lower energy prices, and whether it continues to view a future rate hike as necessary.