Bankruptcies expose weak yen and credit risk as BoJ tightening bites

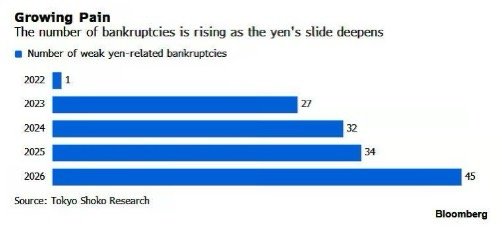

Between January and June, 45 Japanese companies declared bankruptcy due to currency depreciation, a 32.3% increase from a year earlier and the highest first-half total in four years. The number is still far below Japan’s historical insolvency peaks, so this is not yet a broad corporate crisis.

Weak-yen bankruptcies rose to 45 companies in the first half of the year.

The BoJ’s move away from ultra-low rates is raising refinancing pressure.

32.3% year-on-year increase and a four-year high for the first half.

Weak yen pressure is moving into the real economy

The yen’s weakness has been discussed mostly through the lens of inflation and intervention risk. But for companies, the problem is more direct.

A weaker yen raises the cost of imported materials, fuel, food inputs, machinery and dollar-priced goods. Large exporters can often absorb that pressure or even benefit from a weaker currency because overseas earnings translate into more yen. Smaller domestic companies do not have the same protection. Many buy inputs in foreign currencies but sell mostly in the local market. That leaves them exposed to a margin squeeze.

This is why the rise in weak-yen bankruptcies matters

The 45 bankruptcies recorded between January and June are not enough to say Japan is entering a corporate-default wave. The broader insolvency picture remains far below historic extremes. But the direction is important. A 32.3% increase shows that currency pressure is no longer theoretical. It is already breaking weaker balance sheets at the margin.

It does not begin with the strongest companies. It begins with firms that have thin margins, limited pricing power and little access to cheap refinancing. These businesses may survive when one pressure rises. They may even survive when two pressures rise. But when imported costs, wages, rents and interest expenses all move against them at the same time, the cushion disappears quickly.

Source: Tokyo Shoko Research

Major change for corporate Japan

For years, companies operated in a world where debt was cheap, refinancing was easy and lenders had little reason to force difficult decisions. That environment allowed many weaker firms to survive longer than they might have in a normal rate cycle. As long as interest costs stayed low, even companies with poor margins could keep rolling debt forward.

Higher rates do not need to reach extreme levels to create stress. They only need to rise enough to change refinancing math. A company that was comfortable at near-zero rates may look fragile when loans reset higher. If that same company is also paying more for imports because of the weak yen, the pressure becomes much harder to manage.

The BoJ is changing the funding environment

The BoJ’s departure from nearly two decades of ultra-low interest rates is becoming more than a policy shift. It is changing the assumptions behind corporate finance in Japan. After raising its policy rate to 1% in June, and with officials such as Naoki Tamura still arguing that rates should gradually move toward a neutral level around 2%, borrowing is no longer as effortless as it once was.

Source: Bank of Japan

Japan is moving into a different corporate cycle

The important point is that Japan’s policy normalization is happening while the yen is still weak.

That combination is uncomfortable. A weak yen keeps import costs high and feeds inflation pressure. Higher rates are meant to control inflation and support policy credibility, but they also raise financing costs for the same businesses already hurt by the currency. The BoJ is trying to normalize policy without damaging the economy. But for smaller companies, the adjustment is already painful.

This is why the bankruptcy data should not be ignored

It is not just about 45 companies. It is about what those bankruptcies reveal: the first layer of firms that cannot absorb Japan’s new macro environment. The market risk is not an immediate collapse. It is a slow widening of credit stress across smaller and more vulnerable companies.

This creates a difficult balance for policymakers

If the BoJ moves too slowly, yen weakness may continue to raise import costs and damage household purchasing power. If it moves too quickly, more companies could face refinancing pressure, especially those that relied on cheap debt for years.

Credit risk is becoming part of the Japan story

The old focus was simple: will the BoJ finally raise rates? The new question is more complicated: which parts of the economy can survive higher rates and a weaker yen at the same time?

For large firms with global revenues, strong cash flow and pricing power, the adjustment may be manageable. For small domestic firms, importers and companies with floating-rate debt, it is much harder.