Why do rising yields matter more than dovish Fed pricing

Usually, weak labour data pushes investors into duration. Yields fall, Fed rate hike expectations fall, and the long end of the curve starts pricing weaker growth. This time, the policy signal moved in one direction, but the bond market moved in another. Fed expectations became less hawkish, yet the ten-year yield rose toward 4.50%.

High-yield spreads near 2.75% are not yet confirming broad credit stress.

10-year yield rose to 4.49% into news that should have supported bonds.

If long yields rise and credit spreads widen at the same time, it will mean the cost of capital is rising in both sovereign and corporate markets.

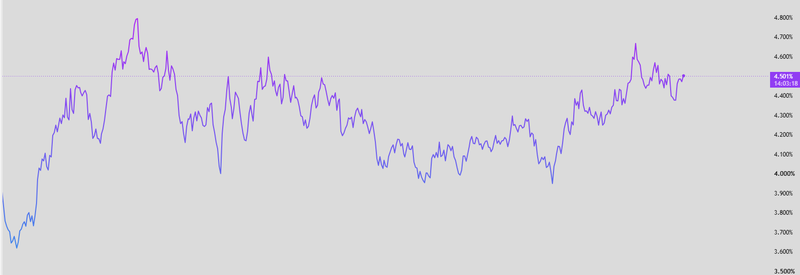

The long end refused to validate the jobs miss

The market did not react to the jobs miss the way a normal growth scare should behave.

The catalyst was not simply the weak labour data. It was the long end’s refusal to validate it. The 10-year yield rose to 4.49% into news that should usually push investors into bonds. In a clean growth scare, that move does not make sense. But this was not a clean growth scare. The long end looked less concerned with the next Fed decision and more focused on supply, fiscal risk and term premium.

That is the central contradiction. Fed pricing became less hawkish, but the market price of long-term money still moved higher. The message was not “the Fed is about to tighten more.” The message was that investors still want more compensation to hold long-dated government debt.

Source: Trading view

The bond market is trading something bigger than the Fed

The front end of the curve can still respond to labour data and Fed expectations. If payrolls disappoint, traders can price a lower chance of another hike or a higher chance of eventual cuts. That part of the market is still closely tied to the next few policy meetings.

Ten-year and thirty-year yields are different

They are not only about where the Fed takes rates next month. They are also about how much compensation investors demand to hold government debt for a long period. That compensation is rising because the market is becoming less comfortable with Treasury supply, the fiscal path and the risk that inflation does not return smoothly to target.

This is why the yield move matters

A weaker jobs report should have pulled long yields lower if investors believed the economy was moving into a normal disinflationary slowdown. Instead, yields rose. That means the market is not treating the labour miss as a simple “growth down, yields down” event.

Credit is not confirming recession stress yet

The first important divergence is between rates and credit.

If the labour miss were a true stress event, high yield should have reacted more aggressively. It did not. High-yield option-adjusted spreads remained near 2.75%, around the 13th percentile. That is not where broad credit fear usually announces itself.

This matters because credit often tells us whether the market sees weaker data as a real default-cycle risk or just a macro headline. So far, high yield is not behaving like investors are preparing for recession. Spreads near 2.75% suggest that companies are still being given access to capital at relatively calm risk premiums.

Source: Govspedning

The 3% level matters

If high-yield spreads stay near 2.75%, the market is not confirming recession stress. It is saying the jobs miss may matter for Fed pricing, but it has not yet changed the credit cycle.

But if spreads push above 3%, the signal becomes harder to dismiss.

At that point, the market would be saying something more serious. Credit investors would be starting to demand higher compensation for default risk at the same time the long end is already demanding more compensation for fiscal and duration risk.

The margin for comfort is narrowing

If long-end yields keep rising while credit spreads stay tight, the market may simply be repricing term premium and fiscal risk. That is uncomfortable, but not necessarily recessionary.

But if long-end yields rise and credit spreads widen at the same time, the message changes. It would mean the cost of capital is rising in both sovereign and corporate markets. Companies would face higher refinancing costs, investors would demand more compensation for risk, and weaker borrowers would feel the pressure first.