Brent crude and DXY advance on geopolitical concerns; European equities slip

Brent crude and the dollar index rose as tensions between Israel and Iran renewed concerns over energy supply, despite late-session hopes of de-escalation. European equities mostly declined amid risks of disruption to energy flows and expectations of tighter European Central Bank (ECB) policy.

Oil opened 5% higher after weekend attacks, but Brent closed up 1.25% and WTI rose 0.84% as hopes emerged for a US-backed pause.

Restrictions in the Strait of Hormuz and Houthi threats in the Red Sea kept energy supply risks elevated for Europe and Asia.

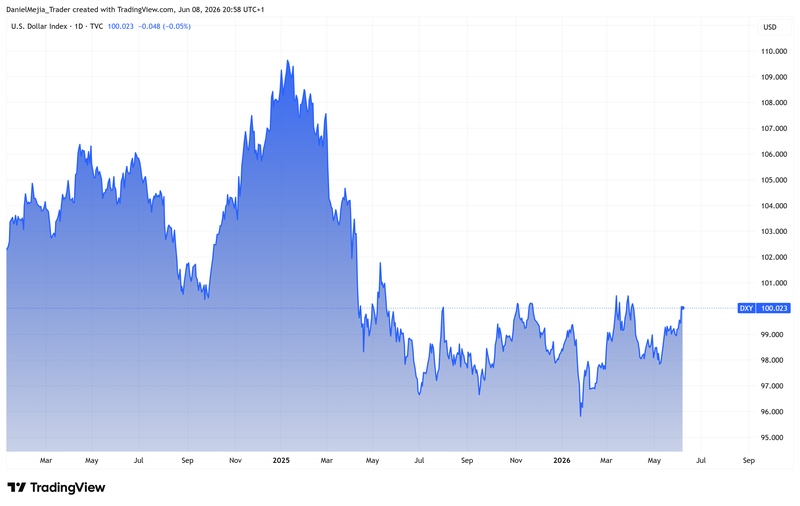

The DXY gained 0.84% over the week, trading near the 100-point mark, supported by strong US payroll data and rising expectations of further Fed tightening.

European equities declined: the CAC 40 fell 0.23% and the DAX 40 lost 0.58%, pressured by energy-related risks and expectations of an ECB rate increase.

Oil prices and dollar index increase amid rising geopolitical tensions

Oil prices closed with modest gains amid rising geopolitical tensions between Israel and Iran over the weekend. Oil benchmarks had opened the trading session around 5% higher following renewed bilateral attacks on Israeli, Iranian, and Lebanese territory. According to Reuters, Israel struck an Iranian petrochemical plant, which it said had been used to produce ballistic missiles. Concurrently, Iran launched attacks on Israeli territory, as well as on key areas in Bahrain and Kuwait, using ballistic missiles.

Nevertheless, by the market close, the Brent futures contract (BRNQ6) had risen by 1.25% to $94.25 per barrel, while West Texas Intermediate (WTI) increased by 0.84% to $91.30 per barrel, amid hopes of potential de-escalation. Reuters reported that Israel had stated it would halt attacks following a request from US President Donald Trump. However, Tehran warned that it would resume strikes if Israel continued attacking Lebanese territory.

At present, the Strait of Hormuz—a key maritime route through which around 20% of global oil supply transit passed before the conflict—remains restricted by Iranian forces, limiting traffic. Meanwhile, Houthi forces in Yemen, aligned with Iran, have stated that they would restrict vessels linked to Israel in the Red Sea, thereby adding to concerns over the energy supply chain, given the importance of this maritime corridor for energy flows between Europe and Asia.

Additionally, the US dollar index (DXY) posted a weekly gain of 0.84%, trading near the 100-point threshold. This renewed demand for the dollar stems from growing expectations that the Federal Reserve will maintain a restrictive monetary policy stance in order to contain inflationary pressures.

Last Friday, the Bureau of Labor Statistics (BLS) released a strong employment report, most notably showing non-farm payrolls above expectations, suggesting that lower interest rates from the US central bank may not be warranted. According to CME’s FedWatch Tool, market-implied probability indicates that an interest rate increase at the December meeting remains the most likely outcome. For the October meeting, the tool shows a 41.6% probability of a rate hike.

Figure 1. Dollar Index DXY (2024–2026). Source: Data from the Intercontinental Exchange (ICE); figure obtained from TradingView.

Israel-Iran tensions impact European equities

The re-escalation of the US–Israel–Iran conflict has had a modest negative impact on European stock markets. The French CAC 40 index fell by 0.23% to 8,199 points. In turn, the Spanish IBEX 35 declined by 0.66% to 18,223. Meanwhile, the German DAX 40 index depreciated by 0.58% to 24,616 points. By contrast, the UK FTSE 100 recorded a marginal gain of 0.05%.

European equity markets have been particularly affected because disruptions to oil supply in the Middle East have weakened Europe’s energy outlook, given the region’s high dependence on Middle Eastern and Asian supply. In addition, market participants expect that the European Central Bank (ECB) will raise interest rates at its next meeting, scheduled for this week, which is generally seen as unfavourable for equity markets as higher financing costs tend to weigh on corporate investment and business projects.

Key economic events this week

Several critical economic indicators are scheduled for release this week, with the following being of particular importance to market participants:

Tuesday

- Australia: Westpac Consumer Confidence

- Australia: NAB Business Confidence

- China: Balance of Trade

- Germany: Balance of Trade

- US: Existing Home Sales

Wednesday

- China: Inflation Rate

- Canada: BoC Interest Rate Decision

- US: Inflation Rate

- US: EIA Crude Oil Stocks Change

Thursday

- European Union: ECB Interest Rate Decision

- US: Producer Price Index

Friday

- United Kingdom: Industrial Production

- US: Michigan Consumer Confidence