Hawkish Fed bets rise on strong US data; Eurozone PPI accelerates

Strong US economic data and a sharp drop in crude inventories have boosted expectations of a hawkish Federal Reserve stance, dragging US stock indices down. Meanwhile, Eurozone producer prices accelerated to their highest level since 2023, while Australia's GDP growth slowed more than expected due to weaker domestic spending.

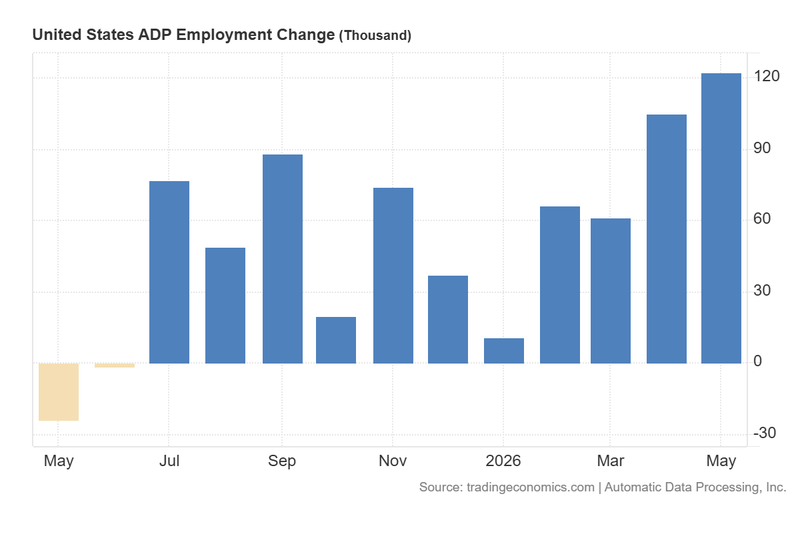

Strong ADP private employment (122K) and a rising ISM Services PMI (54.5) highlight US economic resilience, fuelling hawkish Fed expectations.

A sharp 7.97 million barrel drop in EIA crude inventories pushed oil benchmarks higher, increasing energy-driven inflation risks for the Fed.

Eurozone PPI accelerated to 4.9% in April—the highest since March 2023—ramping up inflationary pressure on the European Central Bank.

Australia's Q1 2026 GDP slowed to 0.3% due to moderate spending and mining disruptions, causing the Australian dollar to fall sharply by 0.72%.

ADP employment change and ISM Services PMI surpass analysts expectations, while EIA oil inventories fall sharply

Robust macroeconomic indicators from the employment and productivity sectors, paired with a significant drawdown in US Energy Information Administration (EIA) crude inventories, have reinforced market expectations that the Federal Reserve will maintain a "higher-for-longer" interest rate regime. Furthermore, the data has sparked concerns that policymakers might consider additional monetary tightening to curb persistent inflationary pressures.

On the one hand, data released by Automatic Data Processing (ADP) Inc. showed that private sector employment additions rose from 105k in April to 122k in May, marking the highest level since January 2025 and beating the consensus estimate of 117k. The ADP report highlighted that the strongest job creation occurred in "Education and health services," which added 57,000 positions, and "Trade, transportation, and utilities," which increased by 36,000. Conversely, the information sector contracted by 9,000 positions. This continued labour market strength is widely closely monitored as a leading indicator ahead of the official non-farm payrolls data due this coming Friday.

On the other hand, the Institute for Supply Management (ISM) reported that its Services PMI increased from 53.6 points in April to 54.5 in May, outperforming the analyst forecast of 53.8 points. Because this reading remains above the critical 50.0 threshold, it denotes a steady expansion within the service sector. Coupled with the robust Manufacturing PMI released by the ISM earlier in the week, the data demonstrates the ongoing resilience of US industrial productivity.

Additionally, the EIA reported a sharp weekly contraction in commercial crude oil inventories, which plunged by 7.97 million barrels. This drop suggests a notable increase in demand, partly driven by geopolitical and energy supply disruptions in the Middle East, which have redirected international demand toward US crude—particularly from European nations heavily reliant on Middle Eastern oil. The drawdown was significantly larger than the forecast 4 million barrel decrease and surpassed the prior week's decline of 3.33 million barrels. Consequently, crude benchmarks advanced on the tighter supply outlook: the Brent crude futures contract (BRNQ6) rose by 1.89% to $97.81 per barrel, while the West Texas Intermediate (WTI) contract (CLN6) appreciated by 2.41% to $96.02 per barrel.

Higher energy costs threaten to fuel broader consumer price inflation, exerting further pressure on the Federal Reserve to adopt a more restrictive monetary stance. According to the CME FedWatch Tool, the implied probability of a primary interest rate hike at the December 2026 meeting has climbed to 41.7%. Following these releases, major US equity benchmarks retreated in tandem as investors adjusted to the prospect of prolonged monetary restriction. The S&P 500 index fell by 0.74% to 7,553 points, the Nasdaq 100 declined by 0.29% to 30,571, and the Dow Jones Industrial Average depreciated by 1.21% to close at 50,692. Mirroring this market logic, the US Dollar Index (DXY) rose by 0.33% to 99.55 points.

Figure 1. US ADP Employment Change (2025–2026). Source: Data from Automatic Data Processing (ADP) Inc.; Figure obtained from Trading Economics.

Eurozone PPI accelerates, increasing pressures for the ECB

According to official data from Eurostat, the Eurozone Producer Price Index (PPI) accelerated sharply from 2.0% in March to 4.9% in April, slightly exceeding the analyst consensus of 4.8%. This reading represents the highest PPI rate recorded since March 2023, signalling significant upstream price pressures that the European Central Bank (ECB) may consider in its upcoming monetary policy decisions. Although ECB officials have reiterated the Governing Council's readiness to act should inflationary pressures become entrenched, policy formulation is complicated by underlying economic weakness; several key member states, most notably Germany, continue to face severe structural hurdles to a sustained economic recovery.

In response to the data and broader dollar strength, the euro depreciated by 0.27% against the greenback, closing the session at $1.1597.

Australian GDP growth prints below market consensus estimates

Data published by the Australian Bureau of Statistics revealed that gross domestic product (GDP) decelerated from a 0.9% expansion in the fourth quarter of 2025 to 0.3% in the first quarter of 2026 on a quarter-on-quarter basis. This print fell short of the 0.5% growth rate projected by market economists. Analysis from Trading Economics suggests the downshift was primarily driven by a moderation in both household consumption and government expenditure, compounded by temporary disruptions to output in the mining sector. Despite the softer quarterly performance, the annual growth rate of 2.5% suggests the Australian economy maintains a degree of structural stability.

Following the softer growth print, the Australian dollar fell sharply at the market close, depreciating by 0.72% against the US dollar to settle at $0.7128.