SK Hynix makes solid US market debut amid AI enthusiasm; Japanese PPI accelerates

The US American Depositary Receipts (ADR) debut of SK Hynix, raising $26.5 billion, has underscored ongoing enthusiasm for artificial intelligence, while Japan’s Producer Price Index (PPI) accelerated to 7.1%, intensifying inflationary concerns.

SK Hynix raised $26.5 billion via US ADRs to finance high-bandwidth memory (HBM) chip production and expand manufacturing capacity.

Shares closed at $168.01, propelling the firm's market capitalisation to $1.02 trillion and highlighting robust AI-driven investor demand.

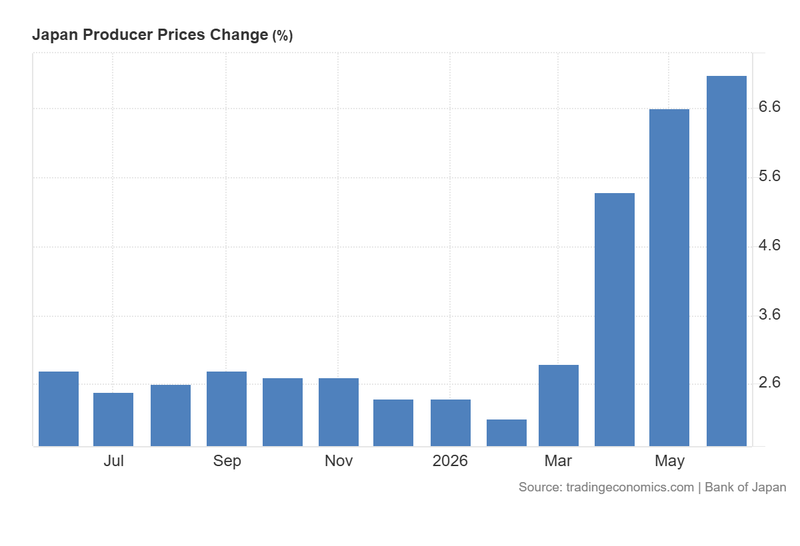

Japan's PPI climbed to 7.1%, exceeding market forecasts; this was propelled by surging energy costs, information technology components, and a weak yen.

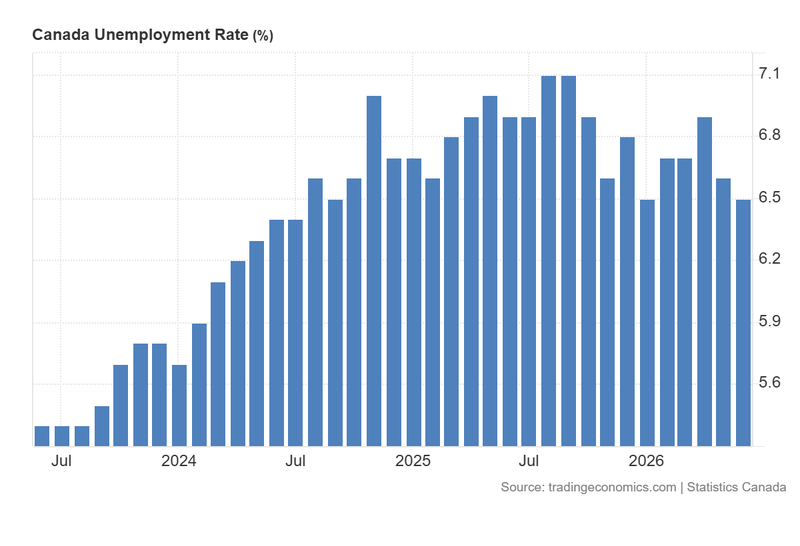

Canada's unemployment rate dropped to 6.5%, easing immediate pressure on the BoC to implement near-term interest rate cuts.

SK Hynix makes high-profile US market debut amid AI euphoria

The South Korean chipmaker SK Hynix has debuted on the US markets through the issuance of American Depositary Receipts (ADRs). The share sale generated $26.5 billion in capital for the firm, which will be deployed to support its global expansion plans. This includes the construction of new fabrication facilities and deeper investments in advanced memory technologies—notably, high-bandwidth memory (HBM) chips, which serve as critical hardware components for artificial intelligence (AI) applications.

At the opening bell, SK Hynix's ADRs commenced trading at $170 per share, embarking on a highly volatile session that reached an intraday maximum of $176 and a minimum of $166. By the close of trading, the shares settled at $168.01, establishing a market capitalisation of $1.02 trillion. This robust initial market response highlights sustained investor demand for enterprises positioned within the AI infrastructure ecosystem.

The transaction is particularly notable as it represents the second-largest share offering in United States history, following SpaceX's record offering earlier in 2026. However, while the success of the listing underscores market confidence in the AI investment thesis, it also raises broader questions regarding the long-term sustainability of the current AI capital-expenditure cycle.

As technology corporations commit hundreds of billions of dollars to AI infrastructure, the investment community will increasingly focus on whether these deployments can generate sufficient investment returns to justify their scale. As quoted by Reuters, BofA Securities analysts project that AI infrastructure capital expenditure could cross the $1.5 trillion threshold by 2027, a milestone that will require robust revenue streams to validate.

Japanese PPI accelerates for fourth consecutive month and surpasses forecasts

According to data released by the Bank of Japan, the country's Producer Price Index (PPI) accelerated from 6.6% in May to 7.1% in June, comfortably surpassing the 6.8% consensus forecast compiled by analysts. The current reading marks the highest level recorded since March 2023, reflecting mounting pressure on the Japanese central bank as wholesale costs risk being transferred to consumers if private enterprises are unable to absorb these elevated inputs indefinitely.

The report highlights that the most aggressive price pressures originated from petroleum and coal products, which surged from 13.7% in May to 22.8% in June, alongside information and communications technology costs, which advanced from 13.7% to 14.5%. These metrics demonstrate that the ongoing conflict in the Middle East has disrupted energy supply chains in Japan, given the nation's profound dependence on oil imports, whilst import costs have been further exacerbated by the sharp depreciation of the Japanese yen.

Nevertheless, following the macroeconomic release, the Japanese yen appreciated by 0.38% against the US dollar to trade at ¥161.72 amidst mounting speculation that the authorities might intervene to support the domestic currency. Concurrently, equity markets shrugged off immediate inflation fears as the Nikkei 225 index appreciated by 1.20% to close at 68,557 points.

Figure 1. Japan Producer Prices Change (2025-2026). Source: Data from the Bank of Japan. Figure obtained from Trading Economics.

Canadian unemployment rate decreases below market expectations

According to data from Statistics Canada, the national unemployment rate declined from 6.6% in May to 6.5% in June, dropping below the market forecast which had anticipated an unchanged reading. Consequently, the current metric has reached its lowest level in six months, reflecting a resilient domestic labour market.

Figure 2 highlights an inflection point that has established a downward trend since September 2025, thereby reducing immediate pressure on the Bank of Canada (BoC) to adopt an expansive monetary policy stance in upcoming sessions. Conversely, Canada's consumer inflation rate reached 3.2% in May, representing its highest level since December 2023.

Market participants are now intensely focused on the BoC's monetary policy decision scheduled for next week on July 15, where the consensus expects the central bank to maintain the benchmark interest rate unchanged at 2.25%. However, it is possible that the central bank could signal a more restrictive tone in its forward guidance, particularly given that the Federal Reserve has adopted a more hawkish stance in its most recent deliberations.

In response to the domestic data, the Canadian dollar appreciated marginally by 0.07% against the US dollar, trading at 1.4155.

Figure 2. Canada Unemployment Rate (2023-2026). Source: Data from Statistics Canada. Figure obtained from Trading Economics.