US stocks drop on inflation and geopolitical risks; EIA shows oil drawdown

US stocks fell sharply as hotter inflation, energy-driven price pressures, and the escalating conflict in the Middle East increased fears of a prolonged hawkish stance from the Federal Reserve. The S&P 500, Nasdaq 100, and Dow all declined, while the VIX rose sharply. Meanwhile, a larger-than-expected draw in US crude inventories lifted oil prices, underscoring concerns over supply disruptions.

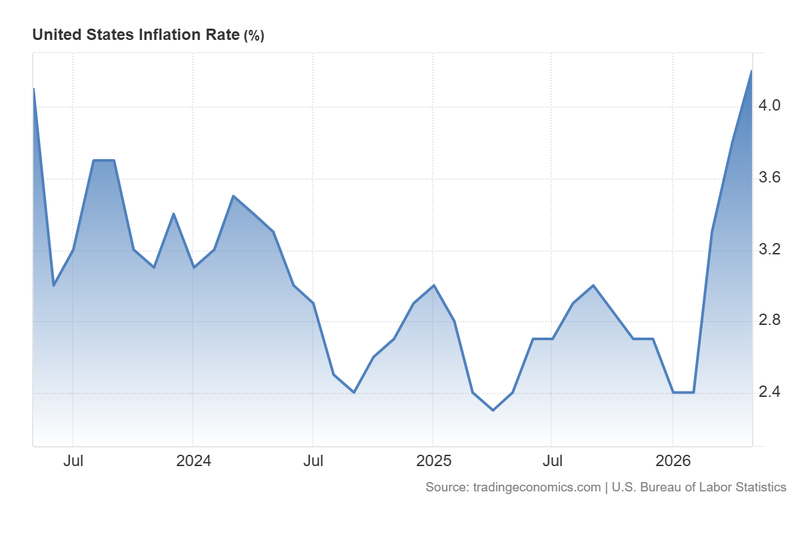

US CPI rose to 4.2% in May, the highest level since April 2023; core inflation edged up to 2.9%, reinforcing expectations of a hawkish Federal Reserve.

Escalating US–Iran and Israel–Hezbollah attacks weighed on sentiment; the S&P 500, Nasdaq 100, and Dow fell, while the VIX jumped by 11.82%.

The EIA reported a 7.23 million-barrel draw in crude inventories, lifting WTI by 2.22% as conflict-driven supply risks remained elevated.

China’s CPI held at 1.2%, below forecasts, while core inflation eased to 1.1%; weak domestic demand weighed on the FTSE China A50 and Hang Seng indices.

US indices decline amid inflation pressures and rising geopolitical tensions

US stock benchmarks declined in tandem amid an increase in the US inflation rate to multi-year highs and rising geopolitical tensions in the Middle East. According to Reuters, US President Donald Trump stated that the United States would attack Iran again “very hard” if a peace agreement with Tehran were not reached. At the same time, attacks on Iranian territory by US forces were reported. In response, Iran launched missile and drone strikes against US bases in Jordan, Kuwait, and Bahrain. Meanwhile, bilateral attacks between Israel and Hezbollah continued, suggesting that the ceasefire agreement remains highly fragile.

In addition, the US Bureau of Labor Statistics (BLS) reported that headline inflation accelerated from 3.9% in April to 4.2% in May on a year-on-year basis, in line with analysts’ expectations. This represents the highest inflation reading since April 2023, suggesting that inflationary pressures may be proving more persistent than previously expected. In turn, core inflation—which excludes the most volatile components, such as energy and unprocessed food—edged up from 2.8% to 2.9%, indicating that energy-linked inflation may also be feeding into underlying prices.

The BLS report showed that the most significant increases in headline inflation in May came from energy costs, which rose by 23.5% year on year, while gasoline prices increased by 40.5%. These price increases reflect the effects of the current conflict in the Middle East, which continues to disrupt global energy supply chains.

In light of the latest US inflation release, CME’s FedWatch Tool indicates a higher implied probability that the Federal Reserve will maintain its hawkish higher-for-longer stance. In addition, the tool assigns a 43.7% probability—the highest reading—to a 25-basis-point rate hike at the December meeting. Market participants are therefore focused on next week, when the Federal Reserve is scheduled to announce its monetary policy decision on Wednesday, 17 June. Market consensus expects the central bank to leave interest rates unchanged at 3.75%, while also releasing its updated economic projections.

Following these developments, US stock benchmarks fell sharply across the board. The S&P 500 index declined by 1.62% to 7,267 points, the Nasdaq 100 fell by 1.98% to 25,508, and the Dow Jones Industrial Average dropped by 1.87% to 49,924 points. By contrast, the VIX index rose by 11.82% to 22.23 points, signalling a highly volatile trading session.

Figure 1. US Inflation Rate (2023–2026). Source: Data from the US Bureau of Labor Statistics; figure obtained from Trading Economics.

EIA reports a sharp oil inventory draw

According to data from the US Energy Information Administration (EIA), crude oil inventories fell sharply by 7.23 million barrels in the latest weekly reading, a steeper decline than the 4 million-barrel draw expected by analysts. The current inventory update marks a seventh consecutive week of contraction, reflecting rising demand for US crude as a consequence of the US–Israel–Iran conflict in the Middle East—particularly from European countries seeking alternative energy sources to meet domestic demand.

Following the EIA inventory release, the West Texas Intermediate (WTI) futures contract (CLN6) rose by 2.22% to $90.02 per barrel. Oil prices continue to exhibit high volatility amid falling US crude reserves and rising geopolitical tensions in the Middle East, both of which reveal severe disruptions to global energy supply.

Chinese inflation is updated below analysts’ forecasts

According to data from the National Bureau of Statistics of China, the headline inflation rate remained unchanged at 1.2% in May on a year-on-year basis, below analysts’ forecasts of 1.3%. By contrast, the producer price index (PPI) accelerated to 3.9%, in line with market expectations. This suggests persistent weakness in Chinese domestic consumption, as producers are facing higher costs while keeping selling prices unchanged—or in some cases lower—in order to preserve demand. In addition, the core inflation rate slowed slightly from 1.2% in April to 1.1% in May, reinforcing the view that domestic demand remains relatively weak.

Following the Chinese inflation update, major stock benchmarks declined in tandem. The FTSE China A50 fell by 0.85% to 15,216, while the Hang Seng index dropped by 1.40% to 24,278 points.