US stocks rebound despite rising Middle East tensions; Chinese inflation slows

US equity markets advanced as a contraction in global oil prices countered geopolitical friction in the Middle East. Concurrently, consumer price inflation in China moderated to a 1.0% annual rate, while US domestic macro data revealed a decline in existing home sales.

The Nasdaq 100 index rose 1.62%, leading a broad market rebound despite escalating military skirmishes in the Gulf region.

Both Brent and WTI crude oil futures depreciated by approximately 2% on optimism regarding a localized diplomatic resolution.

The recently published Federal Reserve minutes underscored that central bank policymakers continue to prioritize inflationary risks over broader economic growth.

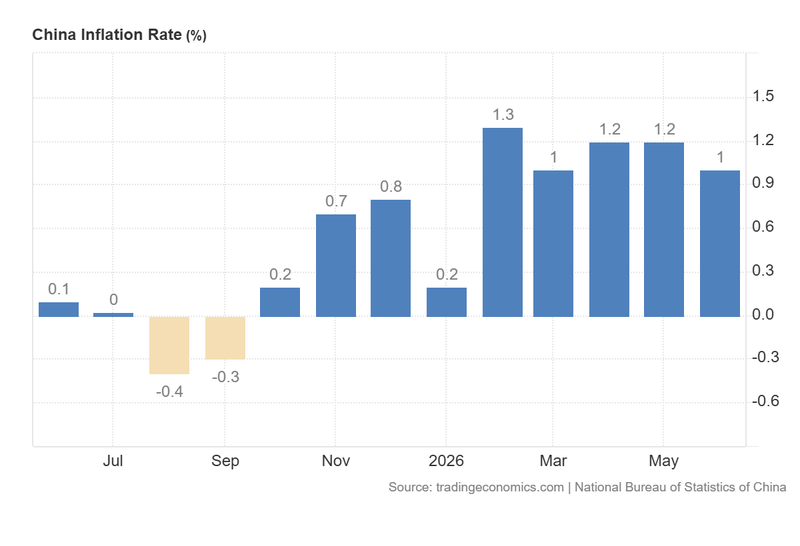

China's headline inflation rate cooled to 1.0% in June, primarily driven by a government-induced reduction in energy costs and softer demand within the housing sector.

Wall Street advances despite heightened Middle East risks

The primary US equity benchmarks advanced in tandem, defying escalating geopolitical tensions between the United States and Iran in the Middle East. At the closing bell, the S&P 500 index rose by 0.81% to 7,543 points, the Dow Jones Industrial Average added 0.27% to settle at 52,492, and the tech-heavy Nasdaq 100 index appreciated by 1.62% to close at 29,727 points.

According to reports from Reuters, both US and Iranian officials confirmed military strikes within the Gulf region. This development underscores the extreme fragility of the recent ceasefire agreement, which had briefly normalized maritime transit through the critical Strait of Hormuz over the preceding weeks. Despite this flashpoint, western equity markets moved higher while global crude benchmarks retreated. In the energy markets, the Brent crude futures contract (BRNU6) dropped by 2.20% to $76.30 per barrel, while the West Texas Intermediate (WTI) futures contract (CLQ6) fell by 1.96% to $72.08 per barrel. Market participants appear optimistic that a comprehensive peace accord may materialize in the near term, given the severe economic penalties both nations would incur should the conflict escalate further.

Simultaneously, the minutes from the Federal Open Market Committee’s (FOMC) previous meeting, released yesterday by the Federal Reserve, revealed that central bank officials remain structurally focused on persistent inflationary pressures rather than risks to employment or aggregate GDP growth. Policymakers noted that while the broader economy and the labour market demonstrate robust resilience, consumer prices continue to follow an upward trajectory significantly above the Fed's 2% target.

Chinese inflation rate decelerates below analyst expectations

Data published by the National Bureau of Statistics of China revealed that the headline consumer price index (CPI) decelerated from 1.2% in May to 1.0% in June, undershooting the market consensus of 1.1%. On a month-on-month basis, headline inflation contracted by 0.3%, representing a steeper decline than the 0.2% reduction anticipated by analysts. An analysis by Trading Economics indicates that this moderation was heavily influenced by a slowdown in transport cost growth, which fell from 5.4% to 4.1% following state-directed cuts to domestic retail gasoline and diesel prices aimed at mitigating energy pressures.

Furthermore, housing costs contracted by 0.3%, while food prices recorded a 1.6% deflationary decline. Conversely, the healthcare and education sectors experienced modest accelerations, rising from 2.1% to 2.3% and from 1.3% to 1.4%, respectively. In aggregate, while the headline disinflationary print is primarily attributable to administrative energy interventions and depressed housing demand, the marginal strength in healthcare and education services points to areas of possible resilient domestic consumption.

Following the macroeconomic release, the FTSE China A50 index advanced firmly by 2.86% to close at 15,277 points, whereas the Hang Seng index in Hong Kong experienced a marginal decline of 0.22%, finishing at 23,980 points.

Figure 1. China Inflation Rate (2025–2026). Source: Data from the National Bureau of Statistics of China; Figure obtained from Trading Economics.

US existing home sales decrease below forecasts

The US National Association of Realtors (NAR) reported that existing home sales contracted by 2.4% on a month-on-month basis in June. Consequently, the seasonally adjusted annual rate pulled back from 4.19 million to 4.09 million units. This downturn in housing market velocity is heavily correlated with mounting affordability constraints, driven by elevated property valuations and restrictive long-term borrowing costs.

Data from the Federal Reserve Bank of St. Louis highlights that the 30-year fixed-rate mortgage average reached 6.49% on July 9, remaining near a six-month high. This operational headwind facing the residential real estate sector could intensify if fixed-income markets continue to price in a "higher-for-longer" interest rate environment across the sovereign bond curve.