SpaceX-Anthropic deal turns AI compute into the next test for SpaceX valuation

SpaceX is no longer valued only as a rocket, satellite or Starlink story. The Anthropic deal changes the frame. By committing nearly $45 billion over the next three years for server capacity, Anthropic is effectively turning SpaceX into a major AI infrastructure provider as well as a space and connectivity company.

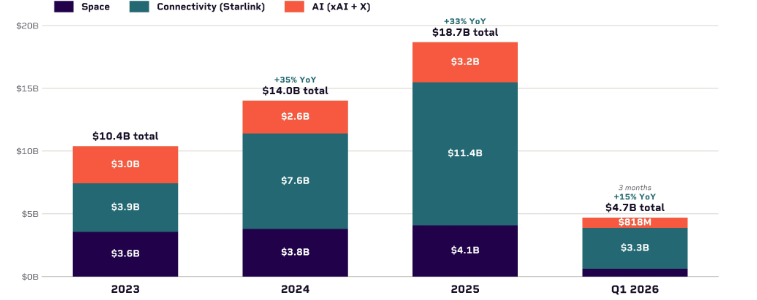

SpaceX could generate roughly $36 billion in total revenue in 2026.

Anthropic agreement gives SpaceX about $1.25 billion through May 2029.

The weaker scenario is a rejection from 172.45 followed by a move back below 156.40.

SpaceX’s Q2 earnings debut

Early independent estimates suggest SpaceX could generate roughly $36 billion in total revenue in 2026. But the market will not judge the company only on the size of that revenue. It will look at the mix.

Launch revenue is important, but it is still tied to mission timing. Starlink is more attractive because it is recurring, scalable and easier for investors to model. AI compute sits somewhere else entirely. It can become a powerful contracted revenue stream, but it also requires heavy spending before the economics are fully proven.

That is why the Anthropic agreement matters. Monthly payments of about $1.25 billion through May 2029 give SpaceX more visibility than one-off launches. Investors like that because visible revenue can support a higher valuation multiple, especially when the market is rewarding companies that can turn infrastructure into recurring cash flow.

Source: rexshare

visibility is not the same as free profit

AI infrastructure is expensive. It needs chips, power, cooling, land, networking and constant upgrades. So, the real question is not whether Anthropic’s demand is serious. It clearly is. The question is how much margin SpaceX can keep after building and operating the capacity needed to serve that demand.

But it also raises the burden of proof

The Cursor acquisition adds another layer to the story. SpaceX’s all-stock $60 billion acquisition of the AI coding tool creates a tighter link between compute, software and engineering automation. If it improves internal productivity, reduces development costs or strengthens SpaceX’s AI platform, the market may treat it as strategic. If not, investors may see it as another expensive bet before the returns are visible.

The Nasdaq-100 inclusion adds a separate technical force

SpaceX is scheduled to join the Nasdaq-100 after the market closes on Monday, July 6, 2026. That matters because index-tracking ETFs and passive funds will need to buy the stock. This type of demand can support prices in the short term because passive funds do not buy based on valuation. They buy because the rules require them to.

passive demand does not answer the bigger question

It can improve liquidity, widen institutional ownership and absorb some supply. It cannot prove the stock deserves a higher multiple. That proof must come from earnings quality, margin performance and the ability to turn AI compute demand into real cash flow.

The market is now being asked to value SpaceX as a launch provider, satellite network, AI compute platform and software ecosystem at the same time. That is a powerful story, but it is also a demanding one. The Anthropic deal strengthens the AI revenue bridge. Nasdaq-100 inclusion strengthens the shareholder base. Now the company must show that economics can support the narrative.

Technical outlook

SpaceX is no longer falling with the same force seen earlier in the correction. After losing a large part of the rally from above 220, the stock has spent several weeks trying to build a base between 147.20 and 156.40. Sellers have tested that area more than once, but each attempt has failed to create a clean breakdown. That does not make the chart bullish yet, but it does show that the market is starting to absorb the selling pressure.

The rebound toward 162 is the first sign that buyers are becoming more active again. The broader trend is still weaker than it was earlier in the year, so this is not a confirmed recovery. But the tone has changed. SpaceX is no longer trading like a stock in free fall. It is trading like a stock trying to decide whether the worst of the correction has already passed.

Momentum is also improving. RSI has recovered above 50, and the move above its signal line shows that short-term buying pressure is returning. Still, the signal needs confirmation from price. The more important development is the series of higher lows forming from the 147 area. That tells us sellers are finding it harder to push the stock back to the same lows.

Scenarios ahead

The first real test was 172.45. If SpaceX can break above that level and hold it, the recovery would look more convincing and could open the way toward 185–190. That area is likely to bring fresh selling interest but reaching it would still show that buyers have regained some control.

On the downside, 156.40 is the level that needs to be held first. A move below it would weaken the recovery attempt. The key floor remains 147.20. If that level breaks, the market would likely treat the recent rebound as only a pause inside the broader correction.

The constructive scenario needs SpaceX to hold above 156.40 and then clear 172.45. If buyers manage that, the chart would start to shift from stabilization to recovery, with 185–190 becoming the next area to watch.

The weaker scenario is a rejection near 172.45 followed by a drop back below 156.40. That would show the rebound still lacks strength. In that case, focus would return to 147.20. A clear break below that level would put sellers back in control and suggest the stock needs more time before forming a durable base.

Source: Trading view