How SpaceX makes money

Starlink is becoming the financial engine of Elon Musk’s private business empire, while SpaceX’s launch division and xAI show how expensive the next phase of growth may be.

Starlink has surpassed 12 million active users, up from nine million in 2025.

SpaceX continues to dominate launches, handling more than 80% of domestic payloads.

xAI generated $3.20 billion in revenue in 2025, but losses remain heavy.

How SpaceX makes money

SpaceX makes money from a mix of government contracts, commercial launches and Starlink subscriptions, but the quality of those revenues is not the same across the business. The government side gives SpaceX visibility and credibility. The U.S. Space Force has awarded the company a multi-billion-dollar contract ceiling running from 2025 through 2029, while NASA remains another important partner. These contracts are usually structured as firm fixed-price deals, which means SpaceX can protect or expand its profit if it delivers missions below budget. That is one reason government work matters. It does not only bring revenue; it rewards execution discipline. Government partnerships are estimated to represent around 20% of SpaceX profit, while NASA-related contracts may generate roughly 5% to 7% of profit. This gives the company a strong institutional revenue base, but it is not the main profit story anymore.

The real engine is Starlink

The satellite internet business generated about $11.39 billion in revenue last year and $4.42 billion in operating income, making it the clearest source of recurring profit inside SpaceX. This is important because Starlink is not a one-time launch business. It works more like a global infrastructure subscription model. Customers pay recurring fees, the network scales over time, and margins can improve as fixed satellite and ground-network costs are spread across a larger subscriber base. With operating margins near 39% and adjusted EBITDA of roughly $7.2 billion, Starlink gives SpaceX a kind of revenue profile investors usually value highly: predictable, recurring and software-like, but supported by hard infrastructure that is difficult for competitors to copy. That mix is why SpaceX is no longer viewed only as a rocket company. Launches and government contracts built the platform, but Starlink is increasingly what turns that platform into a profit machine.

The empire is no longer moving in one direction

Elon Musk’s private companies are often treated as one powerful growth story. But the latest numbers show something more interesting. The empire is not moving as one clean machine. It is splitting into very different financial realities.

Starlink is becoming a high-margin business with strong user growth and serious cash generation. SpaceX’s launch operation remains strategically dominant but still carries the cost of building and expanding into one of the most expensive industrial platforms in the world. xAI, meanwhile, is growing fast, but the price of competing in artificial intelligence is already showing up in heavy losses and massive capital spending.

That distinction matters. Musk’s empire is not short of ambition. The question is whether all that ambition can turn into financial discipline fast enough.

Starlink is becoming the strongest financial pillar

The satellite internet business has now surpassed 12 million active users, compared with nine million in 2025. That kind of growth matters because Starlink is not just adding customers. It is proving that its network can scale into a real recurring revenue business.

In the first quarter of 2026, Starlink generated $3.26 billion in revenue. More importantly, it produced $4.42 billion in operating profit and $7.17 billion in adjusted EBITDA, while maintaining a 63% operating margin.

Unlike the traditional launch business, Starlink functions primarily as a service provider. Revenue comes from monthly internet subscriptions paid by residential customers, sales of user terminals and equipment, enterprise connectivity agreements, government contracts, and specialized services for aviation, maritime and remote locations.

Once satellites are deployed and customers are connected to the network, the business benefits from recurring revenue that can continue generating cash over long periods.

That is not a small detail. It changes the way the wider Musk ecosystem is viewed. Starlink is no longer just a bold satellite project. It is starting to look like the cash engine that can support much bigger ambitions elsewhere. The problem is that the rest of the empire still needs a lot of cash.

SpaceX dominates launches, but dominance is expensive

SpaceX remains one of the most important companies in the global space industry.

Its rocket launch division continues to dominate the market, handling more than 80% of all domestic payloads. That makes SpaceX more than a private space company. It has become a core part of US launch capacity and a critical player in satellite deployment, defense infrastructure and commercial space activity.

The company earns revenue through commercial satellite launches, government and defense missions, NASA contracts, deployment of Starlink satellites and a growing range of space-related infrastructure services.

Its market position is exceptionally strong. SpaceX handles more than 80% of domestic payload launches, making it a critical component of the U.S. space economy and one of the most influential players in the global launch industry.

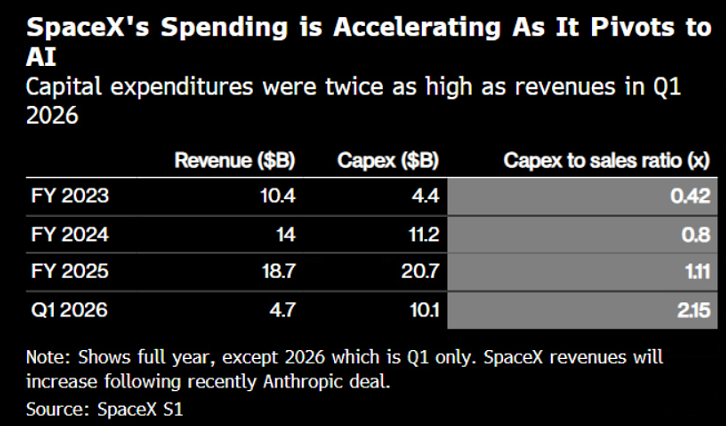

SpaceX reported a consolidated net loss of $4.94 billion for the full year 2025. That number does not erase the company’s strategic importance, but it does highlight the cost of staying ahead. Rockets, launch systems, Starship development, satellite deployment and infrastructure expansion all require enormous capital.

This is the difficult part of the story. SpaceX may be dominant, but it is still operating in a business where leadership must be constantly funded.

A huge forecast raises huge expectations

Goldman projects SpaceX’s total revenue could rise to $474 billion by 2030, up from $18.7 billion in 2025. That would be roughly a 25-fold increase.

On paper, that forecast is extraordinary. It suggests that investors look at SpaceX as something much larger than a launch company. They are looking at a platform that combines rockets, satellites, communications, infrastructure and possibly future links with AI and defense.

To get there, SpaceX needs more than demand. It needs execution across several difficult businesses at the same time. Starlink must keep expanding. Launch activity must keep rising. Costs need to be controlled. And the company must keep funding long-term projects without letting losses dominate the narrative.

Source: Bloomberg

xAI is growing, but the AI race is brutally expensive

The company generated $3.20 billion in revenue in 2025 and brought in $818 million in revenue during the first quarter of 2026. That shows real momentum for a young AI business.

xAI posted an operating loss of $6.35 billion in 2025, followed by another $2.47 billion operating loss in the first quarter of 2026 alone. AI-related capital expenditure reached $12.7 billion, driven by aggressive investment in data center chips and computing clusters.

That is the price of trying to compete in AI at the highest level. This is no longer only a software race. It is an infrastructure race. The companies that want to lead need chips, power, data centers, engineers, models and distribution. xAI is trying to move quickly. But speed at this level is expensive.

FAQs

What is SpaceX's biggest source of income?

SpaceX’s biggest source of income is Starlink, its satellite internet business. Rocket launches remain important, especially for NASA, commercial satellites and defence work, but Starlink gives SpaceX recurring monthly revenue from internet subscribers. That makes it more scalable than one-off launch contracts. As the Starlink user base grows across homes, businesses, airlines, ships and remote regions, it becomes the company’s main financial engine and a key part of SpaceX’s long-term valuation story.

Does SpaceX make more money from Starlink or rocket launches?

SpaceX likely makes more money from Starlink than from rocket launches. Launch services still generate large revenue from government and commercial customers, but that income depends on mission schedules and contract flow. Starlink is different because it works like a subscription business, with customers paying every month for satellite internet. That recurring revenue can grow faster and become more predictable over time. Rocket launches built SpaceX’s reputation, but Starlink is increasingly shaping its financial future.

How does SpaceX's AI business contribute to revenue?

SpaceX’s AI business is not yet its main source of revenue. For now, AI is more connected to future growth, automation, satellite operations, data infrastructure and possible links with Elon Musk’s wider technology ecosystem. AI could help SpaceX improve network management, launch systems, robotics and Starlink performance. But compared with Starlink subscriptions and launch contracts, AI is still an early-stage opportunity. It may support future revenue, but it is not yet the company’s proven profit engine.

How does SpaceX's business model differ from traditional aerospace companies?

SpaceX differs from traditional aerospace companies because it is vertically integrated, faster-moving and more commercially diversified. Traditional aerospace firms often rely heavily on government contracts, long development cycles and expensive single-use systems. SpaceX builds reusable rockets, launches its own satellites and sells internet directly through Starlink. This gives it both launch revenue and recurring subscription revenue. That combination makes SpaceX look less like a normal defence contractor and more like a mix of aerospace, telecom and technology company.

What are the biggest risks to SpaceX's future growth?

The biggest risks to SpaceX’s future growth are regulation, execution risk, competition and heavy capital spending. Starship still needs major technical progress, while Starlink faces pressure from telecom companies, satellite rivals and spectrum regulators. SpaceX also depends on launch approvals, government contracts and safe orbital operations. Another risk is cost: satellites, rockets, AI infrastructure and global network expansion require huge investment. If growth slows or regulation tightens, SpaceX’s valuation and profitability could come under pressure.