SpaceX IPO risks: 7 red flags investors should know before buying

The bull case for SpaceX is easy to sell: dominant launch economics, Starlink scale, and Elon Musk’s ability to keep investors dreaming several years ahead. The harder question is whether public buyers are being asked to pay too much, too early, for a business that is still losing money and taking on new, expensive bets.

The IPO is targeting a $1.75 trillion valuation.

SpaceX lost $4.94 billion in 2025 despite strong revenue growth.

AI spending is now a major drag on profits and cash flow.

Tight float, retail demand, and index buying could fuel sharp early volatility.

Why this SpaceX IPO risk matters now

If you are asking should I buy SpaceX IPO, you are already asking the right question the wrong way. The better question is this: what has to go right to justify buying one of the largest listings in market history at a valuation that would immediately place SpaceX among the most valuable companies in America? Reuters reported that SpaceX plans to raise about $75 billion at $135 per share, implying a valuation of roughly $1.75 trillion, with trading expected to begin on June 12. That alone makes the stock hard to value with a straight face and easy to over-romanticize.

The valuation already prices in a lot of perfection

The first and biggest red flag is the price tag. At around $1.75 trillion, investors are not buying a misunderstood mid-cap with room for discovery. They are buying a company already valued like a fully matured mega-cap, even though its business mix is still evolving and its newest growth engine remains highly speculative. Reuters described the deal as potentially the first U.S. IPO above $1 trillion, which tells you everything about how much success is already embedded in the offer price. If you are wondering is SpaceX IPO overvalued, that is where the skepticism begins.

The company is growing fast, but it is still losing serious money

Revenue growth is not the problem. Profitability is. Reuters reported that SpaceX’s revenue rose to $18.67 billion in 2025 from $14.02 billion a year earlier, yet the company swung to a $4.94 billion net loss from a prior-year profit of $791 million. That kind of reversal matters because it tells investors the business is not simply reinvesting from a position of steady profitability. It is scaling while absorbing heavy losses, and that raises the question of whether public shareholders are funding ambition more than earning power.

AI spending is becoming the biggest financial risk

SpaceX’s story is no longer just rockets and Starlink. Reuters reported that following the February purchase of xAI, AI became central to the IPO pitch and also to the company’s losses. In the first quarter of 2026, SpaceX posted an overall operating loss of $1.94 billion on $4.69 billion in revenue, while the AI division alone generated $818 million in revenue and $2.47 billion in losses. SEC filing snippets also show just how capital-heavy this has become, with AI capital expenditures running into the billions. That is a real red flag because AI is not just an add-on here; it is now a major consumer of cash.

Starlink is carrying the company more than many buyers may realize

Another risk is concentration. Reuters reported that of SpaceX’s three divisions, only the connectivity segment powered by Starlink was profitable in the first quarter of 2026. Starlink generated $1.19 billion in operating profit, but that was not enough to offset losses elsewhere. In other words, one business is doing much of the financial heavy lifting while newer bets consume capital. That does not make SpaceX broken, but it does make the company more dependent on one segment than the broad “space-plus-AI” narrative might suggest.

Musk’s control means public investors will have limited influence

This is one of the clearest SpaceX IPO red flags for institutional investors. Reuters reported that the offering uses a dual-class structure that concentrates voting power with Musk and insiders, and that the filing gives shareholders little meaningful say over his decisions. The company’s unusual governance provisions also preserve Musk’s effective control over the board and over his roles as both chief executive and chairman. If you buy this IPO, you are largely buying into Musk’s judgment with limited ability to challenge it. That can work brilliantly when the founder is right. It can also go very badly when he is not.

Competition is intensifying just as SpaceX expands into harder markets

SpaceX still has a major edge in launch and satellite scale, but competition is not standing still. Reuters explicitly noted that the private space race is intensifying, and the filing itself leans heavily on SpaceX dominating technologies and markets that do not yet exist, including AI data centers in space. That is a subtle but important risk. Investors are not only underwriting the existing launch and connectivity businesses; they are also being asked to underwrite future dominance in categories that remain commercially unproven and likely to attract deep-pocketed competition.

Retail hype and first-day volatility could distort the stock immediately

The final red flag is market behavior rather than company fundamentals. Reuters reported that only around 7% of SpaceX’s listed shares will be freely tradable at launch, while early index inclusion rules from MSCI could force passive funds to buy the stock soon after listing. At the same time, Reuters also reported that SpaceX plans to allocate up to 30% of the IPO to retail investors, and that IPO fever has already triggered speculative activity in related names across Asia. Add in Reuters’ report that the book was only around two times oversubscribed a few days before listing, and you have the ingredients for a stock that could swing wildly on day one regardless of where fair value actually sits.

So, should you buy SpaceX IPO?

SpaceX may turn out to be a long-term winner. That is not the same thing as saying the IPO is a great buy on day one. The risk case is clear: a massive valuation, heavy losses, AI capex, founder control, rising competition, and a trading setup that could become chaotic as passive flows and retail enthusiasm hit a relatively tight float. For cautious investors, the real opportunity may not be owning SpaceX at any price. It may be waiting to see whether the market gives you a better one.

Meta Platforms, still operating under the Facebook name when it went public in 2012, offered a reminder that major technology IPOs do not always deliver instant gains. The company priced its shares at $38, opened near $42, and then lost momentum quickly, ending its first session almost unchanged. That was a weak debut by IPO standards, where deals are often priced to leave room for an early pop. The pressure continued over the following year, with the stock falling more than 30% before eventually becoming one of the market’s biggest long-term winners. Meta shares are now more than 1,400% above their IPO price.

Source: Bloomberg

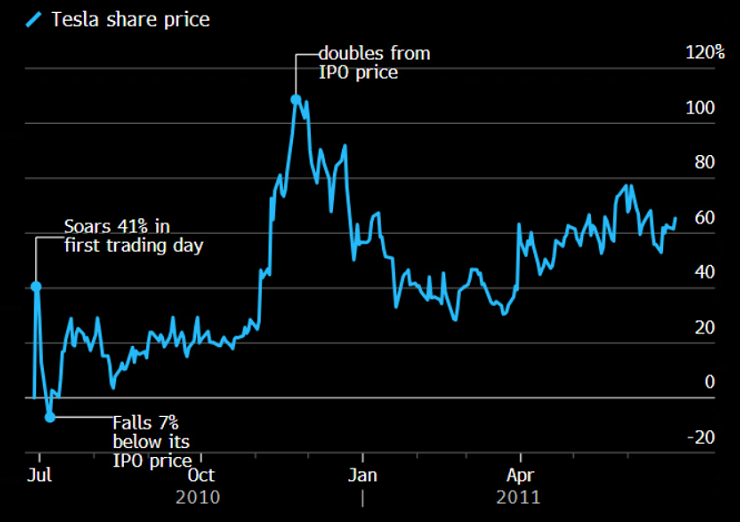

Tesla provides another clear example of how messy the early trading period can be for a high-profile growth stock. After its June 2010 IPO, shares moved sideways for several months, rallied late in the year, and then pulled back again. One year after listing, Tesla was up about 18%, but it was still lagging the S&P 500 and trading below its earlier peak. The stock has remained highly volatile ever since, yet that volatility did not stop Tesla from becoming one of the most powerful long-term performers in the market.

Source: Bloomberg