Gold slides toward worst month in 17 years as Fed easing hopes fade

Gold prices edged higher on Tuesday as hopes for a possible easing of the US-Iran conflict supported sentiment, but the metal remained on course for its steepest monthly decline in more than 17 years as rising energy prices pushed investors to scale back expectations for Federal Reserve rate cuts.

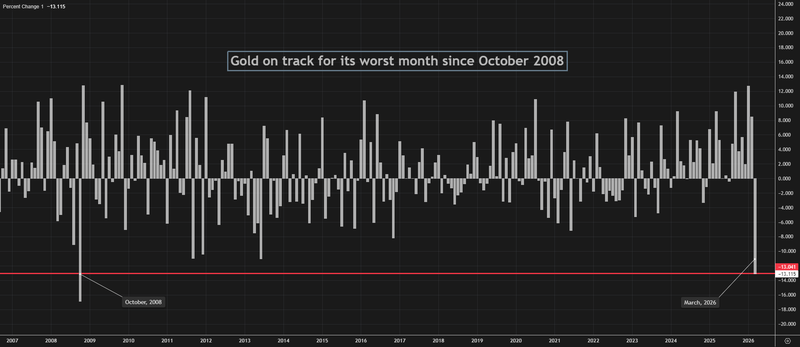

Gold is down more than 13% in March, its worst month since October 2008.

Hopes for de-escalation in the Middle East helped prices rebound on Tuesday.

Higher energy prices have sharply reduced expectations for Fed rate cuts this year.

Gold is still on track for a quarterly gain despite the March selloff.

Gold finds brief support from easing geopolotical tesnsion fears

Gold prices rose in early Tuesday trading as investors reacted to signs that the conflict in the Middle East may not intensify further in the immediate term. Reports that President Donald Trump is willing to end the US military campaign against Iran, even if the Strait of Hormuz remains largely closed for now, helped trigger a modest relief move across financial markets.

March has turned into gold’s worst month in years

Even with Tuesday’s rebound, bullion remains deep in the red for the month. Gold has fallen more than 13% in March, putting it on track for its sharpest monthly decline since October 2008.

Source: Reuters

The scale of the pullback reflects a major change in the interest-rate outlook rather than a collapse in gold’s long-term appeal. The market has increasingly concluded that the Federal Reserve may not cut rates at all this year, as the jump in oil and energy prices linked to the Middle East tension threatens to keep inflation elevated for longer.

That shift has hurt gold because the metal tends to perform best when interest rates are falling or expected to fall. As a non-yielding asset, it becomes less attractive when investors expect policy to stay tight.

Fed outlook has turned against bullion

Before the latest tension-driven energy shock, markets were broadly expecting two Fed rate cuts in 2026. That view has now been largely dismantled. Traders have almost fully priced out the prospect of any easing this year, with policymakers signaling that inflation must resume cooling before cuts can come back into the picture.

Chair Jerome Powell’s recent comments reinforced that message. His wait-and-see tone on the inflation effects of the tension made clear that the Fed is in no hurry to ease while energy prices remain a fresh upside risk.

That has left gold squeezed between two forces: lingering geopolitical anxiety, which would normally support it, and a rising-rate environment, which has become the more dominant driver this month.

Stabilization, but not yet recovery

There are signs that the selling pressure may be easing. Gold has been stabilizing for about a week, and last Friday’s rally stood out because it came alongside falling Treasury yields, suggesting some investors are beginning to view the Iran war less as a pure inflation shock and more as a potential drag on growth.

That nuance matters. If markets start treating the conflict as a recession risk rather than only an oil-price problem, gold could find firmer support again. For now, though, the metal remains caught in the tension between geopolitical demand and the fading prospect of Fed easing.

Long-term forecasts stay constructive

Despite the sharp March slide, gold is still up about 5% for the quarter, showing that the broader trend has not fully broken. Some longer-term forecasts also remain bullish. Goldman Sachs, for example, continues to expect gold to reach $5,400 an ounce by the end of 2026, supported by central-bank diversification and eventual Fed easing.

That leaves the market in an awkward position. Short term, gold is suffering from the collapse in rate-cut hopes. Longer term, many still see the structural case intact.

For now, though, March belongs to the bears.