Kharg island tensions push Brent to 2022 high

Brent crude prices climbed sharply reaching around $106 per barrel, the highest level since mid-2022, as geopolitical tensions in the Middle East intensified and traders grew increasingly concerned about disruptions to global oil supply.

Kharg Island is critical to Iran’s oil exports, handling roughly 90% of the country’s shipments.

War is currently affecting around 7.5% of global oil supply.

History shows that geopolitical disruptions in the Middle East often have an outsized impact.

A critical route under pressure

Kharg Island sits at the heart of Iran’s energy exports. Any escalation around the facility immediately affects global supply expectations. U.S. President Donald Trump warned that Iran’s energy infrastructure on the island could become a target if Tehran interferes with shipping through the Strait of Hormuz, one of the world’s most vital oil transit routes.

The Strait of Hormuz connects the Persian Gulf to global markets and is responsible for nearly 20% of daily crude flows worldwide. Historically, even short-term disruptions in the strait have triggered sharp price spikes and logistical bottlenecks, highlighting the fragility of global oil supply chains. Since the conflict began, tanker activity has slowed considerably. Heightened security risks have forced companies to reroute shipments, delay deliveries, or halt operations temporarily, adding pressure to an already tight market.

The market reaction has been swift. Brent crude’s rise to $106 per barrel reflects concerns over potential supply shortages and the broader geopolitical risk to Middle Eastern exports. Analysts note that even a temporary closure of the strait could disrupt refining schedules, push up shipping costs, and drive volatility in fuel markets worldwide.

Source: Trading View

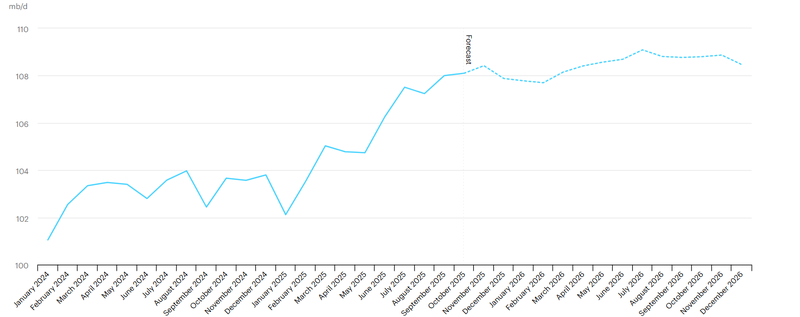

A historic supply shock

According to the International Energy Agency, the current conflict represents one of the most significant supply shocks in recent memory. The war is estimated to be impacting 7.5% of global oil supply, and its effects on exports further magnify the disruption. In practical terms, the IEA projects a potential reduction of 8 million barrels per day this month, equivalent to roughly 250 million barrels removed from the market, a scale rarely seen outside of major global crises.

To mitigate immediate pressure, the IEA confirmed that oil from a record 400-million-barrel strategic reserve release will begin reaching Asian markets almost immediately. While this supply injection can temporarily ease shortages and calm short-term market volatility, it is not a long-term solution if the conflict continues or intensifies. Analysts note that ongoing disruptions could keep Brent crude prices elevated above $100 per barrel for the coming months, with renewed spikes if key export infrastructure is damaged or shipping lanes remain restricted.

Looking ahead, the situation may also reshape global trade patterns. Countries dependent on Middle Eastern crude could accelerate plans to diversify supply, sourcing oil from Africa, South America, or the U.S., while refiners may adjust production schedules to prioritize lighter or alternative grades of crude. This could create a period of sustained volatility and higher energy costs in Asia, Europe, and North America, with potential knock-on effects for fuel prices and industrial energy consumption.

Even if the conflict stabilizes in the near term, market participants may continue to price in a risk premium due to the strategic importance of the Strait of Hormuz and Kharg Island. This suggests that oil prices could remain structurally higher than pre-conflict levels, reflecting both the immediate supply disruption and the longer-term perception of geopolitical risk in one of the world’s most critical oil-producing regions.

Source: IEA

Markets balancing risk and supply

Energy markets are now navigating a complex environment. On one hand, the disruption of Kharg Island and the threat to the Strait of Hormuz could tighten supply significantly. On the other, reserve releases and reports of a potential U.S.-led coalition to escort commercial tankers provide some reassurance to traders. If realized, this coalition could partially restore shipping confidence, though risks would remain elevated as long as hostilities continue.

History shows that geopolitical tensions in the Middle East tend to amplify price swings because of the region’s central role in supplying global energy. Even short-term closures can have ripple effects, affecting shipping schedules, refining operations, and fuel availability worldwide. The current situation is particularly concerning given the limited spare production capacity elsewhere, leaving markets vulnerable to sustained volatility.